Modigliani-Miller Theorem: Understanding Capital Structure & Firm Value

The M&M Theorem, or the Modigliani-Miller Theorem, is one of the most important theorems in corporate finance. The theorem was developed by economists Franco Modigliani and Merton Miller in 1958. The main idea of the M&M theory is that the capital structureCapital StructureCapital structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. A firm's capital structure of a company does not affect its overall value.

The first version of the M&M theory was full of limitations as it was developed under the assumption of perfectly efficient markets, in which the companies do not pay taxes, while there are no bankruptcy costs or asymmetric informationAsymmetric InformationAsymmetric information is, just as the term suggests, unequal, disproportionate, or lopsided information. It is typically used in reference to some type of business deal or financial arrangement where one party possesses more, or more detailed, information than the other.. Subsequently, Miller and Modigliani developed the second version of their theory by including taxes, bankruptcy costs, and asymmetric information.

The M&M Theorem in Perfectly Efficient Markets

This is the first version of the M&M Theorem with the assumption of perfectly efficient markets. The assumption implies that companies operating in the world of perfectly efficient markets do not pay any taxes, the trading of securities is executed without any transaction costs, bankruptcyBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts is possible but there are no bankruptcy costs, and information is perfectly symmetrical.

Proposition 1 (M&M I):

Where:

- VU = Value of the unlevered firm (financing only through equity)

- VL = Value of the levered firm (financing through a mix of debt and equity)

The first proposition essentially claims that the company’s capital structure does not impact its value. Since the value of a company is calculated as the present value of future cash flows, the capital structure cannot affect it. Also, in perfectly efficient markets, companies do not pay any taxes. Therefore, the company with a 100% leveraged capital structure does not obtain any benefits from tax-deductible interest payments.

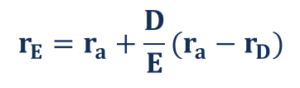

Proposition 2 (M&M I):

Where:

- rE = Cost of levered equity

- ra = Cost of unlevered equity

- rD = Cost of debt

- D/E = Debt-to-equity ratio

The second proposition of the M&M Theorem states that the company’s cost of equityCost of EquityCost of Equity is the rate of return a shareholder requires for investing in a business. The rate of return required is based on the level of risk associated with the investment is directly proportional to the company’s leverage level. An increase in leverage level induces higher default probability to a company. Therefore, investors tend to demand a higher cost of equity (return) to be compensated for the additional risk.

M&M Theorem in the Real World

Conversely, the second version of the M&M Theorem was developed to better suit real-world conditions. The assumptions of the newer version imply that companies pay taxes; there are transaction, bankruptcy, and agency costs; and information is not symmetrical.

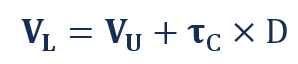

Proposition 1 (M&M II):

Where:

- tc = Tax rate

- D = Debt

The first proposition states that tax shields that result from the tax-deductible interest payments make the value of a levered company higher than the value of an unlevered company. The main rationale behind the theorem is that tax-deductible interest payments positively affect a company’s cash flows. Since a company’s value is determined as the present value of the future cash flows, the value of a levered company increases.

Proposition 2 (M&M II):

The second proposition for the real-world condition states that the cost of equity has a directly proportional relationship with the leverage level.

Nonetheless, the presence of tax shields affects the relationship by making the cost of equity less sensitive to the leverage level. Although the extra debt still increases the chance of a company’s default, investors are less prone to negatively reacting to the company taking additional leverage, as it creates the tax shields that boost its value.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Corporate Finance OverviewCorporate Finance OverviewCorporate finance deals with the capital structure of a corporation, including its funding and the actions that management takes to increase the value of

- Little’s LawLittle’s LawLittle’s Law is a theorem that determines the average number of items in queuing systems, based on the average waiting time of an item within a system and

- Unlevered Cost of CapitalUnlevered Cost of CapitalUnlevered cost of capital is the theoretical cost of a company financing itself for implementation of a capital project, assuming no debt. Formula, examples. The unlevered cost of capital is the implied rate of return a company expects to earn on its assets, without the effect of debt. WACC assumes the current capital

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

-

Understanding Total Leverage: A Comprehensive Guide

The degree of total leverage is a ratio that compares the rate of change a company experiences in earnings per share (EPS)Earnings Per Share (EPS)Earnings per share (EPS) is a key metric used to deter

-

Understanding the Envy Ratio in Private Equity

In private equity, the envy ratio is a ratio that shows the price paid by investors in relation to the price paid by the management team for their respective shares of the company’s common equit

finance

- Acid-Test Ratio: Understanding Your Company's Short-Term Liquidity

- Understanding the Earnings Multiplier (P/E Ratio): A Comprehensive Guide

- Understanding the IPO Process: A Comprehensive Guide

- Skin in the Game: Understanding Risk & Accountability

- Clientele Effect: How Investor Preferences Impact Stock Prices

- Understanding the Icahn Effect: How Activist Investing Impacts Stock Prices

- Understanding Lock-Up Periods After an IPO: A Comprehensive Guide

- Understanding the Primary Market: A Comprehensive Guide

- Understanding the Stock Market: A Beginner's Guide

-

Financial Leverage: Definition, Calculation & Impact on Profitability

Financial Leverage: Definition, Calculation & Impact on ProfitabilityThe degree of financial leverage is a financial ratio that measures the sensitivity in fluctuations of a company’s overall profitability to the volatility of its operating income caused by chang...

-

Understanding Degree of Operating Leverage (DOL): A Comprehensive Guide

Understanding Degree of Operating Leverage (DOL): A Comprehensive GuideThe degree of operating leverage (DOL) is a financial ratio that measures the sensitivity of a company’s operating incomeOperating IncomeOperating income is the amount of revenue left after dedu...