Understanding Accrued Expenses: A Comprehensive Guide

Accrued expenses are expenses that are recognized at the time they are incurred, even though cash has not yet been paid. These expensesFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according are paired up against revenue via the matching principle from the GAAP (Generally Accepted Accounting Principles).

For those who are unaware of the matching principle, it states that you record revenues and all related expenses in the accounting period in which they occur. This is true regardless of whether or not cash has actually been received by the seller or paid out by the buyer.

Types of Accrued Expenses

There are different types of accrued expenses. However, in this article, we focus on the more common accrued expenses that you will run into as an accountant from time to time:

- Accrued Salaries and Wages

- Accrued Interest

In demonstrating and showing examples of accrued expenses, we are using MS Excel. If you are unfamiliar with Microsoft’s spreadsheet program, be sure to check out our free Excel crash course.

Accrued Salaries and Wages

This type of accrued expense is very common and occurs regularly within company operations. Following is an example to demonstrate how and when this type of accrued expense may occur.

Example

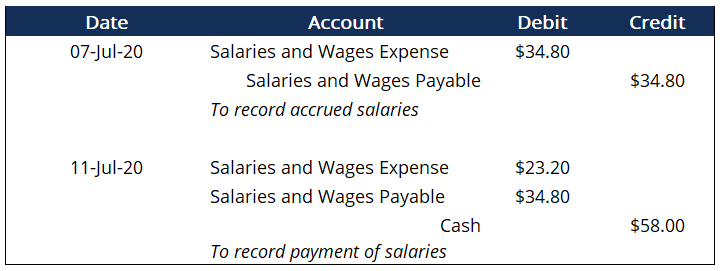

Corporate Finance Institute pays salaries of $58 per day in a 5-day work week every week. The last time employees were paid was on June 30, Friday. Unfortunately, due to statutory holidays occurring in the preceding week (Monday and Tuesday), employees were only paid for Wednesday, Thursday, and Friday. It means management needed to prepare adjusting entries to recognize employees have only been paid three days out of five. This is the entry that management would record:

Notice that on Friday, July 7, management would record the recognition of the accrued salaries expense. This is the salaries that have accrued over the three days, which can be found through some math: (58/5)*3.

Now, when the company reaches the end of their 5-day work week, which lands on Tuesday of next week, July 11, management records the payment of the salaries. This is shown in the second entry by debiting the salaries and wages payable account by the amount that was accrued and debiting the salaries expense account. We also credit cash to demonstrate that cash was paid for salaries. Note that salaries payable is similar to accounts payable.

Accrued Interest

Accrued interest is another type of accrued expense that is common for companies with notes payables. Notes payablesNotes PayableNotes payable are written agreements (promissory notes) in which one party agrees to pay the other party a certain amount of cash. are promissory notes issued by either an individual, banks, or even other companies that obligate the issuing party (the one who must pay it back) to pay back the amount stated by a certain date. Just like earlier with salaries and wages, we use an example to demonstrate what we mean.

Example

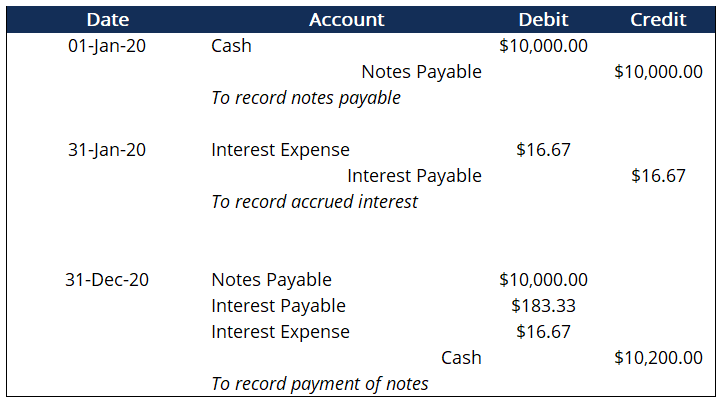

On January 1, Corporate Finance Institute issued a 1-year promissory note to AC Bank. The terms of the promissory note were a $10,000 value along with an annual interest rate of 2%. Because the note was for a term of one year, the maturity date of the note would be December 31 of the present year. These are the journal entries that the company would record:

The very first entry on January 1 is the recording of the issuance of the note. Recall that the note’s face value was $10,000, with an annual interest of 2%. The next entry on February 1 records the accrued interest for the month of January. We record interest every month to recognize the monthly interest that we are obligated to pay. All this monthly interest eventually adds up to the annual interest amount at the end of the year.

To record the monthly interest expenseInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also, we take the face value of $10,000, multiply it by the annual interest rate of 2%. This gives us $200, which is our annual interest. We then divide this annual interest by 12 (200/12), and we end up with $16.67. This will be the monthly interest that we record every month leading up to the last month, when we actually pay the interest due.

The last entry represents the payment of the note, along with all interest that has accrued over the life of the note. Again, we see that there is a debit of interest payableInterest PayableInterest Payable is a liability account shown on a company’s balance sheet that represents the amount of interest expense that has accrued along with a debit of interest expense. This is done because we are paying off all of the accrued interest along with the last bit of interest that accrues in December. An important thing to note is that debits must always equal credits. Otherwise, issues can arise in your financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are, especially in the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. and income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or, because these two statements are closely related to one another.

Learn More

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)®Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Adjusting EntriesAdjusting EntriesThis guide to adjusting entries covers deferred revenue, deferred expenses, accrued expenses, accrued revenues and other adjusting journal

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Current LiabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the

- Depreciation ExpenseCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the

- Financial Modeling CertificationBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!

-

Understanding Non-Cash Expenses: A Comprehensive Guide

Non-cash expenses appear on an income statement because accounting principlesIB Manual – Accounting PrinciplesAccounting Principles for Investment Banking Analysts. A fundamental understanding o

-

Understanding Fixed Income Securities: A Comprehensive Guide

Fixed income securities are a type of debt instrument that provides returns in the form of regular, or fixed, interest payments and repayments of the principal when the security reaches maturity. The

Accounting

- Understanding Competitive Interest Rates: What You Need to Know

- Accrued vs. Regular Interest: Understanding the Difference

- Understanding Accounts Expenses: A Comprehensive Guide

- Accrued Expenses: Definition, Examples & Accounting Explained

- Accrued Interest Explained: Accounting & Financial Definition

- Understanding Administrative Expenses: A Comprehensive Guide

- Understanding Maintenance Expenses: A Comprehensive Guide

- Understanding Operating Expenses (OPEX): A Comprehensive Guide

- Understanding Prepaid Expenses: Definition & Accounting

-

Understanding Operating Expenses (OpEx): A Comprehensive Guide

Understanding Operating Expenses (OpEx): A Comprehensive GuideWhat Are Operating Expenses? Operating expenses are expenditures directly related to d...

-

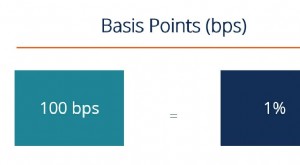

Basis Points (BPS): Understanding Interest Rate Measurement

Basis Points (BPS): Understanding Interest Rate MeasurementIn finance, Basis Points (BPS) are a unit of measurement equal to 1/100th of 1 percent. BPS are used for measuring interest rates, the yield of a fixed-income securityFixed Income Bond Term...