Auditor Legal Liability: Understanding Risks and Responsibilities

Concerns about the legal liability of auditors continue to grow every day. Auditors are highly important people because, ultimately, they are responsible for enhancing the reliability of financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are for all kinds of external users. Like other professionals, they can face civil and criminal liability in the performance of their duties.

Without independent and competent auditors, many fraud casesTop Accounting ScandalsThe last two decades saw some of the worst accounting scandals in history. Billions of dollars were lost as a result of these financial disasters. In this worldwide would’ve gone unnoticed, notwithstanding all the other cases that are still undiscovered. The code of professional conduct states that auditors must go about their business with due care. Due care is the “prudent person” concept.

Due care generally implies four things:

- The auditor must possess the requisite skills to evaluate financial statements

- The auditor has a duty to employ such skill with reasonable care and diligence

- The auditor undertakes his task(s) with good faith and integrity but is not infallible

- The auditor may be liable for negligence, bad faith, or dishonesty, but not for mere errors in judgment

Sources of Legal Liability for an Auditor

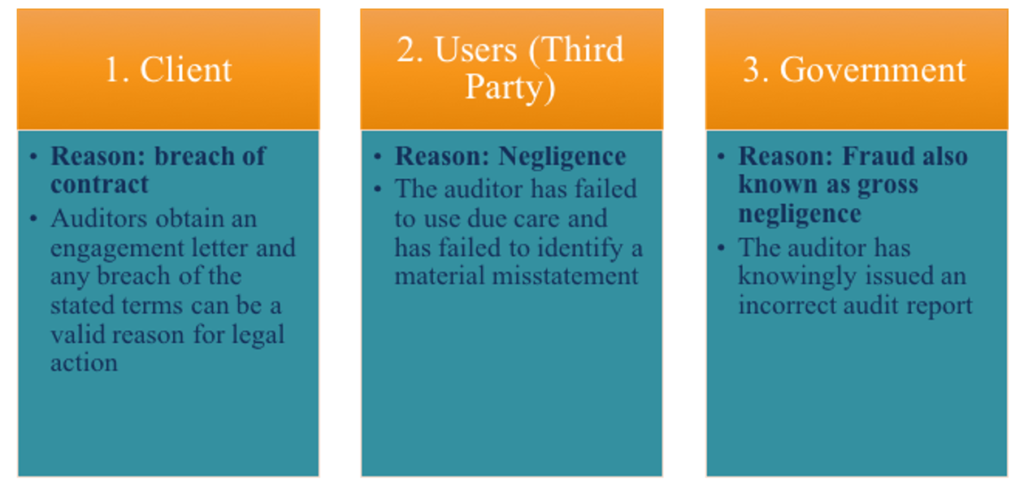

Let us consider the possible entities that may sue an auditor and the possible reasons for a lawsuit.

The Legal Liability of Auditors to Third Parties

By reading this article, one question that might arise is who exactly are auditors responsible to? Can any third party sue an auditor? Or is there a certain class of parties? It is generally known that auditors are responsible to two groups of third parties: 1) Known users of the financial statements, and 2) A limited class of foreseeable users who will rely on the financial statements.

Known users of the financial statements consist of the actual shareholders and creditors of the company. Usually, the company maintains a full list of all these individuals by name. The second group pertaining to foreseeable users requires a bit of judgment.

For example, if the company is trying to issue new equity or get a loan from a bank, these potential investors and the potential creditor (i.e., a bank) will fall under the class of foreseeable users. Therefore, even though the auditor does not know the specific user, the auditor is aware that the client will be using the financial statements to raise bank financing or issue new shares – thus, they know the type of user.

Unjustified Lawsuits

Despite all the potential for lawsuits against auditors, many lawsuits by third parties are unjustified. For example, if a third party sues the auditor because the client (i.e., the company being audited) is no longer a viable company, that is not justified, because the auditor is not responsible for making sure that the company is viable and can continue operating in the long-term. The auditor is solely responsible for making sure that the financial statements are presented fairly against the appropriate evaluation criteria. In addition, unjustified lawsuits also may involve the phenomenon of audit risk.

