Accrued Expenses: Definition, Examples & Accounting Explained

Accrued expense is a concept in accrualAccrual AccountingIn financial accounting, accruals refer to the recording of revenues that a company has earned but has yet to receive payment for, and the accounting that refers to expenses that are recognized when incurred but not yet paid.

In some transactions, cash is not paid or earned yet when the revenues or expenses are incurred. For example, a company pays its February utility bill in March, or delivers its products to customers in May and receives the payment in June. Accrual accounting requires revenues and expenses to be recorded in the accounting period that they are incurred.

Since accrued expenses are expenses incurred before they are paid, they become a company’s liabilities for cash payments in the future. Therefore, accrued expenses are also known as accrued liabilities.

Summary

- Accrued expenses, also known as accrued liabilities, are expenses recognized when they are incurred but not yet paid in the accrual method of accounting.

- Typical accrued expenses include utility, salaries, and goods and services consumed but not yet billed.

- Accrued expenses are recorded in estimated amounts, which may differ from the real cash amount paid or received later.

Accrual Accounting

There are two types of accounting methods: the accrual method and the cash method. The major difference between the two methods is the timing of recording revenues and expenses. In the cash method of accounting, revenues, and expenses are recorded in the reporting period that the cash payment is made. It is a simpler method.

The accrual method of accounting required revenues and expenses to be recorded in the period that they are incurred, regardless of the time of payment or receiving cash. Since the accrued expenses or revenues recorded in that period may differ from the actual cash amount paid or received in the later period, the records are merely an estimate. The accrual method requires appropriate anticipation for revenues and expenses.

Although it is easier to use the cash method of accounting, the accrual method can reveal a company’s financial health more accurately. It allows companies to record their credit and cash sales or payments in the same reporting period when the transactions occur.

Therefore, the accrual method of accounting is more commonly used, especially by public companies. International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP)GAAPGAAP, Generally Accepted Accounting Principles, is a recognized set of rules and procedures that govern corporate accounting and financial both require companies to implement the accrual method.

Understanding Accrued Expenses

Accrued expenses or liabilities occur when expenses take place before the cash is paid. The expenses are recorded in a company’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. as current liabilities most of the time, as the payments are generally due within one year from the transaction date.

Some typical cases of accrued expenses include:

- Goods and services have been consumed, but bills have not yet been received.

- The utility is consumed in one month, and the bill is received in the next month.

- Salaries are not paid to employees until the end of the payment period.

At the end of each recording period, a company should properly estimate the dollar amount for each of its accrued expenses, and then record it as an expense account with a corresponding payable account.

The format of the journal entry is shown below:

