Book Value vs. Fair Value: Understanding the Difference

In accounting and finance, it is important to understand the differences between book value vs fair value. Both concepts are used in the valuation of an asset, but they refer to different aspects of an asset’s value. In this article, we will discuss book value vs fair value in detail and indicate their key distinctions.

Book value indicates an asset’s value that is recognized on the balance sheet. Essentially, book value is the original cost of an asset minus any depreciationDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in., amortization, or impairmentImpairmentThe impairment of a fixed asset can be described as an abrupt decrease in fair value due to physical damage, changes in existing laws creating costs.

On the other hand, fair value is referred to as an estimate of the potential value of an asset. In other words, it is the intrinsic value of an asset.

What is Book Value?

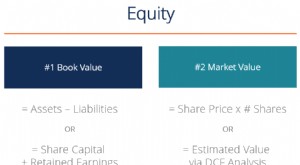

Book value (also known as carrying value or net asset valueNet Asset ValueNet asset value (NAV) is defined as the value of a fund’s assets minus the value of its liabilities. The term "net asset value" is commonly used in relation to mutual funds and is used to determine the value of the assets held. According to the SEC, mutual funds and Unit Investment Trusts (UITs) are required to calculate their NAV) is the value of an asset that is recognized on the balance sheet. It is determined as the cost paid for acquiring an asset minus any depreciation, amortization, or impairment costs applicable to the asset. The concept of book value arises from the practice of recording the assets on the balance sheet at its historical cost.

Book value is one of the most important concepts in accounting. Book value is the historical value of an asset on a company’s balance sheet. Since stockholders’ equityStockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus is calculated as the difference between the assets’ and liabilities’ values, the book value is used to determine the theoretical equity value attributable to the company’s shareholders.

Note that the book value of assets indicates the recorded value that shareholders own in case of the company’s liquidation. In addition, the book value is commonly used to evaluate whether an asset is over- or underpriced by comparing the difference between the asset’s book and market values.

What is Fair Value?

Fair value is a reasonable and unbiased estimate of the intrinsic value of an asset. Essentially, the fair value of an asset is based on several factors such as utility, related costs, and supply and demand considerations. Another common definition of fair value is the price that would be obtained for the sale of an asset or paid to transfer a liability in a transaction between the market participants at the measurement date.

Essentially, the estimation of an asset’s fair value is a generally complicated process. Determining the asset’s fair value is generally guided by the accounting standards. IFRSIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world and US GAAPGAAPGAAP, Generally Accepted Accounting Principles, is a recognized set of rules and procedures that govern corporate accounting and financial provide guidance on how to measure the fair value of an asset.

Note that in accounting, the concept of fair value is not applied to all assets. Fair value is usually estimated for current assets that are held for resale such as marketable securities. Accounting using fair values is frequently exposed to potential accounting fraud due to the fact that companies can manipulate the fair value calculations.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Depreciation MethodsDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits.

- Enterprise Value vs Equity ValueEnterprise Value vs Equity ValueEnterprise value vs equity value. This guide explains the difference between the enterprise value (firm value) and the equity value of a business. See an example of how to calculate each and download the calculator. Enterprise value = equity value + debt - cash. Learn the meaning and how each is used in valuation

- Modified Book ValueModified Book ValueModified book value is one of the several valuation methods used by analysts and investors to assign a value to a company. The modified book value method

- Top Accounting ScandalsTop Accounting ScandalsThe last two decades saw some of the worst accounting scandals in history. Billions of dollars were lost as a result of these financial disasters. In this

-

Understanding Money: Definition, History & Value

Money refers to any verifiable record that is accepted as a medium of exchange for payment of goods and services and repayment of debts in a specific country. Throughout history, governments adopted d

-

Nominal Value Explained: Definition & Financial Significance

Nominal value is a common financial term that is used in various contexts within finance. For stocks and bonds, it is also referred to as the “face value” of an investment that is stated o

Accounting

- Fair Value vs. Book Value: Understanding the Difference

- Understanding Asset Base: Definition, Value & Significance

- Asset Valuation: Understanding Property Value for Business & Finance

- Understanding Fair Value: Definition & Importance

- Understanding Book Value: A Key Financial Metric

- Understanding Fair Market Value: A Comprehensive Guide

- Impaired Assets: Definition, Recognition, and Accounting Standards

- Market Value vs. Book Value: Understanding the Difference

- Net Book Value (NBV): Definition & Calculation

-

Understanding Equity: A Comprehensive Guide for Investors

Understanding Equity: A Comprehensive Guide for InvestorsIn finance and accounting, equity is the value attributable to the owners of a business. The book value of equity is calculated as the difference between assetsTypes of AssetsCommon types of assets in...

-

Face Value Explained: Definition, Examples & Importance

Face Value Explained: Definition, Examples & ImportanceThe value mentioned on an instrument like a coin, stamp, or bill is called the face value of that instrument. For example, a $100 bill comes with a face value of $100. In calculus, the face value of 3...