EBITDA Explained: Understanding Earnings Before Interest, Taxes, Depreciation & Amortization

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization and is a metric used to evaluate a company’s operating performance. It can be seen as a proxy for cash flowCash FlowCash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period. There are many types of CF from the entire company’s operations.

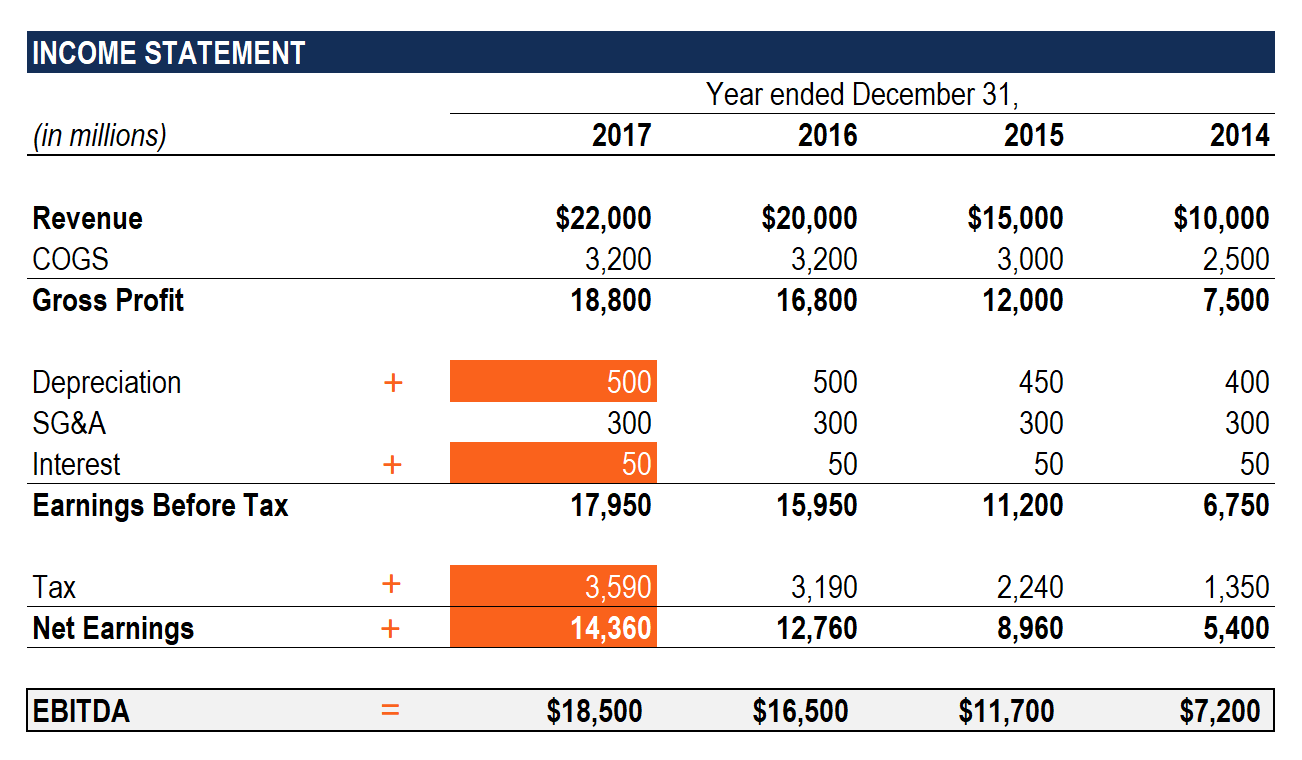

Image: CFI’s Financial Analysis Course.