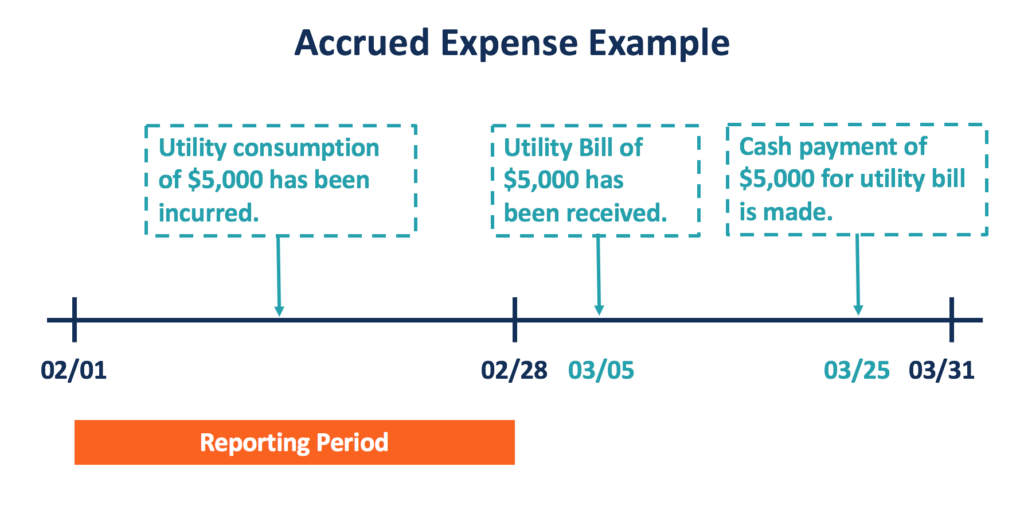

Accrued Expenses – Example

For example, a company consumes $5,000 utility in February. The expense for the utility consumed remains unpaid on the balance day (February 28). The company then receives its bill for the utility consumption on March 05 and makes the payment on March 25.

Under the accrual method of accounting, the entry for the transaction should be recorded in the reporting period of February, as shown below:

On the balance day, the accrued expense of utility is treated as a current liability (Utility Payable) owed to the utility company, and an expense (Utility Expense) incurred by the company in February.

In the reporting period of March, the company should record its cash payment on March 25 for its utility bill. This entry includes a counter account for the utility payable from the previous period and a cash account.

Accrued Expenses and Prepaid Expenses

A related concept under accrual accounting is prepaid expenses. Accrued expenses represent the expenditures incurred before cash is paid, but there are also cases where cash is paid before the expenditures are incurred. Such expenditures are known as prepaid expenses.

Prepaid expenses are a type of asset on the balance sheet, as the goods or services will be received in the future. Like accrued expenses, prepaid expenses are also recorded in the reporting period when they are incurred under the accrual accounting method. Typical examples of prepaid expenses include prepaid insurance premiums, rents, and expected taxes.

In the reporting periodReporting PeriodA reporting period, also known as the accounting period, is a discrete and uniform span of time for which the financial performance and that the cash is paid, the company records a debit in the prepaid asset account and a credit in cash. In the later reporting period that the expenditure is incurred, the firm will record a debit in expense and a credit in the prepaid asset.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Accounting TransactionsAccounting TransactionsAccounting transactions refer to any business activity that results in a direct effect on the financial status and financial statements of the

- Philosophy of AccountingPhilosophy of AccountingThe philosophy of accounting encompasses the general rules, concepts, and ideas surrounding the preparation and auditing of the accounts and

- Prepaid ExpensesPrepaid ExpensesPrepaid expenses represent expenditures that have not yet been recorded by a company as an expense, but have been paid in advance. In other

- Accounting CycleAccounting CycleThe accounting cycle is the holistic process of recording and processing all financial transactions of a company, from when the transaction

-

Expense Ratios: Understanding Investment Fund Fees

An expense ratio is a fee charged by an investment company to manage the shareholders’ funds. Investment companies such as mutual fundsMutual FundsA mutual fund is a pool of money collected from

-

Accrued Expenses: Definition, Examples & Accounting Explained

Accrued expense is a concept in accrualAccrual AccountingIn financial accounting, accruals refer to the recording of revenues that a company has earned but has yet to receive payment for, and the acco

Accounting

- Understanding Discretionary Expenses: Definition & Examples

- Accounting Explained: Understanding Financial Records & Reporting

- Understanding Accounting Income: A Key Financial Metric

- Understanding Accounts Expenses: A Comprehensive Guide

- Understanding Accrued Expenses: A Comprehensive Guide

- Understanding Business Expenses: A Comprehensive Guide

- Understanding Non-Operating Expenses: Definition & Examples

- Understanding Utilities Expense: Definition & Accounting

- Understanding Variable Expenses: A Comprehensive Guide

-

Accrued Expenses and the Income Statement: Understanding the Impact

Accrued Expenses and the Income Statement: Understanding the ImpactIn accounting, not all cash expenditures are expenses for an income statement. Conversely, when using accrual-based accounting, expenses can occur in the income statement without showing any cash paym...

-

Understanding Wage Expense: Definition, Types & Accounting

Understanding Wage Expense: Definition, Types & AccountingWage expense refers to the cost incurred by an organization to compensate employees and contractors for work performed over a specific time period. SummaryWage expense is a type of variable...