General Ledger (GL): Definition, Function & Importance

In accountingAccountingAccounting is a term that describes the process of consolidating financial information to make it clear and understandable for all, a General Ledger (GL) is a record of all past transactions of a company, organized by accounts. General Ledger (GL) accounts contain all debit and credit transactionsCredit SalesCredit sales refer to a sale in which the amount owed will be paid at a later date. In other words, credit sales are purchases made by affecting them. In addition, they include detailed information about each transaction, such as the date, description, amount, and may also include some descriptive information on what the transaction was.

In accountingAccountingAccounting is a term that describes the process of consolidating financial information to make it clear and understandable for all software, a general ledger sorts all transaction information through the accounts. Also, it is the primary source for generating the company’s trial balanceTrial BalanceA trial balance is a report that lists the balances of all general ledger accounts of a company at a certain point in time. The accounts and financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are. The ledger’s accuracy is validated by a trial balance, which confirms that the sum of all debit accounts is equal to the sum of all credit accounts.

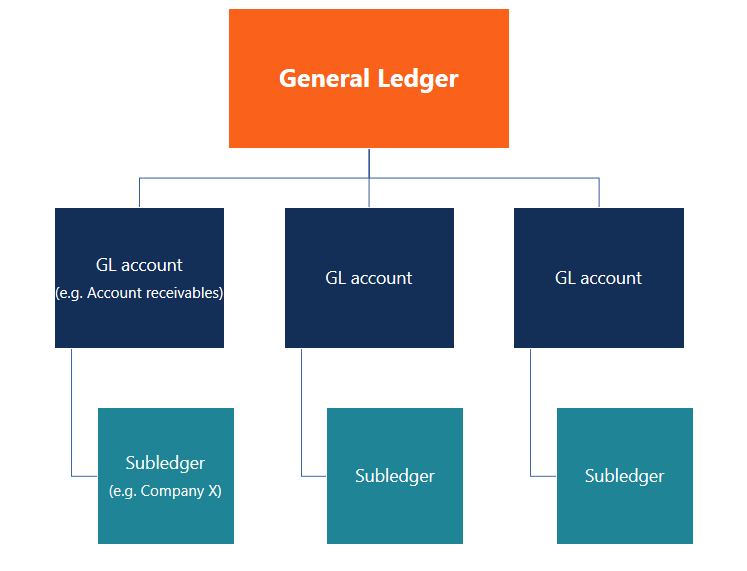

General ledger account

A general ledger account (GL account) is a primary component of a general ledger. A GL account records all transactions for that account. The transactions are related to various accounting elements, including assets, liabilities,Types of LiabilitiesThere are three primary types of liabilities: current, non-current, and contingent liabilities. Liabilities are legal obligations or debt equityEquity MethodThe equity method is a type of accounting used in investments. It is used when the investor holds significant influence over investee but does, revenues, expenses,Accrued ExpensesAccrued expenses are expenses that are recognized even though cash has not been paid. They are usually paired up against revenue via the matching principle gains, and losses.

For example, cash and account receivablesAccounts Payable vs Accounts ReceivableIn accounting, accounts payable and accounts receivable are sometimes confused with the other. The two types of accounts are very similar in are part of the company’s assets. On the ledger, each of the assets will have its own GL account.

You can explore Financial Statements further with CFI’s Reading Financial Statements Course.

Controlling Accounts vs. Subsidiary ledger

For a large organization, a general ledger can be extremely complicated. In order to simplify the audit of accounting records or the analysis of records by internal stakeholders, subsidiary ledgers can be created.

A subsidiary ledger (sub-ledger) is a sub-account related to a GL account that traces the transactions corresponding to a specific company, purchase, property, etc. If a GL account includes sub-ledgers, they are called controlling accounts.

For example, Companies X, Y, and Z are the clients of Company A. For accounting purposes, Company A may create three sub-ledger accounts corresponding to its three clients under account receivables (controlling accounts) to trace the amounts expected to be received from each client.