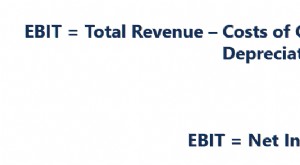

The EBITDA metric is a variation of operating income (EBITEBIT GuideEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it's found by deducting all operating expenses (production and non-production costs) from sales revenue.) that excludes non-operating expenses and certain non-cash expenses. The purpose of these deductions is to remove the factors that business owners have discretion over, such as debt financing, capital structure, methods of depreciationDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in., and taxes (to some extent). It can be used to showcase a firm’s financial performance without accounting for its capital structure.

EBITDA focuses on the operating decisions of a business because it looks at the business’ profitabilityNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through from its core operations before the impact of capital structure, leverage, and non-cash items such as depreciation are taken into account.

It is not a recognized metric in use by IFRSIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world or US GAAP. In fact, certain investors like Warren Buffet have a particular disdainWarren Buffett - EBITDAWarren Buffett is well known for disliking EBITDA. Warren Buffett is credited for saying “Does management think the tooth fairy pays for CapEx?" for this metric, as it does not account for the depreciation of a company’s assets. For example, if a company has a large amount of depreciable equipment (and thus a high amount of depreciation expense), then the cost of maintaining and sustaining these capital assets is not captured.

EBITDA Formula

Here is the formula for calculating EBITDA:

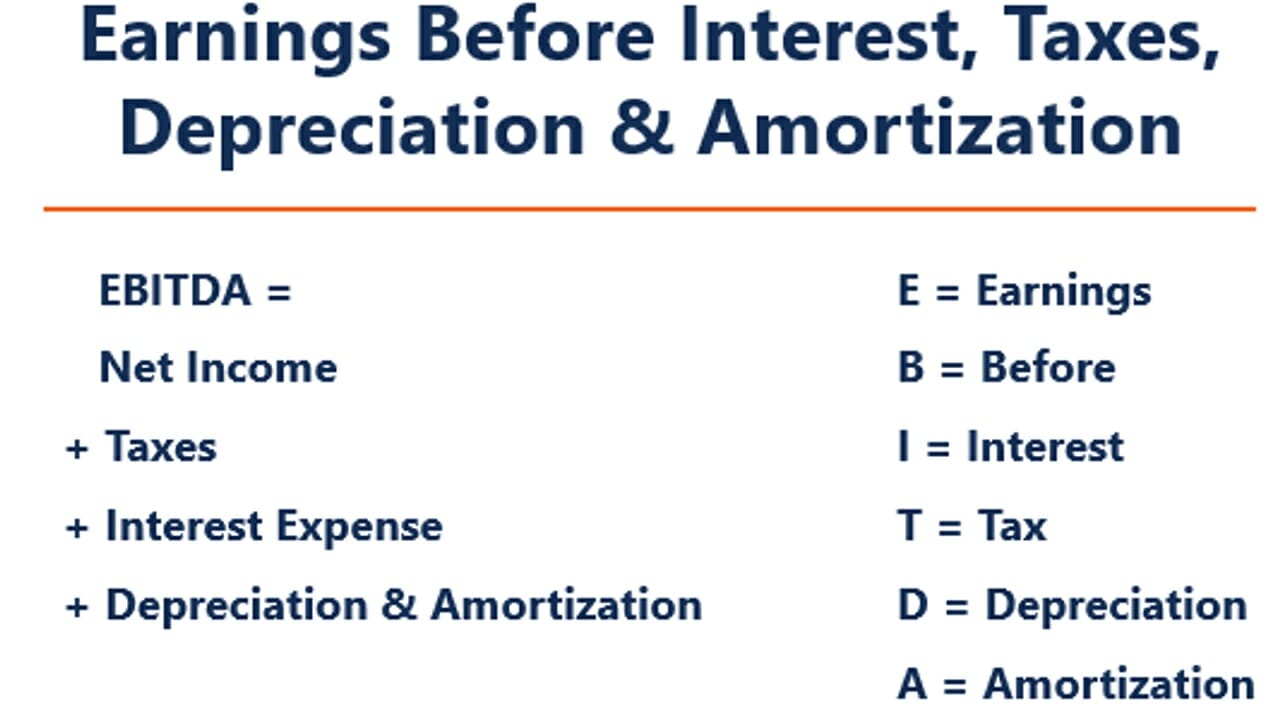

EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

OR

EBITDA = Operating Profit + Depreciation + Amortization

Below is an explanation of each component of the formula:

