Goodwill in Accounting: Definition & Value

In accounting, goodwill is an intangible assetIntangible AssetsAccording to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible assets. The concept of goodwill comes into play when a company looking to acquire another company is willing to pay a price premium over the fair market value of the company’s net assets.

The elements or factors that a company is paying extra for or that are represented as goodwill are things such as a company’s good reputation, a solid (loyal) customer or client base, brand identity and recognition, an especially talented workforce, and proprietary technology. These things are, in fact, valuable assets of a company. However, they are neither tangible (physical) assets nor can their value be precisely quantified.

Under US GAAP and IFRS StandardsIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world, goodwill is an intangible asset with an indefinite life and thus does not need to be amortized. However, it needs to be evaluated for impairment yearly, and only private companies may elect to amortize goodwill over a 10-year period.

Accounting vs. Economic Goodwill

Goodwill is sometimes separately categorized as economic, or business, goodwill and goodwill in accounting, but to speak as if these were two separate things is an artificial and misleading construct. What is referred to as “accounting goodwill” is really just the recognition in the accounting of a company’s “economic goodwill.”

Accounting goodwill is sometimes defined as an intangible asset that is created when a company purchases another company for a price higher than the fair market value of the target company’s net assets. But referring to the intangible asset as being “created” is misleading – an accounting journal entry is created, but the intangible asset already exists. The entry of “goodwill” in a company’s financial statements – it appears in the listing of assets on a company’s balance sheet – is not really the creation of an asset but merely the recognition of its existence.

Economic, or business, goodwill is defined as previously noted: an intangible asset – for example, strong brand identity or superior customer relations – that provides a company with competitive advantagesCompetitive AdvantageA competitive advantage is an attribute that enables a company to outperform its competitors. It allows a company to achieve superior margins in the marketplace. Both the existence of this intangible asset, as well as an indication or estimate of its value, is often drawn from examining a company’s return on assets ratio.

Warren Buffett used California-based See’s Candies as an example of this. See’s consistently earned approximately a two million dollar annual net profit with net tangible assetsNet Tangible AssetsNet Tangible Assets (NTA) is the value of all physical ("tangible") assets minus all liabilities in a business. In other words, NTA are the of only eight million dollars. Because a 25% return on assets is exceptionally high, the inference is that part of the company’s profitability was due to the existence of substantial goodwill assets.

The inference of contributing intangible assets was borne out as being based in fact, as See’s was widely recognized in the industry as enjoying a significant edge over its competitors by virtue of its overall favorable reputation and, specifically, thanks to its outstanding customer service relations.

The following excerpt from Warren Buffett’s 1983 Berkshire Hathaway shareholder letter explains and indicates the estimate of the value of goodwill:

“Businesses logically are worth far more than net tangible assets when they can be expected to produce earnings on such assets considerably in excess of market rates of return. The capitalized value of this excess return is economic goodwill.”

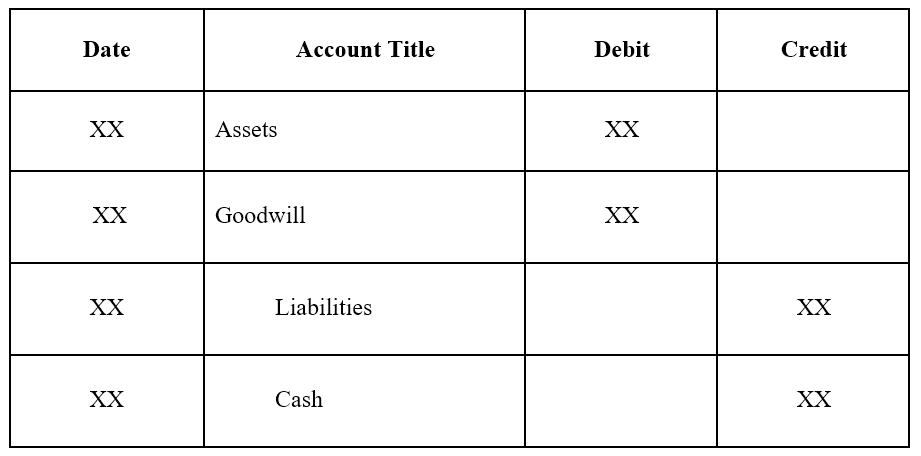

Accounting for Goodwill (Journal Entries)

The journal entry is as follows:

Purchase of a Company:

To understand it in more depth, let’s look at an example.

