Understanding the Fraud Triangle: Opportunity, Incentive, and Rationalization

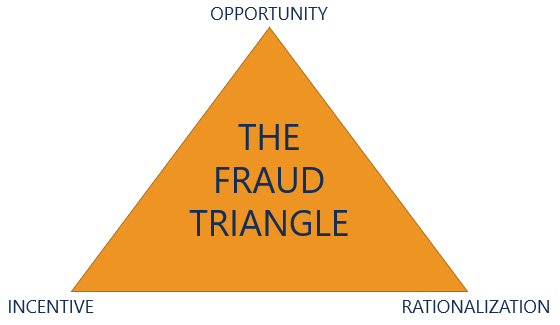

The fraud triangle is a framework commonly used in auditing to explain the reason behind an individual’s decision to commit fraud. The fraud triangle outlines three components that contribute to increasing the risk of fraud: (1) opportunity, (2) incentive, and (3) rationalization.

Summary

- The fraud triangle is a framework used to explain the reason behind an individual’s decision to commit fraud.

- The fraud triangle consists of three components: (1) Opportunity, (2) Incentive, and (3) Rationalization.

- Fraud refers to the deception that is intentional and caused by an employee or organization for personal gain.

What is Fraud?

The fraud triangle is used to explain the reason behind a fraud. However, what exactly is fraud?

Fraud refers to a deception that is intentional and caused by an employee or organizationTypes of OrganizationsThis article on the different types of organizations explores the various categories that organizational structures can fall into. Organizational structures for personal gain. In other words, fraud is a deceitful activity used to gain an advantage or generate an illegal profit. Also, the illegal act benefits the perpetrator and harms other parties involved.

For example, an employee that pockets cash from the company’s register is committing fraud. The employee would benefit from getting additional cash at the expense of the company.

Below, we discuss the components of the fraud triangle.

The Fraud Triangle – Opportunity

Opportunity refers to circumstances that allow fraud to occur. In the fraud triangle, it is the only component that a company exercises complete control over. Examples that provide opportunities for committing fraud include:

1. Weak internal controls

Internal controls are processes and procedures implemented to ensure the integrity of accounting and financial information. Weak internal controls such as poor separation of duties, lack of supervision, and poor documentation of processes give rise to opportunities for fraud.

2. Poor tone at the top

Tone at the top Tone at the TopTone at the top, commonly referred to in auditing, is used to define a company's management and board of director’s leadership and their commitment to being honest and ethical. The tone at the top sets forth a company’s cultural environment and corporate values.refers to upper management and the board of directors’ commitment to being ethical, showing integrity, and being honest – a poor tone at the top results in a company that is more susceptible to fraud.

3. Inadequate accounting policies

Accounting policies refer to how items on the financial statements are recorded. Poor (inadequate) accounting policies may provide an opportunity for employees to manipulate numbers.

The Fraud Triangle – Incentive

Incentive, alternatively called pressure, refers to an employee’s mindset towards committing fraud. Examples of things that provide incentives for committing fraud include:

1. Bonuses based on a financial metric

Common financial metrics used to assess the performance of an employee are revenues and net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through. Bonuses that are based on a financial metric create pressure for employees to meet targets, which, in turn, may cause them to commit fraud to achieve the objective.

2. Investor and analyst expectations

The need to meet or exceed investor and analyst expectations to ensure stock prices are maintained or increased can create pressure to commit fraud.

3. Personal incentives

Personal incentives may include wanting to earn more money, the need to pay personal bills, a gambling addiction, etc.

The Fraud Triangle – Rationalization

Rationalization refers to an individual’s justification for committing fraud. Examples of common rationalizations that fraud committers use include:

1. “They treated me wrong”

An individual may be spiteful towards their manager or employer and believe that committing fraud is a way of getting payback.

2. “Upper management is doing it as well”

A poor tone at the top may cause an individual to follow in the footsteps of those higher in the corporate hierarchyCorporate StructureCorporate structure refers to the organization of different departments or business units within a company. Depending on a company’s goals and the industry.

3. “There is no other solution”

An individual may believe that they might lose everything (for example, losing a job) unless they commit fraud.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below:

- Audit MaterialityMateriality Threshold in AuditsThe materiality threshold in audits refers to the benchmark used to obtain reasonable assurance that an audit does not detect any material

- Cash LarcenyCash LarcenyCash larceny refers to the act of stealing cash that has already been recorded in the books of accounts during a specific period. This fraud is perpetrated

- Forensic AccountingForensic AccountingForensic accounting is the investigation of fraud or financial manipulation by performing extremely detailed research and analysis of financial information. Forensic accountants are often hired to prepare for litigation related to insurance claims, insolvency, embezzlement, fraud - any type of financial theft.

- Key Performance Indicators (KPIs)Key Performance Indicators (KPIs)Key Performance Indicators (KPIs) are metrics used to periodically track and evaluate the performance of an organization toward the achievement of specific goals. They are also used to gauge the overall performance of a company

-

Operating Ratio: Definition, Calculation & Importance

The operating ratio is a measure of efficiency that is used by management to determine day-to-day operational performance. This metric compares operating expenses, also known as OPEX, to net sales. Th

-

Understanding the Overnight Interest Rate: A Comprehensive Guide

The overnight rate refers to the interest rate that depository institutions (e.g., banks or credit unionsCredit UnionA credit union is a type of financial organization that is owned and governed by it

Accounting

- Corporate Fraud: Definition, Types, and Detection

- Dow 30 Explained: Understanding the Dow Jones Industrial Average

- Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]

- Understanding the Accounting Equation: Assets = Liabilities + Equity

- Understanding Average Inventory: Definition & Calculation

- Understanding Unemployment Fraud: Risks and Prevention

- Nifty 50: History, Significance & Key Stocks - A Comprehensive Guide

- Protect Yourself: Identifying and Addressing Unemployment Fraud

- Fraud Alerts: Understanding Identity Theft Protection

-

Modigliani-Miller Theorem: Understanding Capital Structure & Firm Value

Modigliani-Miller Theorem: Understanding Capital Structure & Firm ValueThe M&M Theorem, or the Modigliani-Miller Theorem, is one of the most important theorems in corporate finance. The theorem was developed by economists Franco Modigliani and Merton Miller in ...

-

Understanding NCREIF: Real Estate Investment Performance Data

Understanding NCREIF: Real Estate Investment Performance DataNCREIF is an acronym of the National Council of Real Estate Investment Fiduciaries, and it operates as a non-profit entity. The main aim of the NCREIF is to inform concerned parties on the actual perf...