Interest

InterestInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also is excluded from EBITDA, as it depends on the financing structure of a company. It comes from the money it has borrowed to fund its business activities. Different companies have different capital structuresCapital StructureCapital structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. A firm's capital structure, resulting in different interest expenses. Hence, it is easier to compare the relative performance of companies by adding back interest and ignoring the impact of capital structure on the business. Note that interest payments are tax-deductible, meaning corporations can take advantage of this benefit in what is called a corporate tax shieldTax ShieldA Tax Shield is an allowable deduction from taxable income that results in a reduction of taxes owed. The value of these shields depends on the effective tax rate for the corporation or individual. Common expenses that are deductible include depreciation, amortization, mortgage payments and interest expense.

Taxes

TaxesAccounting For Income TaxesIncome taxes and their accounting is a key area of corporate finance. There are several objectives in accounting for income taxes and optimizing a company's valuation. vary and depend on the region where the business is operating. They are a function of tax rules, which are not really part of assessing a management team’s performance and, thus, many financial analystsBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! prefer to add them back when comparing businesses.

Depreciation & Amortization

DepreciationDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in. and amortization (D&A) depend on the historical investments the company has made and not on the current operating performance of the business. Companies invest in long-term fixed assetsLong Term AssetsLong term assets are assets that a company uses in its production process and with a useful life of more than one year. Such assets are also (such as buildings or vehicles) that lose value due to wear and tear. The depreciation expense is based on a portion of the company’s tangible fixed assets deteriorating. Amortization expense is incurred if the asset is intangible. Intangible assetsIntangible AssetsAccording to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible assets such as patents are amortized because they have a limited useful life (competitive protection) before expiration.

D&A is heavily influenced by assumptions regarding useful economic life, salvage value,Salvage ValueSalvage value is the estimated amount that an asset is worth at the end of its useful life. Salvage value is also known as scrap value and the depreciation methodDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits. used. Because of this, analysts may find that operating income is different than what they think the number should be, and therefore D&A is backed out of the EBITDA calculation.

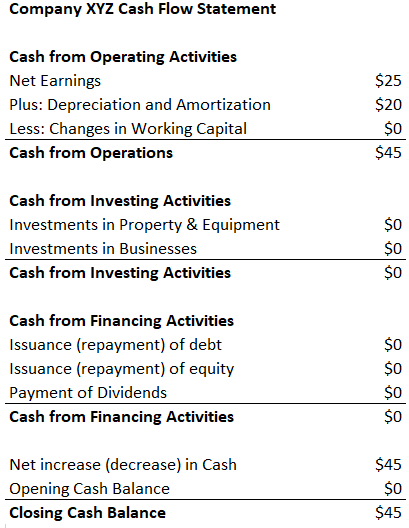

The D&A expense can be located in the firm’s cash flow statement under the cash from operating activitiesOperating Cash FlowOperating Cash Flow (OCF) is the amount of cash generated by the regular operating activities of a business in a specific time period. section. Since depreciation and amortization is a non-cash expenseNon-Cash ExpensesNon cash expenses appear on an income statement because accounting principles require them to be recorded despite not actually being paid for with cash. , it is added back (the expense is usually a positive number for this reason) while on the cash flow statement.

Example: The depreciation and amortization expense for XYZ is $20.

Why Use EBITDA?

