Contra Asset Accounts: Definition & Accounting Explained

In bookkeeping, a contra asset account is an asset account in which the natural balance of the account will either be a zero or a credit (negative) balance. The account offsets the balance in the respective asset account that it is paired with on the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting..

Normal asset accounts have a debit balance, while contra asset accounts are in a credit balance. Therefore, a contra asset can be regarded as a negative asset account. Offsetting the asset account with its respective contra asset account shows the net balance of that asset.

Examples of Contra Assets

Common examples of contra assets include:

- Accumulated depreciationAccumulated DepreciationAccumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use.

- Allowance for doubtful accountsAllowance for Doubtful AccountsThe allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable. The amount represents the value of accounts receivable that a company does not expect to receive payment for.

- Reserve for obsolete inventory

Reasons to Show Contra Accounts on the Balance Sheet

By reporting contra asset accounts on the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting., users of financial statements can learn more about the assets of a company. For example, if a company just reported equipment at its net amount, users would not be able to observe the purchase price, the amount of depreciation attributed to that equipment, and the remaining useful life. Contra asset accounts allow users to see how much of an asset was written off, its remaining useful life, and the value of the asset.

Now let’s focus our attention on the two most common contra assets – accumulated depreciation and allowance for doubtful accounts.

Contra Asset – Accumulated Depreciation

Accumulated depreciation is a contra asset account used to record the amount of depreciation to date on a fixed asset. Examples of fixed assetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and include buildings, machinery, office equipment, furniture, vehicles, etc. The accumulated depreciation account appears on the balance sheet and reduces the gross amount of fixed assets.

Example of Accumulated Depreciation

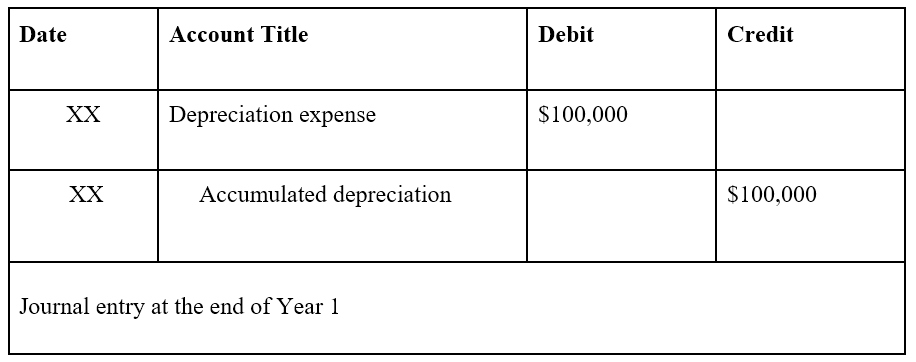

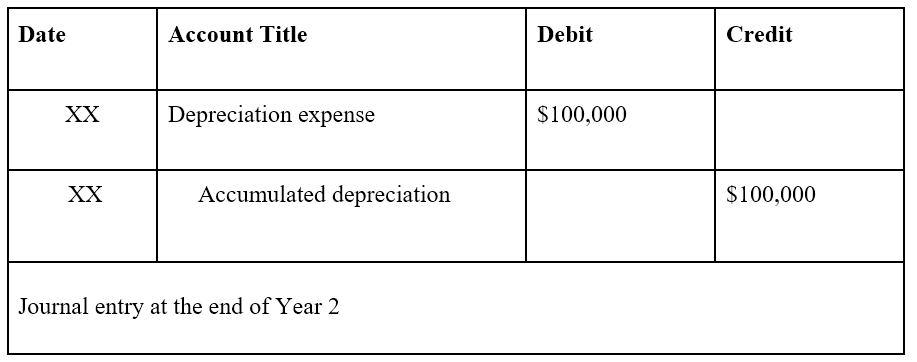

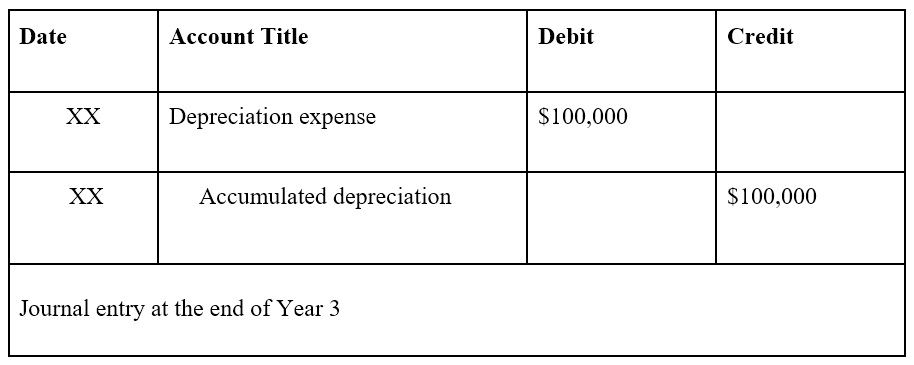

Assume Company A purchases a machine for $300,000. The company estimates that the machine’s useful life is three years with no salvage value and will apply a straight-line depreciation methodStraight Line DepreciationStraight line depreciation is the most commonly used and easiest method for allocating depreciation of an asset. With the straight line to the machine. The journal entries will look as follows:

On the balance sheet, accumulated depreciation would increase by every year to reduce the value of the machine. Therefore:

- At the end of year 1, the net value of the machine would be $300,000 – $100,000 in accumulated depreciation = $200,000.

