Fully Depreciated Assets: Definition, Causes & Implications

A fully depreciated asset is an accounting term used to describe an asset that is worth the same as its salvage valueSalvage ValueSalvage value is the estimated amount that an asset is worth at the end of its useful life. Salvage value is also known as scrap value. An asset can become fully depreciated in two ways:

- The asset has reached the end of its useful life.

- There has been an impairment in the asset and it has been written down to zero.

If the asset’s accumulated depreciationAccumulated DepreciationAccumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use. is equivalent to the asset’s original cost, then it is classified as fully depreciated. If an impairment charge equal to the asset’s cost is incurred, then the asset is immediately fully depreciated.

The depreciation expense for accounting does not fully reflect the actual used value of the equipment. It is more of an approximation that gives an estimate of the actual value used. For this reason, there are different methods to estimate the depreciation expense.

When using more conservative accounting practices,IFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world it is typical to impose a more aggressive depreciation schedule and recognize expenses earlier. Sometimes, a fully depreciated asset can still provide value to a company. In such a case, the operating profits of a company will increase because no depreciation expenses will be recognized.

Whenever the asset is no longer used by a company or is sold, the asset is removed from the company’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting..

Accounting for Fully Depreciated Assets

Since property, plant, and equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex, and accumulated depreciation are balance sheet items, the full depreciation of an asset will affect the company’s balance sheet. At the same time, the income statement is impacted because that is where the depreciation expense is recorded. There are two cases for accounting reporting for fully depreciated assets: the fully depreciated asset is still in production use or it is disposed of.

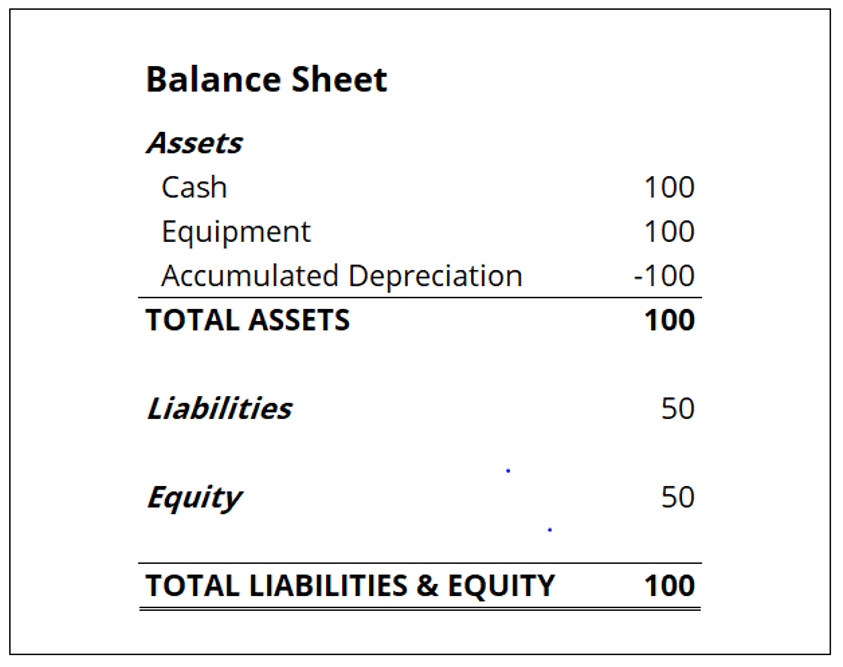

If the asset is still used in the company’s operations, the asset’s account and accumulated depreciation will still be reported on the company’s balance sheet. The reported asset’s value and accumulated depreciation will be equal, but no entry will be required until the asset is disposed of. On the income statement, the operating profit is likely to increase because the depreciation expense will no longer be recorded on the income statement.

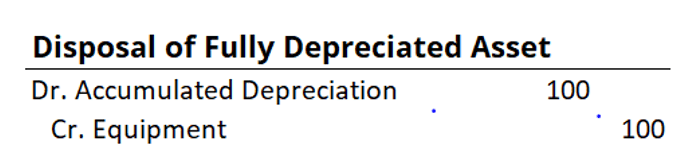

If the fully depreciated asset is disposed of, the asset’s value and accumulated depreciation will be written off from the balance sheet. In such a scenario, the effect on the income statement will be the same as if no depreciation expense happened.

The accounting treatment for the disposal of a completely depreciated asset is a debit to the account for the accumulated depreciation and a credit for the asset account.

Additional Resources

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program and other corporate finance training online. To advance your career, check out the additional CFI resources below:

- Accelerated DepreciationAccelerated DepreciationAccelerated depreciation is a depreciation method in which a capital asset reduces its book value at a faster (accelerated) rate than it would

- Depreciation MethodsDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits.

- Depreciation ScheduleDepreciation ScheduleA depreciation schedule is required in financial modeling to link the three financial statements (income, balance sheet, cash flow) in Excel.

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

Book Value vs. Fair Value: Understanding the Difference

In accounting and finance, it is important to understand the differences between book value vs fair value. Both concepts are used in the valuation of an asset, but they refer to different aspects

-

Understanding Lease Classifications: Operating vs. Capital Leases

Lease classifications include operating leases and capital leases. A lease is a type of transaction undertaken by a company to have the right to use an asset. In a direct purchase, a company will simp

Accounting

- Accelerated Depreciation: A Comprehensive Guide

- Accounting vs. Tax Depreciation: Key Differences Explained

- Understanding Accumulated Depreciation: A Comprehensive Guide

- Understanding Allowed Depreciation: Tax Deductions for Businesses

- Contra Asset Accounts: Definition & Accounting Explained

- Depreciated Cost Explained: Calculation & Importance

- Understanding Leases: Types, Classifications, and Key Concepts

- Straight-Line Depreciation: Definition, Calculation & Example

- Tax Depreciation Explained: A Comprehensive Guide for Taxpayers

-

Non-Financial Assets: Definition, Examples & Value

Non-Financial Assets: Definition, Examples & ValueA non-financial asset refers to an asset that is not traded on the financial markets, and its value is derived from its physical characteristics rather than from contractual claims. Examples of non-fi...

-

Synthetix: A Decentralized Platform for Synthetic Asset Trading

Synthetix: A Decentralized Platform for Synthetic Asset TradingTrading on exchanges has been traditionally dominated by major financial centres and exchanges, such as the London or New York stock exchanges. It has been hard to trade without going through these la...