The EBITDA metric is commonly used as a proxy for cash flowCash FlowCash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period. There are many types of CF. It can give an analyst a quick estimate of the value of the company, as well as a valuation range by multiplying it by a valuation multipleEBITDA MultipleThe EBITDA multiple is a financial ratio that compares a company's Enterprise Value to its annual EBITDA. This multiple is used to determine the value of a company and compare it to the value of other, similar businesses. A company's EBITDA multiple provides a normalized ratio for differences in capital structure, obtained from equity research reportsEquity Research ReportAn equity research report is a document prepared by an analyst that provides a recommendation for investors to buy, hold, or sell shares of a company., industry transactions, or M&AMergers Acquisitions M&A ProcessThis guide takes you through all the steps in the M&A process. Learn how mergers and acquisitions and deals are completed. In this guide, we'll outline the acquisition process from start to finish, the various types of acquirers (strategic vs. financial buys), the importance of synergies, and transaction costs.

In addition, when a company is not making a profitNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through, investors can turn to EBITDA to evaluate a company. Many private equity firms use this metric because it is very good for comparing similar companies in the same industry. Business owners use it to compare their performance against their competitors.

Disadvantages

EBITDA is not recognized by GAAP or IFRSIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world. Some are skeptical (like Warren BuffettWarren Buffett - EBITDAWarren Buffett is well known for disliking EBITDA. Warren Buffett is credited for saying “Does management think the tooth fairy pays for CapEx?") of using it because it presents the company as if it has never paid any interest or taxes, and it shows assets as having never lost their natural value over time (no depreciation or Capital ExpendituresCapital ExpendituresCapital expenditures refer to funds that are used by a company for the purchase, improvement, or maintenance of long-term assets to improve deducted).

For example, a fast-growing manufacturing company may present increasing sales and EBITDA year over year (YoYYoY (Year over Year)YoY stands for Year over Year and is a type of financial analysis used for comparing time series data. It is useful for measuring growth and detecting trends.). To expand rapidly, it acquired many fixed assets over time and all were funded with debt. Although it may seem that the company has strong top-line growth, investors should look at other metrics as well, such as capital expenditures, cash flow, and net income.

Video Explanation of EBITDA

Below is a short video tutorial of Earnings Before Interest, Taxes, Depreciation, and Amortization. The short lesson will cover various ways to calculate it and provide some simple examples to work through.

Video: CFI Financial Analyst Training ProgramBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!.

