Zero-Coupon Bonds: Definition, How They Work & Examples

A zero-coupon bond is a bond that pays no interest and trades at a discount to its face value. It is also called a pure discount bond or deep discount bond. U.S. Treasury billsTreasury Bills (T-Bills)Treasury Bills (or T-Bills for short) are a short-term financial instrument issued by the US Treasury with maturity periods from a few days up to 52 weeks. are an example of a zero-coupon bond.

Quick Summary:

- A zero-coupon bond is a bond that pays no interest.

- The bond trades at a discount to its face value.

- Reinvestment risk is not relevant for zero-coupon bonds, but interest rate risk is relevant for the bonds.

Understanding Zero-Coupon Bonds

As a zero-coupon bond does not pay periodic coupons, the bond trades at a discount to its face value. To understand why, consider the time value of moneyTime Value of MoneyThe time value of money is a basic financial concept that holds that money in the present is worth more than the same sum of money to be received in the future. This is true because money that you have right now can be invested and earn a return, thus creating a larger amount of money in the future. (Also, with future.

The time value of money is a concept that illustrates that money is worth more now than an identical sum in the future – an investor would prefer to receive $100 today than $100 in one year. By receiving $100 today, the investor is able to put that money into a savings account and earn interest (thereby having more than $100 in a year’s time).

Extending the idea above into zero-coupon bonds – an investor who purchases the bond today must be compensated with a higher future value. Therefore, a zero-coupon bond must trade at a discount because the issuer must offer a return to the investor for purchasing the bond.

Pricing Zero-Coupon Bonds

To calculate the price of a zero-coupon bond, use the following formula:

Where:

- Face value is the future value (maturity value) of the bond;

- r is the required rate of return or interest rate; and

- n is the number of years until maturity.

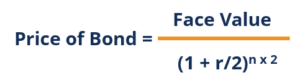

Note that the formula above assumes that the interest rateInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. is compounded annually. In reality, zero-coupon bonds are generally compounded semi-annually. In such a case, refer to the following formula:

Note that the formula above looks similar to the previous one, with the only difference being the required rate of returnRequired Rate of ReturnThe required rate of return (hurdle rate) is the minimum return that an investor is expecting to receive for their investment. Essentially, the required rate of return is the minimum acceptable compensation for the investment’s level of risk. (r) being divided by 2 and the number of years until maturity (n) being multiplied by two. Since the bond compounds semi-annually, we must divide the required rate of return by two and multiply the number of years until maturity by two to account for the total number of periods the bond will be compounded for.

Example of a Zero-Coupon Bonds

Example 1: Annual Compounding

John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today?

Price of bond = $1,000 / (1+0.05)5 = $783.53

The price that John will pay for the bond today is $783.53.

Example 2: Semi-annual Compounding

John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded semi-annually. What price will John pay for the bond today?

Price of bond = $1,000 / (1+0.05/2)5*2 = $781.20

The price that John will pay for the bond today is $781.20.

Reinvestment Risk and Interest Rate Risk

Reinvestment risk is the risk that an investor will be unable to reinvest a bond’s cash flows (coupon payments) at a rate equal to the investment’s required rate of return. Zero-coupon bonds are the only type of fixed-income investments that are not subject to investment risk – they do not involve periodic coupon payments.

Interest rate risk is the risk that an investor’s bond will decline in value due to fluctuations in the interest rate. Interest rate risk is relevant when an investor decides to sell a bond before maturity and affects all types of fixed-income investments.

For example, recall that John paid $783.53 for a zero-coupon bond with a face value of $1,000, 5 years to maturity, and a 5% interest rate compounded annually. Assume that immediately after John purchased the bond, interest rates change from 5% to 10%. In such a scenario, what would be the price of the bond?

Price of bond = $1,000 / (1+0.10)5 = $620.92

If John were to sell the bond immediately after purchasing it, he would realize a loss of $162.61 ($783.53 – $620.92).

To conclude:

- Reinvestment risk is not relevant for zero-coupon bonds; and

- Interest rate risk is relevant for zero-coupon bonds.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Continuously Compounded ReturnContinuously Compounded ReturnContinuously compounded return is what happens when the interest earned on an investment is calculated and reinvested back into the account for an infinite number of periods. The interest is calculated on the principal amount and the interest accumulated over the given periods

- Effective Annual Interest RateEffective Annual Interest RateThe Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective

- Interest Rate RiskInterest Rate RiskInterest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (e.g., bonds) rather than with equity investments.

- 10-Year US Treasury Note10-Year US Treasury NoteThe 10-year US Treasury Note is a debt obligation that is issued by the US Treasury Department and comes with a maturity of 10 years.

-

Understanding Call Protection in Bonds: Investor Protection Explained

Call protection refers to protection from investment risk to bond investors that exists by limiting the conditions under which a bond issuer may elect to call, i.e., redeem bonds before a bond’s

-

Understanding Call Provisions in Bonds: A Comprehensive Guide

A call provision refers to a clause – essentially, an embedded optionEmbedded OptionAn embedded option is a provision in a financial security (typically in bonds) that provides an issuer or hold

invest

- Personal Bond Explained: Release from Jail Without Bail

- Understanding Bond Duration: A Key Fixed Income Metric

- Understanding Bond Accretion: A Comprehensive Guide

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Noncallable Securities: A Comprehensive Guide

- Samurai Bonds: A Guide to Understanding Yen-Denominated Corporate Debt

- Treasury Bonds: A Comprehensive Guide to U.S. Government Debt

- Understanding Bonds: A Comprehensive Guide for Investors

-

Understanding Call Dates: What You Need to Know

Understanding Call Dates: What You Need to KnowA call date refers to the date when a callable bondCallable BondA callable bond (redeemable bond) is a type of bond that provides the issuer of the bond with the right, but not the obligation, to rede...

-

Understanding Call Prices: Callable Bonds & Preferred Stocks

Understanding Call Prices: Callable Bonds & Preferred StocksA call price refers to the price that a preferred stock or bond issuer would pay to buyers if they chose to redeem the callable security before the maturity date. The price is set during the issuance ...