Accounting Example

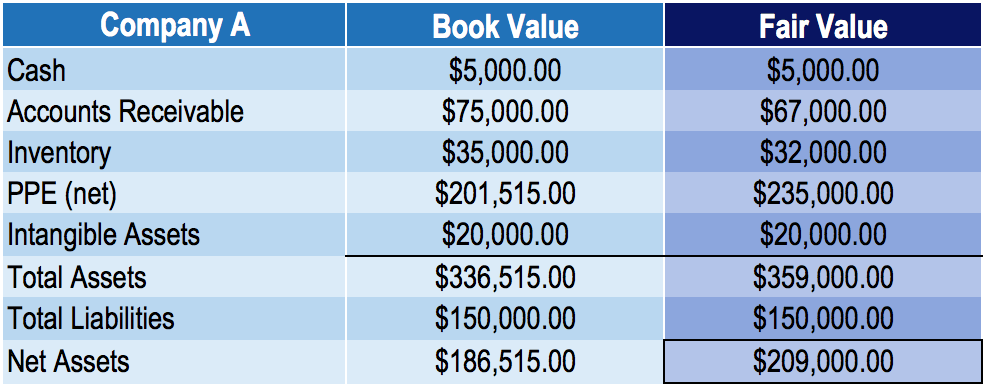

Company A reports the following amounts:

The fair value differs from book value in the example above because:

- Fair value accounts receivable is lower than book value due to uncollectible accounts.

- Fair value inventory is lower than book value due to obsolescence.

- Fair value PPE is higher than book value due to depreciation being greater than the decline in PPE fair value.

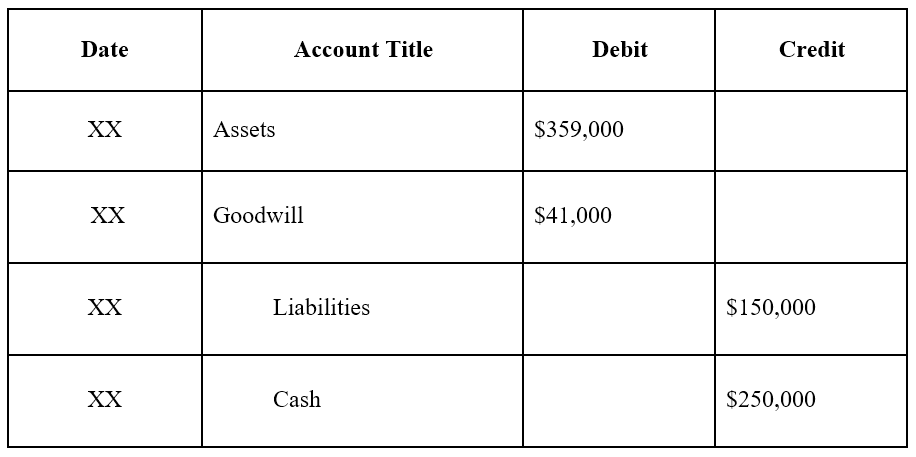

If Company B purchases Company A for $250,000, the amount of economic goodwill “created” would be the purchase price minus the fair market value of net assets: $250,000 – $209,000 = $41,000.

The journal entry for the purchasing company, Company B, would be as follows:

Goodwill in Financial Modeling

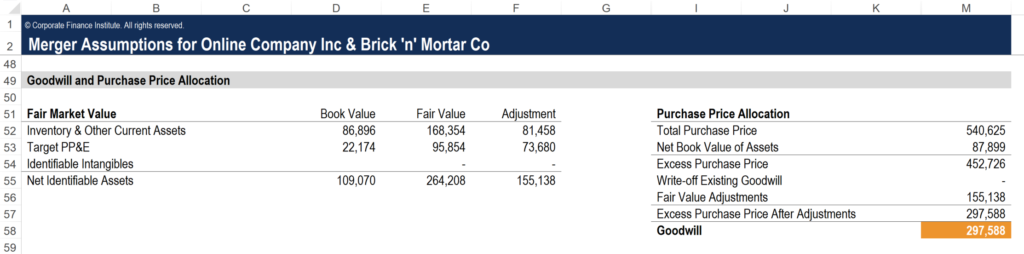

In financial modelingWhat is Financial ModelingFinancial modeling is performed in Excel to forecast a company's financial performance. Overview of what is financial modeling, how & why to build a model. for mergers and acquisitions (M&AMergers Acquisitions M&A ProcessThis guide takes you through all the steps in the M&A process. Learn how mergers and acquisitions and deals are completed. In this guide, we'll outline the acquisition process from start to finish, the various types of acquirers (strategic vs. financial buys), the importance of synergies, and transaction costs), it’s important to accurately reflect the value of goodwill in order for the total financial model to be accurate. Below is a screenshot of how an analyst would perform the analysis required to calculate the values that go on the balance sheet.

This screenshot is taken from CFI’s M&A Financial Modeling Course.

Steps for Calculating Goodwill in an M&A Model

1. Book Value of Assets

First, get the book value of all assets on the target’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting.. This includes current assets, non-current assets, fixed assets, and intangible assets. You can get these figures from the company’s most recent set of financial statements.

2. Fair Value of Assets

Next, have an accountant determine the fair value of the assets. This process is somewhat subjective, but an accounting firm will be able to perform the necessary analysis to justify a fair current market value of each asset.

3. Adjustments

Calculate the adjustments by simply taking the difference between the fair value and the book value of each asset.

4. Excess Purchase Price

Next, calculate the Excess Purchase Price by taking the difference between the actual purchase price paid to acquire the target company and the Net Book Value of the company’s assets (assets minus liabilities).

5. Calculate Goodwill

With all of the above figures calculated, the last step is to take the Excess Purchase Price and deduct the Fair Value Adjustments. The resulting figure is the Goodwill that will go on the acquirer’s balance sheet when the dealDeals & TransactionsResources and guide to understanding deals and transactions in investment banking, corporate development, and other areas of corporate finance. Download templates, read examples and learn about how deals are structured. Non-disclosure agreements, share purchase agreements, asset purchases, and more M&A resources closes.

More Resources

CFI is a leading provider of financial analysis courses, including the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program. To help you advance your career, check out the additional CFI resources below:

- M&A Considerations and ImplicationsM&A Considerations and ImplicationsWhen conducting M&A a company must acknowledge & review all factors and complexities that go into mergers and acquisitions. This guide outlines important

- Takeover PremiumTakeover PremiumTakeover premium is the difference between the market value (or estimated value) of the company and the actual price to acquire it.

- Types of AssetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

-

Accrued Revenue: Definition, Examples & Accounting Explained

Accrued revenue is revenue that has been earned by providing goods or services but the payment has yet to be received. In other words, cash collection will occur in a subsequent period after the goods

-

Understanding Book Value: A Key Financial Metric

Book value is a company’s equity value as reported in its financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statem

Accounting

- Acquirer Definition: Understanding Corporate Acquisitions

- Understanding Clawbacks: Protecting Stakeholders from Failed Performance

- Understanding Financial Gearing: Debt & Leverage Explained

- Leverage in Finance: Strategies, Types & Risks

- EBITA Explained: Understanding Earnings Before Interest, Taxes, and Amortization

- Understanding Expenditures: Definition and Types

- Understanding Goodwill Impairment: A Comprehensive Guide

- OIBDA Explained: Understanding Operating Income Before Depreciation & Amortization

- Understanding Vouchers: A Guide to Accounts Payable Documents

-

Understanding the Role of an Accountant: Key Responsibilities & Importance

Understanding the Role of an Accountant: Key Responsibilities & ImportanceAn accountant plays a very crucial role in an organizationTypes of OrganizationsThis article on the different types of organizations explores the various categories that organizational structures can ...

-

Streamlining Processes: Definition, Benefits & Techniques

Streamlining Processes: Definition, Benefits & TechniquesStreamlining refers to the improvement of the efficiency of a certain process within an organization. It can be done by automationExcel vs Automation in Financial ModelingBefore we discuss Excel vs au...