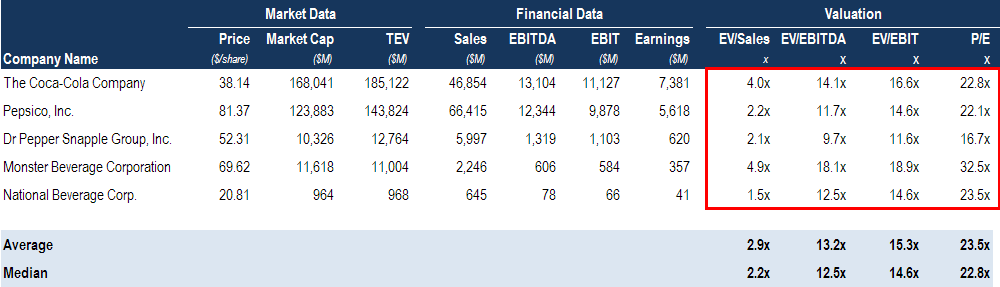

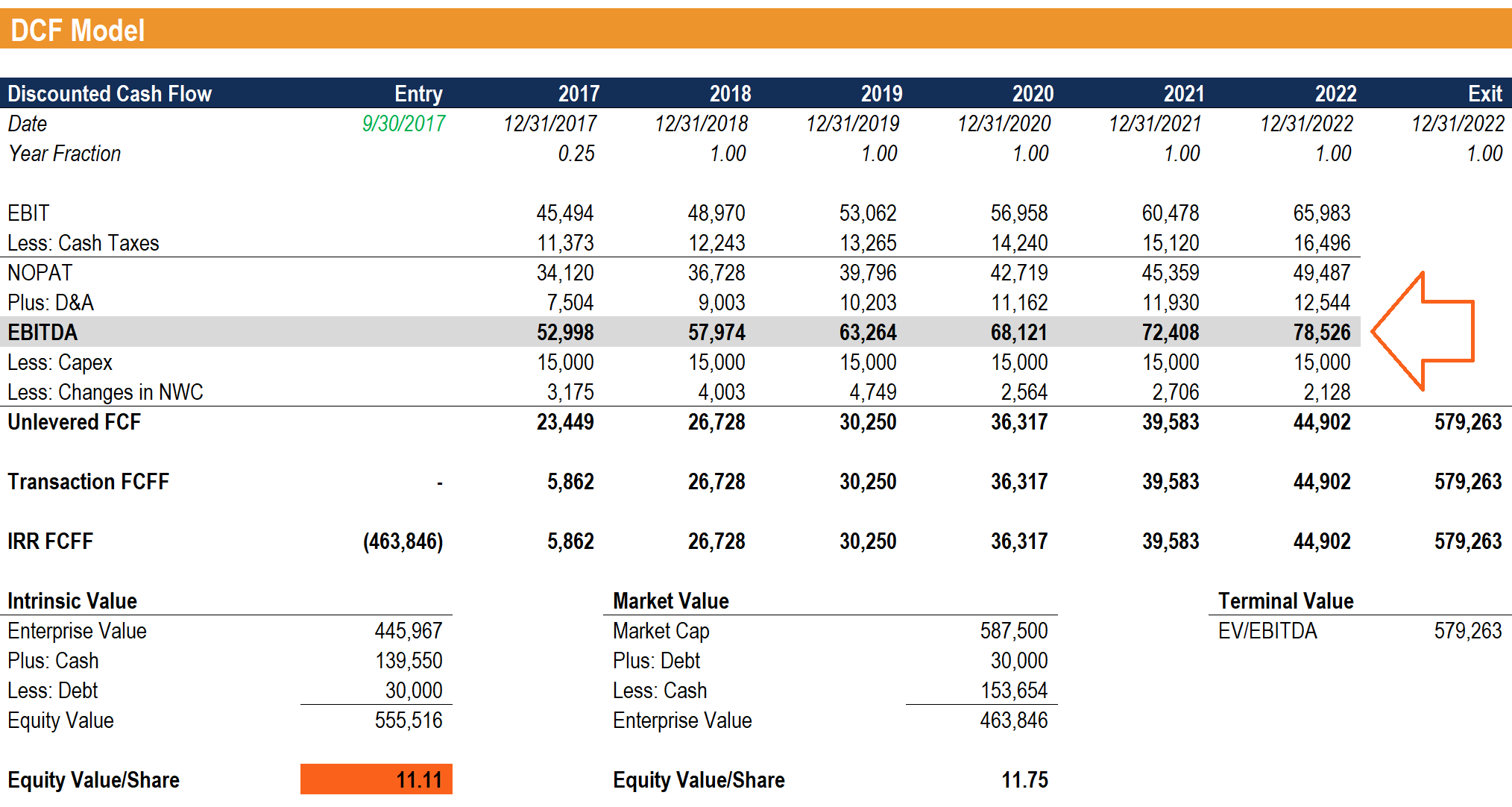

EBITDA Used in Valuation (EV/EBITDA Multiple)

When comparing two companies, the Enterprise Value/EBITDA ratioEV/EBITDAEV/EBITDA is used in valuation to compare the value of similar businesses by evaluating their Enterprise Value (EV) to EBITDA multiple relative to an average. In this guide, we will break down the EV/EBTIDA multiple into its various components, and walk you through how to calculate it step by step can be used to give investors a general idea of whether a company is overvalued (high ratio) or undervalued (low ratio). It’s important to compare companies that are similar in nature (same industry, operations, customers, margins, growth rate, etc.), as different industries have vastly different average ratios (high ratios for high-growth industries, low ratios for low-growth industries).