- At the end of year 2, the net value of the machine would be $300,000 – $200,000 in accumulated depreciation = $100,000.

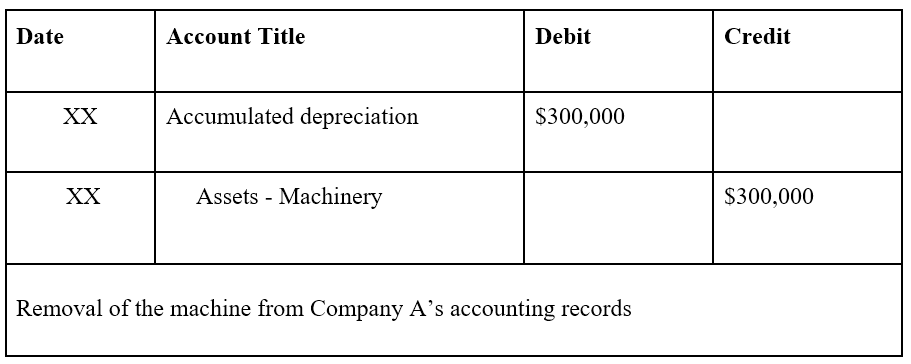

- At the end of year 3, the net value of the machine would be $300,000 – $300,000 in accumulated depreciation = $0.

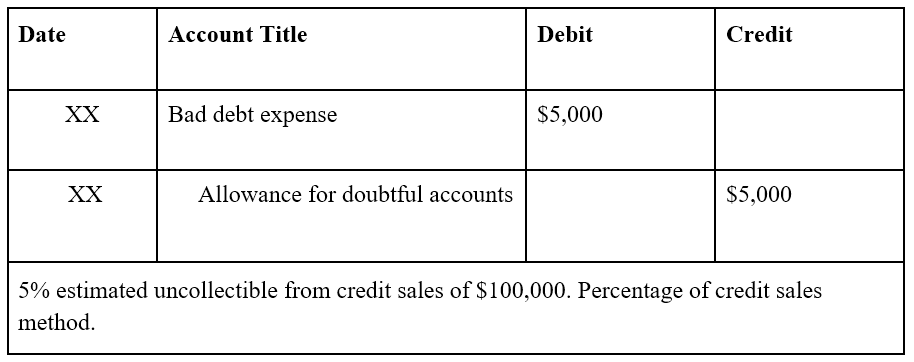

Allowance for Doubtful Accounts

Allowance for doubtful accounts (ADA) is a contra asset account used to create an allowance for customers that are not expected to pay the money owed for purchased goods or services. The allowance for doubtful accounts appears on the balance sheet and reduces the amount of receivables.

Example of Allowance for Doubtful Accounts

For example, Company A uses the percentage of credit sales method and estimates that 5% of credit sales will default. The company reported credit sales of $100,000. The journal entry would look as follows:

On the balance sheet, allowance for doubtful accounts reduces the amount of receivables. For example, if Company A reported receivables of $100,000, the journal entry above would reduce the amount of receivables by $5,000. $100,000 – $5,000 (allowance for doubtful accounts) = $95,000 in net receivables.

Related Readings

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Three Financial StatementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are

- PP&E (Property, Plant & Equipment)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

- Straight-Line Depreciation MethodStraight Line DepreciationStraight line depreciation is the most commonly used and easiest method for allocating depreciation of an asset. With the straight line

- Credit SalesCredit SalesCredit sales refer to a sale in which the amount owed will be paid at a later date. In other words, credit sales are purchases made by

-

Accelerated Depreciation: A Comprehensive Guide

Accelerated depreciation is a depreciation methodDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of year

-

Accounting vs. Tax Depreciation: Key Differences Explained

Before we discuss accounting depreciation vs tax depreciation, let us first talk about depreciation itself. Essentially, depreciation is a method of allocating the cost of a tangible asset over severa

Accounting

- UTMA Account: A Comprehensive Guide for Custodians

- Understanding Account Balances: A Comprehensive Guide

- Understanding Accumulated Depreciation: A Comprehensive Guide

- Understanding Due to Account: A Comprehensive Guide

- Fully Depreciated Assets: Definition, Causes & Implications

- Understanding Leases: Types, Classifications, and Key Concepts

- Straight-Line Depreciation: Definition, Calculation & Example

- Tax Depreciation Explained: A Comprehensive Guide for Taxpayers

- Asset Management Accounts: A Comprehensive Guide

-

Margin Accounts: Borrowing to Invest & Increase Buying Power

Margin Accounts: Borrowing to Invest & Increase Buying PowerA margin account refers to a type of brokerage account that investors use where they can borrow funds to purchase financial products. Investors are required to pay a monthly interest rate on the amoun...

-

Wrap Accounts: A Comprehensive Guide for Investors

Wrap Accounts: A Comprehensive Guide for InvestorsA wrap account refers to an investment account that is managed by a broker for a flat annual fee. The flat annual fee, which ranges from 1% to 3% of assets under management (AUM)Assets Under Managemen...