Lessor vs. Lessee: Understanding Lease Agreements

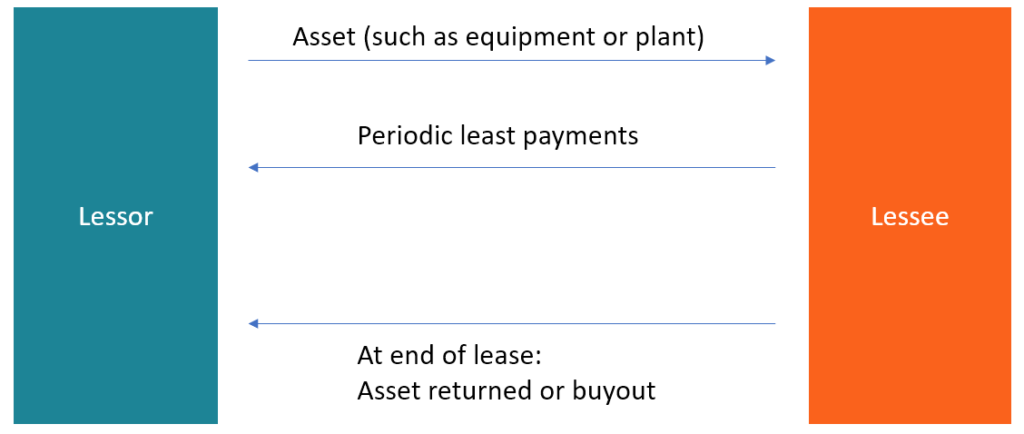

There are two main parties in a lease agreement, and every finance professionalFP&A AnalystBecome an FP&A Analyst at a corporation. We outline the salary, skills, personality, and training you need for FP&A jobs and a successful finance career. FP&A analysts, managers, and directors are responsible for providing executives with the analysis and information they need needs to know how to differentiate between the lessor vs lessee. A leaseLease ClassificationsLease classifications include operating leases and capital leases. A lease is a type of transaction undertaken by a company to have the right to use an asset. In a lease, the company will pay the other party an agreed upon sum of money, not unlike rent, in exchange for the ability to use the asset. is a contractual arrangement where one party, called the lessor, provides an assetTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and for use by the other party, referred to as the lessee, based on periodic payments for an agreed period. The lessee pays the lessor for the usage of the asset or property.

Leasing an asset is often a more economical option than purchasing the actual asset because it requires a much lower cash outlay. Lessor vs lessee – the arrangement between these two parties is entered into a lease agreementEquipment Lease AgreementEquipment lease agreement is a contractual agreement where the lessor, who is the owner of the equipment, allows the lessee to use the equipment for, which is a contractual document signed by both parties.

Roles of Lessor vs Lessee

There are two principal parties in a lease agreement.

Lessor

The lessor is the legal owner of the asset or property, and he gives the lessee the right to use or occupy the asset or property for a specific period. During the contract, the lessor retains the right of ownership of the property and is entitled to receive periodic payments from the lessee based on their initial agreement. He must also be compensated for any losses incurred during the contract due to damage or misuse of the asset in question. If the asset is sold, the lessor must authorize such a transaction and is entitled to receive any financial gains resulting from the sale.

Although the lessor retains ownership of the asset, he enjoys reduced rights to the asset during the course of the agreement. One of these limitations is that the owner, given his limited access to the asset, may only gain entry with the permission of the lessee. He must inform the lessee of any maintenance to be done on the asset or property prior to the actual time of the visit.

However, if the lessee causes damage to the asset, or uses the asset to commit illegal activities, then the lessor reserves the right to evict the lessee or otherwise terminate the lease agreement, without notice. On the expiry of the contract period and depending on the condition of the asset, the asset or property is returned to the lessor, although the lessee may have an option to purchase the asset.

Lessee

The lessee is the party who gets the right to use an asset for a specific period and makes periodic payments to the lessor based on their initial agreement. The length of the lease period often depends at least partially on the type of asset or property. For example, the lease of land to set up a manufacturing plant may be for a longer period than the lease of equipment or a vehicle.