The metric is widely used in business valuationValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions and is found by dividing a company’s enterprise value by EBITDA.

Image: CFI’s Business Valuation Course.

EV/EBITDA Example:

Company ABC and Company XYZ are competing grocery stores that operate in New York. ABC has an enterprise value of $200M and an EBITDA of $10M, while firm XYZ has an enterprise valueEnterprise Value (EV)Enterprise Value, or Firm Value, is the entire value of a firm equal to its equity value, plus net debt, plus any minority interest of $300M and an EBITDA of $30M. Which company is undervalued on an EV/EBITDA basis?

Company ABC: Company XYZ:

EV = $200M EV = $300M

EBITDA = $10M EBITDA = $30M

EV/EBITDA = $200M/$10M = 20x EV/EBITDA = $300M/$30M = 10x

On an EV/EBITDA basis, company XYZ is undervalued because it has a lower ratio.

EBITDA in Financial Modeling

EBITDA is used frequently in financial modelingWhat is Financial ModelingFinancial modeling is performed in Excel to forecast a company's financial performance. Overview of what is financial modeling, how & why to build a model. as a starting point for calculating un-levered free cash flow. Earnings before interest, taxes, depreciation, and amortization is such a frequently referenced metric in finance that it’s helpful to use it as a reference point, even though a financial model only values the business based on its free cash flowFree Cash Flow (FCF)Free Cash Flow (FCF) measures a company’s ability to produce what investors care most about: cash that's available be distributed in a discretionary way..

Image: CFI’s video-based financial modeling courses.

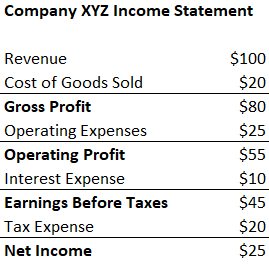

Example Calculation #1

Company XYZ accounts for their $20 depreciation and amortization expense as a part of their operating expenses. Calculate their Earnings Before Interest Taxes Depreciation and Amortization:

EBITDA = Net Income + Tax Expense + Interest Expense + Depreciation & Amortization Expense

= $25 + $20 + $10 + $20

= $75

EBITDA = Revenue – Cost of Goods Sold – Operating Expenses + Depreciation & Amortization Expense

= $100 – $20 – $25 + $20

= $75

Download the Free Template

Enter your name and email in the form below and download the free template now!

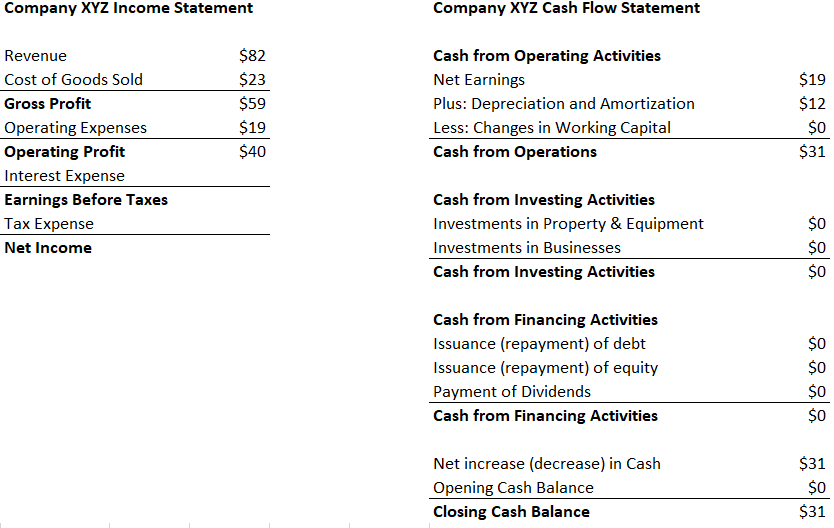

Example Calculation #2

Company XYZ’s depreciation and amortization expense are incurred from using their machine that packages the candy they sell. They pay 5% interest to debtholders and have a tax rate of 50%. What is XYZ’s Earnings Before Interest Taxes Depreciation and Amortization?