General Ledgers and Double-Entry Bookkeeping

A general ledger summarizes all the transactions entered through the double-entry bookkeepingBookkeeperThe primary job of a bookkeeper is to maintain and record the daily financial events of the company. A Bookkeeper is responsible for recording and maintaining a business' financial transactions, such as purchases, expenses, sales revenue, invoices, and payments. method. Under this method, each transaction affects at least two accounts; one account is debited, while another is credited. The total debit amount must always be equal to the total credit amount.

Assets = Liabilities + Shareholder’s Equity is known as the Accounting Equation and is a mathematical representation of the double-entry system of accounting. The equation is broken down in CFI’s Accounting Fundamentals Course.

Source: WikimediaCommons

Link to Balance Sheet and Income Statement

As a General Ledger (GL) records all of the transactions that affect a company’s accounting elements such as Assets, Liabilities, Equity, Expenses, and Revenue, it is the data source used to construct the Balance SheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. and the Income StatementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or. The set of 3-financial statements is the backbone of accounting, as discussed in our Accounting Fundamentals Course.

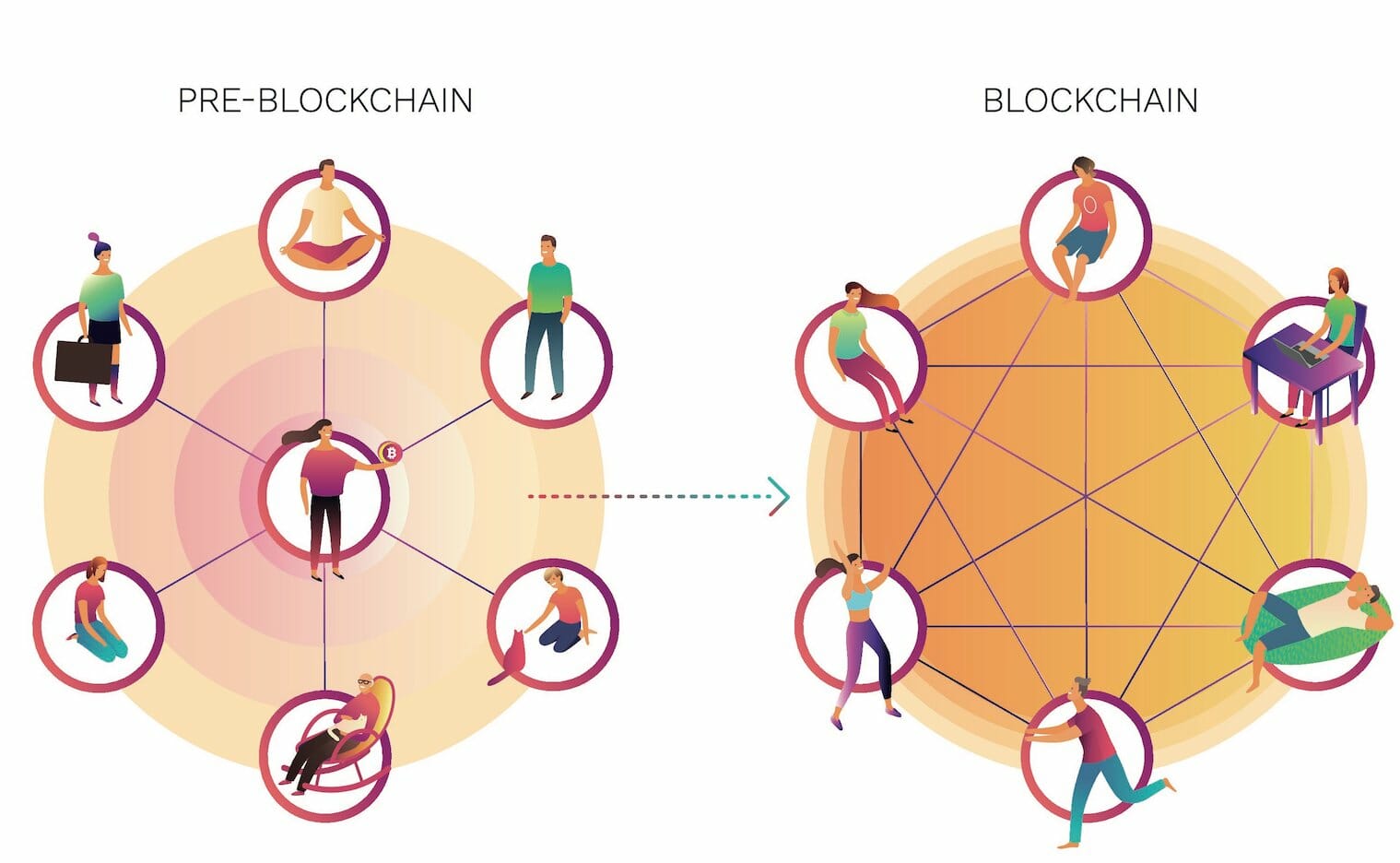

Decentralized Ledger – Blockchain Technology

Blockchain technology has given rise to a decentralized or distributed ledger. Blockchain allows the ledger to be distributed across users worldwide, and each user is part of the entire network, making it less dependent on a single centralized node.

Therefore, everyone within the company network can access the ledger at any point and make a personal copy of the ledger, making it a self-regulated system. This mitigates the risks that Centralized General Ledgers have from having one source control the ledger. The image below is a great illustration of how the blockchain distributed ledger works.

Additional Resources

CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! designation, a leading financial analyst certification program. To continue learning and advancing your financial career, these additional CFI resources will be helpful:

