Understanding Qualifying Dispositions: Tax Benefits for Stock Sales

Qualifying disposition is a tax term used in the U.S. that refers to a sale or other disposition of shares that receive favorable tax treatment for the individual disposal of the stock.

Qualifying dispositions are important for stockholders because there may be a wide disparity between the stockholder’s regular income tax rate and the significantly lower long-term capital gains tax rateCapital Gains TaxCapital gains tax is a tax imposed on capital gains or the profits that an individual makes from selling assets. The tax is only imposed once the asset has been converted into cash, and not when it’s still in the hands of an investor.. Therefore, qualifying dispositions can save stockholders a substantial amount of money in relation to taxes owed.

The qualifying disposition tax rules most commonly apply to stock that individuals acquire by virtue of being employed by the company issuing the stock. They may acquire stock shares through an employee stock purchase plan (known as an ESPP) or incentive stock option plans (referred to as ISOs).

ISOs are typically stock purchase options offered to employees who occupy an upper-level executive management position, such as the Chief Executive Officer (CEO), Chief Financial Officer (CFO), or Sales Manager.

Summary

- Qualifying disposition is a tax term used in the U.S. that refers to a sale or other disposition of shares that receives favorable tax treatment.

- The qualifying disposition rules are important because of the wide disparity between an individual’s marginal tax rate and the significantly lower capital gains tax rate.

- The determining factor for qualifying dispositions is the length of time an individual holds onto stock shares before selling them.

How It Affects Your Taxes – Example

Assume that you acquire 100 shares of your company’s stock through an ESPP that enables you to buy shares at a 10% discount to their current market priceMarket PriceThe term market price refers to the amount of money for what an asset can be sold in a market. The market price of a given good is a point of convergence of $20 per share, so you only need to pay $18 per share for the stock. Your total purchase price for 100 shares is $1,800.

Further, assume that you can sell your stock shares for a price of $35 a share a few years later. Your total proceeds from the sale of your shares are $3,500. $3,500 minus your $1,800 purchase price gives you a tidy gross profit of $1,700.

Here is how the tax treatment of your stock profits would look if the sale of your shares is a qualifying disposition:

- You would be taxed at your regular income tax rate on the $2 per share gain you realized by being able to purchase the shares at a discounted price of $18 per share (versus a market price of $20); assuming that you are in the 35% tax bracket, that tax liability would come out to $70 ($2 per share, times 100 shares, multiplied by 35%).

- The additional gain you realized upon the sale of your shares is $15 per share – the difference between your sale price of $35 per share and the non-discounted market price of $20 per share that existed when you bought the stock; that total gain of $1,500 would only be taxed at the much lower capital gains tax rate of 15%, making your tax liability $225 ($15 per share, times 100 shares, multiplied by 15%).

- Your total tax liability would equal $295 ($70 + $225 = $295).

In contrast, if the sale of your stock shares was not a qualifying disposition, then you would be taxed at the 35% income tax rate on the whole profitProfit vs CashUnderstanding the difference between profit vs cash is very important in the finance industry. Profit is defined as revenue less all the expenses of a realized from your stock – $1700. It would make your tax liability on your stock profits $595 ($1,700 multiplied by 35%) – nearly twice as much as your tax liability with a qualifying disposition.

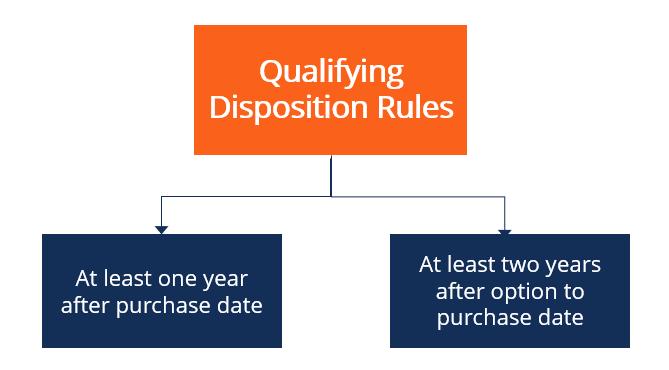

What Qualifies as a Qualifying Disposition?

Since it can obviously make a big difference for you in terms of your tax liability, it is important to know the rules that govern whether the sale of your stock shares meets the requirements for being a qualifying disposition. Two basic rules that determine qualifying dispositions:

- The date of the stock sale must be at least one year or more from the date the stock was purchased.

- The date of the stock sale must be at least two years or more from the date when the option to purchase the stock was granted (when companies offer stock purchase options to employees, the offer period typically extends for quite some time).

Thus, your company may have originally granted you the option to purchase shares at the 10% discount in May 2004, but you did not actually purchase your shares under the terms of the offer until June 2005).

The above conditions must be met for the sale of your stock shares to be deemed a qualifying disposition.

Related Readings

CFI offers the Capital Markets & Securities Analyst (CMSA)®Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Employee Stock Purchase Plan (ESPP)Employee Stock Purchase Plan (ESPP)An employee stock purchase plan (ESPP) refers to a stock program that allows participating employees to purchase their organization's stock

- Stock OptionStock OptionA stock option is a contract between two parties which gives the buyer the right to buy or sell underlying stocks at a predetermined price and within a specified time period. A seller of the stock option is called an option writer, where the seller is paid a premium from the contract purchased by the stock option buyer.

- Deferred Tax Liability/AssetDeferred Tax Liability/AssetA deferred tax liability or asset is created when there are temporary differences between book tax and actual income tax.

- Taxable IncomeTaxable IncomeTaxable income refers to any individual's or business’ compensation that is used to determine tax liability. The total income amount or gross income is used as the basis to calculate how much the individual or organization owes the government for the specific tax period.

-

What is a Stock Option?

A stock option is a contract between two parties that gives the buyer the right to buy or sell underlying stocksStockWhat is a stock? An individual who owns stock in a company is called a shareholder

-

Understanding Taxation: A Comprehensive Guide to Government Revenue

Taxation refers to the fees and financial obligations imposed by a government on its residents. Income taxes are paid in almost all countries around the world. However, taxation applies to all p

invest

- Understanding Downtrends: Definition, Identification & Reversal

- Understanding Net Unrealized Appreciation (NUA) for Employees

- Understanding Non-Assessable Stock: Limited Liability Explained

- Understanding Overweight Stocks: A Comprehensive Guide

- Stock Indexes Explained: A Beginner's Guide to Market Benchmarks

- Stock Valuation: A Comprehensive Guide for Investors

- Stock Float Explained: Understanding Publicly Available Shares

- Stock Splits Explained: What They Are & What They Mean for Investors

- Understanding Qualifying Disposition in Stock Options

-

Understanding Stocks: A Beginner's Guide to Share Ownership

Understanding Stocks: A Beginner's Guide to Share OwnershipWhen a person owns stock in a company, the individual is called a shareholder and is eligible to claim part of the company’s residual assets and earnings (should the company ever have to dissolv...

-

Stock Dividends: Definition, Types & How They Work

Stock Dividends: Definition, Types & How They WorkA stock dividend, a method used by companies to distribute wealth to shareholders, is a dividend payment made in the form of shares rather than cash. Stock dividends are primarily issued in lieu of ca...