Non-Current Assets: Definition, Examples & Accounting

Non-current assets are assets whose benefits will be realized over more than one year and cannot easily be converted into cash. The assets are recorded on the balance sheet at acquisition cost, and they include property, plant and equipment, intellectual property, intangible assetsIntangible AssetsAccording to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible assets, and other long-term assets.

Property, plant, and equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex, refers to fixed assets such as land, buildings, motor vehicles, etc., whereas intangible assets are the items that lack a physical form.

Non-current assets are capitalized rather than expensed, and their value is drawn down and allocated over the number of years that the asset will be in use. Companies purchase non-current assets with the aim of using them in the business since their benefits will last for a period exceeding one year. The assets may be amortized or depreciated, depending on its type.

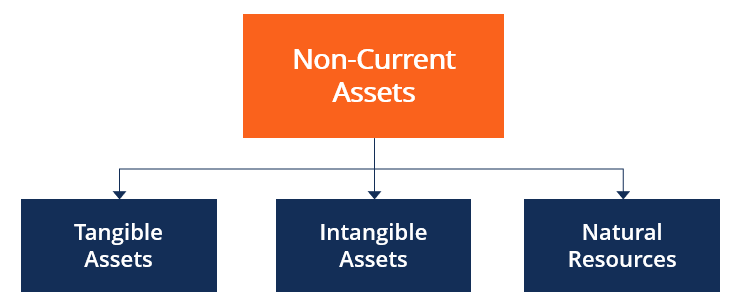

Types of Non-Current Assets

The following are the key categories of non-current assets:

1. Tangible Assets

Tangible assets refer to assets with a physical form or property that are owned by a company and are central to its core operations. The recorded value of a tangible asset is its original acquisition cost less any accumulated depreciation.

However, not all physical assets are depreciated. Assets, such as land, are held at cost even though they tend to appreciate in value. Depreciation is a non-cash notation that reduces the value of an asset over time.

2. Intangible Assets

Intangible are assets that lack a physical form but offer economic value to the company. Examples of such assets include goodwill and intellectual property, such as trademarks, patents, and copyrights.

A company can acquire intangible assets from another entity or create them from within the business. The assets created by the business lack a recorded book valueBook ValueBook value is a company’s equity value as reported in its financial statements. The book value figure is typically viewed in relation to the and are, therefore, not recorded on the balance sheet.

Intangible assets can be definite or indefinite. An example of an indefinite intangible asset is brand recognition, which remains for as long as the company stays afloat. On the other hand, a definite intangible asset comes with a limited life, and it only stays with the company for the duration of a contract or agreement.

An example of a definite intangible asset is a legal agreement to operate the patents of another entity. The company is required to operate the patent for an agreed period of time, and the creator of the patent remains the owner of the patent. Even though an intangible asset lacks physical value, it can significantly contribute to the long-term success of a company.

3. Natural Resources

Natural resources are the assets that occur naturally, and they are derived from the earth. Examples of natural resources include timber, fossil fuels, oil fields, and minerals. Natural resources are also called wasting assets because they are used up when they are consumed. The assets must be consumed through extraction from the natural setting.

For example, natural gas is an example of a natural resource that must be extracted in order to be used. It means that the asset must be mined or pumped out of the ground for it to be used. Natural assets are recorded on the balance sheet at the cost of acquisition plus exploration and development costs and less accumulated depletion.

Examples of Non-Current Assets

The following are some examples of non-current assets:

1. Property, Plant and Equipment (PP&E)

PP&E are long-term physical assets that are an important part of a company’s core operations, and they are used in the production process or sale of other assets. The assets come in a physical form, and they are not easily converted to cash or liquidated.

The total value of PP&E is equal to the total value of property, plant, and equipment recorded on the balance sheet less accumulated depreciation. Accumulated depreciation is the total depreciation expense charged to an asset since it was put into use. Investments in PP&E show there is potential future growth and a positive outlook for the company.

2. Goodwill

Goodwill is an intangible asset that is created when one company purchases another entity. It is generated when the price paid for the company exceeds the fair value of all identifiable assets and liabilities assumed in the transaction.

The goodwill purchased is for intangible assets such as the reputation of the company, brand nameBrand EquityIn marketing, brand equity refers to the value of a brand and is determined by the consumer’s perception of the brand. Brand equity can be positive or, good customer relations, solid customer base, and the quality of the employees.

3. Long-term Investments

Long-term investments include assets such as bonds, stocks, and notes that investors buy in the financial markets with the hope that they will appreciate in value and earn a good return in the future. These assets are also recorded in the company’s balance sheet.

Additional Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

- AmortizationAmortizationAmortization refers to the process of paying off a debt through scheduled, pre-determined installments that include principal and interest

- Net Identifiable AssetsNet Identifiable AssetsNet Identifiable Assets consist of assets acquired from a company whose value can be measured, used in M&A for Goodwill and Purchase Price Allocation.

- Depreciation MethodsDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits.

- Non-Operating AssetsNon-Operating AssetsNon-operating assets are assets that are not required in the normal operations of a business but that can generate income nonetheless. The assets are recorded in the balance sheet and may be listed separately or as part of operating assets. Non-operating assets may be investments or assets that can be disposed of to generate income

-

Understanding Redundant Assets: Definition & Impact on Business

Redundant assets are assets that generate incomeOperating IncomeOperating income is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue. for the bus

-

Risk-Weighted Assets (RWA): A Comprehensive Guide for Finance Professionals

Risk-weighted assets is a banking term that refers to an asset classification system that is used to determine the minimum capital that banks should keep as a reserve to reduce the risk of insolvency.

Accounting

- Investable Assets: A Comprehensive Guide for Investors

- Understanding Household Assets: A Comprehensive Guide

- Fixed Assets: Definition, Examples & Importance for Businesses

- Monetary Assets: Definition, Examples & Key Characteristics

- Understanding Non-Monetary Assets: Definition & Examples

- Understanding Quick Assets: Definition & Examples

- Biological Assets: Definition, Examples & Accounting

- Understanding Financial Assets: Definitions & Types

- Understanding Intangible Assets: Definition & Importance

-

Net Liquid Assets: Definition, Calculation & Importance

Net Liquid Assets: Definition, Calculation & ImportanceNet liquid assets is a term used to define the immediate liquidity position of a company. It is calculated as the difference between liquid assets and current liabilitiesCurrent LiabilitiesCurrent lia...

-

Non-Operating Assets: Definition, Examples & Financial Impact

Non-Operating Assets: Definition, Examples & Financial ImpactNon-operating assets are assets that are not required in the normal operations of a business but that can generate income nonetheless. The assets are recorded in the balance sheetBalance SheetThe bala...