- Adjusting EntriesAdjusting EntriesThis guide to adjusting entries covers deferred revenue, deferred expenses, accrued expenses, accrued revenues and other adjusting journal

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

- How to Link the 3 StatementsHow the 3 Financial Statements are LinkedHow are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and

- T AccountsT Accounts GuideIf you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts

-

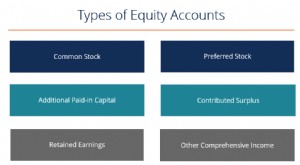

Understanding Equity Accounts: A Comprehensive Guide for Investors

There are several types of equity accounts that combine to make up total shareholders’ equityStockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a company

-

Understanding Accounts Receivable Quality: A Key Indicator of Financial Health

The quality of accounts receivable is the likelihood that the cash flows that are owed to a company in the form of receivables are going to be collected. Analyzing the quality of accounts receivables

Accounting

- Understanding the General Ledger: Definition & Importance for Businesses

- Accounts Payable (AP): Definition, Function & Importance

- Account Aggregation: Simplify Your Finances | [Your Brand Name]

- Understanding the Accounting Cycle: A Comprehensive Guide

- Understanding Accounts Expenses: A Comprehensive Guide

- Accounts Receivable (AR): Definition, Management & Forecasting

- Understanding Accounts Receivable Aging: A Comprehensive Guide

- Understanding T-Accounts: A Guide for Accounting Professionals

- General Ledger: Understanding Your Company's Financial Record

-

Accounts Payable Turnover Ratio: Definition & Interpretation

Accounts Payable Turnover Ratio: Definition & InterpretationThe accounts payable turnover ratio, also known as the payables turnover or the creditor’s turnover ratio, is a liquidity ratioFinancial RatiosFinancial ratios are created with the use of numeri...

-

Accounts Receivable Turnover Ratio: Definition & Calculation

Accounts Receivable Turnover Ratio: Definition & CalculationThe accounts receivable turnover ratio, also known as the debtor’s turnover ratio, is an efficiency ratioFinancial RatiosFinancial ratios are created with the use of numerical values taken from ...