For the duration of the lease period, the lessee is responsible for taking care of the asset and conducting regular maintenance as necessary. If the subject of the lease is an apartment, the lessee must not make any structural changes without the permission of the lessor. Any damages to the property must be repaired before the expiry of the contract. If the lessee fails to make needed repairs or replace any broken fixtures, the lessor has the right to charge the amount of the repairs to the lessee as per the lease agreement.

Lessor vs Lessee Agreement

The lease agreement is a contract between the lessor vs lessee for the use of the asset or property. It outlines the terms of the contract and sets the legal obligations associated with the use of the asset. Both parties are signatories to the agreement and are required to abide by its rules. If either of the parties contravenes the conditions of the lease agreement, the contract can be terminated.

For example, if the lessee conducts illegal activities on the premises of the lessor, the latter holds the right to cancel the contract and evict the lessee from the property. Some lease agreements include the option of the lessee buying the leased asset or property at the end of the lease period.

Types of Lease Agreements

The following are three types of lease agreements:

Capital Lease

A capital lease,Capital Lease vs Operating LeaseThe difference between a capital lease vs operating lease - A capital lease (or finance lease) is treated like an asset on a company’s also referred to as a finance lease, is a lease in which the lessee acquires full control and ownership of the asset and is responsible for all maintenance and other costs associated with the asset. GAAP requires that this type of lease agreement be recorded on the lessee’s balance sheet as an asset with a corresponding liability.

Any interest is recorded separately in the income statement. The lessee assumes both risks and benefits of the ownership of the asset. A capital lease is a long-term lease that spans most of the asset’s useful life.

Operating Lease

An operating lease is a type of lease where the lessor retains all the benefits and responsibilities associated with ownership of the asset. The lessor is in charge of covering everyday operating expenses (such as buying ink for a printer). The lessee uses the asset or equipment for a fixed portion of the asset’s life and does not bear the cost of maintenance. Unlike in a capital lease agreement, the lessee does not record the asset on the balance sheet.

Sale and Leaseback

A sale and leaseback is a type of agreement where one party purchases an asset or property from another party, and immediately leases it to the selling party. The seller becomes the lessee, and the company that purchases the asset becomes the lessor.

This type of agreement is implemented based on the understanding that the seller will immediately lease back the asset from the buyer, subject to an agreed payment rate and period of payment. The buyer in this type of transaction may be a leasing company, finance company, insurance company, individual investor, or institutional investor.

Other Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional free CFI resources below will be useful:

- Prepaid LeasePrepaid LeaseA prepaid lease (or operating lease) is a contract to acquire the use of tangible assets, which include plant, equipment, and real estate.

- Lease AccountingLease AccountingLease accounting guide. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for money or other assets. The two most common types of leases in accounting are operating and financing (capital leases). Advantages, disadvantages, and examples

- Property, Plant & Equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

Variance Swaps: Understanding Volatility Derivatives

Variance swap refers to an over-the-counter financial derivative that allows the holder to speculate on the future volatility of a given underlying asset. Holders use variance swaps to hedge their exp

-

Book Value vs. Fair Value: Understanding the Difference

In accounting and finance, it is important to understand the differences between book value vs fair value. Both concepts are used in the valuation of an asset, but they refer to different aspects

Accounting

- Lease Ratification: Understanding Land Rights for Oil & Mining

- Asset Dissipation: Financing Your Home with Liquid Assets

- Asset Disposal: Definition, Types & Financial Statement Impact

- Depreciated Cost Explained: Calculation & Importance

- Historical Cost Accounting: Definition & Importance

- Impaired Assets: Definition, Recognition, and Accounting Standards

- Understanding Leases: Types, Classifications, and Key Concepts

- Non-Financial Assets: Definition, Examples & Value

- Synthetix: A Decentralized Platform for Synthetic Asset Trading

-

Synthetic Long Assets: Strategy, Risks & Rewards

Synthetic Long Assets: Strategy, Risks & RewardsSometimes referred to as a synthetic long stock, a synthetic long asset is a strategy for options trading that is designed to mimic a long stock position. Traders create a synthetic long asset by purc...

-

Understanding Underlying Assets: Definition & Importance

Understanding Underlying Assets: Definition & ImportanceUnderlying asset is an investment term that refers to the real financial asset or security that a financial derivative is based on. Thus, the value of the underlying asset drives the value of the fina...