Audit risk is the risk that an auditor does everything correctly/to the best of his/her ability, but may still express an inappropriate audit opinion on the financial statements. Essentially, the situation deals with errors in financial statements that can remain even after the auditor has followed the auditing rules provided by the governing body.

There are simply bad luck situations when an auditor, for example, decides to pick a sample to audit which is not representative of the entire population of data. The errors originate from unfortunate situations and are not the auditor’s responsibility. If, however, an auditor were not to comply with the general auditing standards outlined by the governing accounting body, that would be a justified reason for a lawsuit, a situation called audit failure.

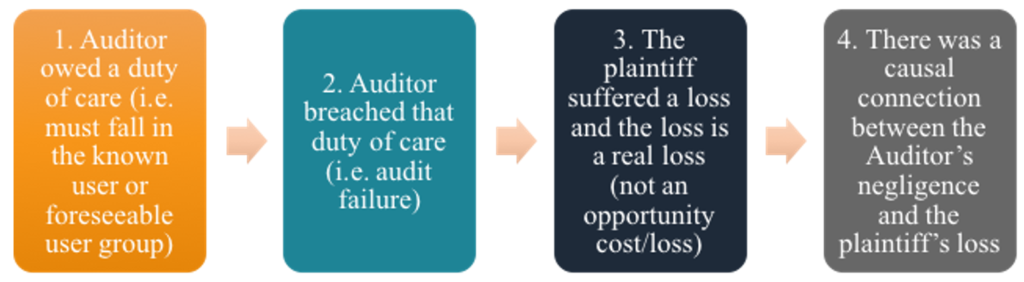

Successful Lawsuits Against Auditors

In order for a third party or a client to successfully sue an auditor under negligence, it is not sufficient to just come up with some evidence and file a court case. The plaintiff must prove the following four criteria:

Additional Resources

Thank you for reading this guide to better understanding the legal liability of auditors. CFI is the official global provider of the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! and on a mission to help anyone in the world advance their career in the financial industry. To continue learning, these free CFI resources will helpful:

- Auditor’s ReportAuditor's ReportAn independent Auditor’s Report is an official opinion issued by an external or internal auditor as to the quality and accuracy of the

- Forensic Audit GuideForensic Audit GuideA forensic audit is a detailed audit of a company's records to be used in a court of law in a legal proceeding. Accountants, lawyers, and

- Audited Financial StatementsAudited Financial StatementsPublic companies are obligated by law to ensure that their financial statements are audited by a registered CPA. The purpose of the

- Audit Legal ImplicationsAccountingAccounting is a term that describes the process of consolidating financial information to make it clear and understandable for all

-

Understanding Audit Evidence: A Comprehensive Guide

Evidence in an audit is information that is collected and required in the review of an entity’s financial transactions, balances, and internal controls to certify the financial statements as bei

-

Understanding Financial Assets: Definitions & Types

Financial assets refer to assets that arise from contractual agreements on future cash flowsCash Flow StatementA cash flow Statement contains information on how much cash a company generated an

Accounting

- Legal Guardian Financial Responsibilities: A Comprehensive Guide

- Understanding Auditors: Roles, Responsibilities & Audit Processes

- Accounting Explained: Understanding Financial Records & Reporting

- Understanding Financial Audits: A Comprehensive Guide

- Understanding Auditor's Reports: A Comprehensive Guide

- Understanding Finance: A Comprehensive Overview

- Contingent Liabilities: Definition, Accounting & Examples

- The Critical Role of Audits in Legal Compliance

- Understanding Auditors: Roles, Responsibilities & Importance

-

Calendarization of Financial Statements: Standardization Explained

Calendarization of Financial Statements: Standardization ExplainedThe process of standardizing the reporting time periods of financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statem...

-

Understanding Deferred Revenue: A Comprehensive Guide

Understanding Deferred Revenue: A Comprehensive GuideDeferred Revenue (also called Unearned Revenue) is generated when a company receives payment for goods and/or services that have not been delivered or completed. In accrual accountingAccrual Accountin...