Straight-Line Depreciation: Definition, Calculation & Example

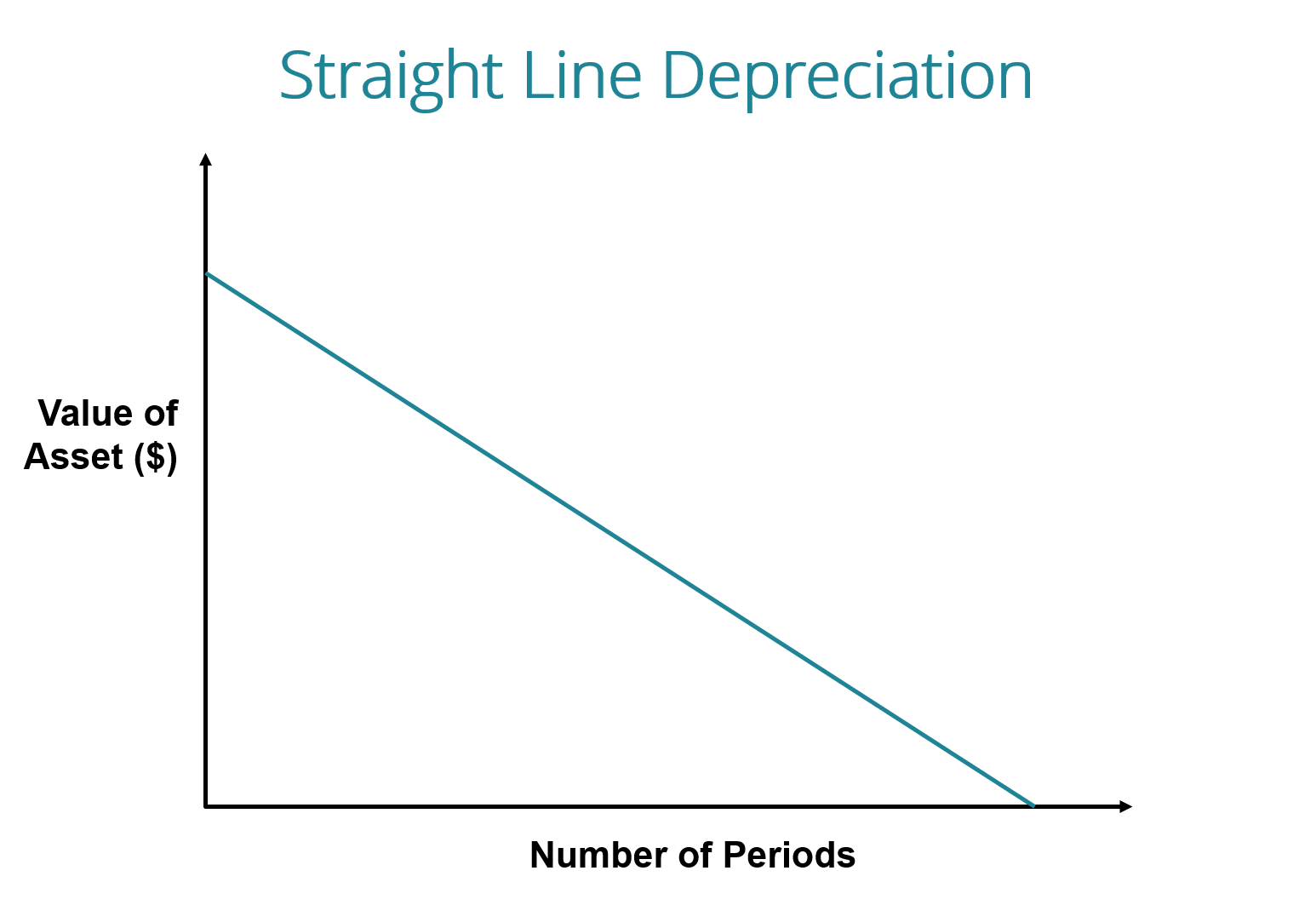

With the straight line depreciation method, the value of an asset is reduced uniformly over each period until it reaches its salvage valueSalvage ValueSalvage value is the estimated amount that an asset is worth at the end of its useful life. Salvage value is also known as scrap value. Straight line depreciation is the most commonly used and straightforward depreciation methodDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in. for allocating the cost of a capital assetTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and. It is calculated by simply dividing the cost of an asset, less its salvage value, by the useful life of the asset.

Image: CFI’s Free Accounting Course.

Straight Line Depreciation Formula

The straight line depreciation formula for an asset is as follows:

Where:

Cost of the asset is the purchase price of the asset

Salvage value is the value of the asset at the end of its useful life

Useful life of asset represents the number of periods/years in which the asset is expected to be used by the company

Additionally, the straight line depreciation rate can be calculated as follows:

How to Calculate Straight Line Depreciation

The straight line calculation steps are:

- Determine the cost of the asset.

- Subtract the estimated salvage value of the asset from the cost of the asset to get the total depreciable amount.

- Determine the useful life of the asset.