First Step: Fill out the income statementIncome Statement TemplateFree Income Statement template to download. Create your own statement of profit and loss with annual and monthly templates in the Excel file

Interest expense = 5% * $40 (operating profit) = $2

Earnings Before Taxes = $40 (operating profit) – $2 (interest expense) = $38

Tax Expense = $38 (earnings before taxes) * 50% = $19

Net Income = $38 (earnings before taxes) – $19 (tax expense) = $19

*Note: net income can also be found in the Cash Flow Statement, above the depreciation and amortization expense.

Second Step: Find the depreciation and amortization expense

In the Statement of Cash FlowsStatement of Cash FlowsThe Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements that report the cash, the expense is listed as $12.

Since the expense is attributed to the machines that package their candy (the depreciating asset directly helps with producing inventory), the expense will be a part of their cost of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct.

Third Step: Calculate Earning Before Interest Taxes Depreciation and Amortization

EBITDA = Net Income + Tax Expense + Interest Expense + Depreciation & Amortization Expense

= $19 + $19 + $2 + $12

= $52

EBITDA = Revenue – Cost of Goods Sold – Operating Expenses + Depreciation & Amortization Expense

= $82 – $23 – $19 + $12

= $52

More Resources

We hope this has been a helpful guide to EBITDA – Earnings Before Interest Taxes Depreciation and Amortization. If you are looking for a career in corporate finance, this is a metric you’ll hear a lot about. To keep learning more, we highly recommend these additional CFI resources:

- EBIT vs EBITDAEBIT vs EBITDAEBIT vs EBITDA - two very common metrics used in finance and company valuation. There are important differences, pros/cons to understand.

- Valuation methodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

- Financial modeling guideFree Financial Modeling GuideThis financial modeling guide covers Excel tips and best practices on assumptions, drivers, forecasting, linking the three statements, DCF analysis, more

- How to be a great financial analystThe Analyst Trifecta® GuideThe ultimate guide on how to be a world-class financial analyst. Do you want to be a world-class financial analyst? Are you looking to follow industry-leading best practices and stand out from the crowd? Our process, called The Analyst Trifecta® consists of analytics, presentation & soft skills

-

Understanding Flow-Through Entities: Tax Advantages & Types

A flow-through entity – also known as a “pass-through entity” or “fiscally-transparent entity” – is a legal business entity where its profits flow directly to the i

-

Understanding Income Tax Payable: A Guide for Businesses

Income tax payable is a term given to a business organization’s tax liability to the government where it operates. The amount of liability will be based on its profitability during a given perio

finance

- Understanding Discretionary Income: Definition & Examples

- EBITDA Margin: Definition, Calculation & Importance

- Understanding Income: Definition, Types & Uses

- Understanding Income Properties: A Guide to Real Estate Investment

- Understanding Income Tax: A Comprehensive Guide for Individuals & Businesses

- Understanding Interest Income: A Comprehensive Guide

- Understanding Taxable Income: Definition & Calculation

- Understanding Accounting Income: A Key Financial Metric

- Net Income Explained: A Comprehensive Guide for Businesses & Individuals

-

EBIT Explained: Understanding Earnings Before Interest & Taxes

EBIT Explained: Understanding Earnings Before Interest & TaxesEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statementIncome StatementThe Income Statement is one of a companys core financial statements...

-

Understanding Federal Income Tax: A Comprehensive Guide

Understanding Federal Income Tax: A Comprehensive GuideIn many countries, taxes are imposed at the federal, state/provincial, and local level. The income tax that one pays at the federal level is determined by applying a predetermined rate to the earnings...