- Divide the sum of step (2) by the number arrived at in step (3) to get the annual depreciationDepreciation ScheduleA depreciation schedule is required in financial modeling to link the three financial statements (income, balance sheet, cash flow) in Excel. amount.

Straight Line Example

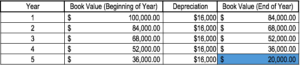

Company A purchases a machine for $100,000 with an estimated salvage valueSalvage ValueSalvage value is the estimated amount that an asset is worth at the end of its useful life. Salvage value is also known as scrap value of $20,000 and a useful life of 5 years.

The straight line depreciation for the machine would be calculated as follows:

- Cost of the asset: $100,000

- Cost of the asset – Estimated salvage value: $100,000 – $20,000 = $80,000 total depreciable cost

- Useful life of the asset: 5 years

- Divide step (2) by step (3): $80,000 / 5 years = $16,000 annual depreciation amount

Therefore, Company A would depreciate the machine at the amount of $16,000 annually for 5 years.

The depreciation rate can also be calculated if the annual depreciation amount is known. The depreciation rate is the annual depreciation amount / total depreciable cost. In this case, the machine has a straight-line depreciation rate of $16,000 / $80,000 = 20%.

Note how the book value of the machine at the end of year 5 is the same as the salvage value. Over the useful life of an asset, the value of an asset should depreciate to its salvage value.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Other Methods of Depreciation

In addition to straight line depreciation, there are also other methods of calculating depreciationDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits. of an asset. Different methods of asset depreciation are used to more accurately reflect the depreciation and current value of an asset. A company may elect to use one depreciation method over another in order to gain tax or cash flow advantages.

1. Double-declining balance method

The double-declining balance method is a form of accelerated depreciation. It means that the asset will be depreciated faster than with the straight line method. The double-declining balance method results in higher depreciation expenses in the beginning of an asset’s life and lower depreciation expenses later. This method is used with assets that quickly lose value early in their useful life. A company may also choose to go with this method if it offers them tax or cash flow advantages.

2. Units of production method

The units of production method is based on an asset’s usage, activity, or units of goods produced. Therefore, depreciation would be higher in periods of high usage and lower in periods of low usage. This method can be used to depreciate assets where variation in usage is an important factor, such as cars based on miles driven or photocopiers on copies made.

Video Explanation of How Depreciation Works

Below is a video tutorial explaining how depreciation works and how it impacts a company’s three financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are.

The Practicality of Straight Line Depreciation

Accountants use the straight line depreciation method because it is the easiest to compute and can be applied to all long-term assets. However, the straight line method does not accurately reflect the difference in usage of an asset and may not be the most appropriate value calculation method for some depreciable assets.

For example, due to rapid technological advancements, a straight line depreciation method may not be suitable for an asset such as a computer. A computer would face larger depreciation expenses in its early useful life and smaller depreciation expenses in the later periods of its useful life, due to the quick obsolescence of older technology. It would be inaccurate to assume a computer would incur the same depreciation expense over its entire useful life.

Related Reading

Thank you for reading this guide to the most common type of depreciation – straight line. CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification. To prepare for the FMVA curriculum, these additional CFI resources will be helpful:

- Depreciation ExpenseDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in.

- Accumulated DepreciationAccumulated DepreciationAccumulated depreciation is the total amount of depreciation expense allocated to a specific asset since the asset was put into use.

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Property, Plant & Equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

-

Lessor vs. Lessee: Understanding Lease Agreements

There are two main parties in a lease agreement, and every finance professionalFP&A AnalystBecome an FP&A Analyst at a corporation. We outline the salary, skills, personality, and training you

-

Listed Property Explained: Tax Implications & Business Use

Listed property is a specific type of depreciable asset that is primarily used as a productive asset for business purposes. To qualify as listed property, the property should be used for over 50% of t

Accounting

- Diminishing Balance vs. Straight-Line Depreciation: A Comprehensive Comparison

- Understanding Horizontal Lines in Technical Analysis & Geometry

- Understanding Accumulated Depreciation: A Comprehensive Guide

- Contra Asset Accounts: Definition & Accounting Explained

- Fully Depreciated Assets: Definition, Causes & Implications

- Understanding Leases: Types, Classifications, and Key Concepts

- Straight-Line Depreciation: Understanding the Basics

- Tax Depreciation Explained: A Comprehensive Guide for Taxpayers

- Straight-Line Depreciation: A Simple Guide for Businesses

-

Historical Cost Accounting: Definition & Importance

Historical Cost Accounting: Definition & ImportanceIn accounting, the historical cost of an asset refers to its purchase price or its original monetary value. Based on the historical cost principle, the transactions of a business tend to be recorded a...

-

Impaired Assets: Definition, Recognition, and Accounting Standards

Impaired Assets: Definition, Recognition, and Accounting StandardsAn impaired asset is an accounting term that describes an asset with a recoverable value or fair market valueFair Market ValueThe fair market value (of a good or service being exchanged) refers to the...