Understanding Product Costs: Direct Materials, Labor & Overhead

Product costs are costs that are incurred to create a product that is intended for sale to customers. Product costs include direct material (DM), direct labor (DL), and manufacturing overhead (MOH).

Understanding the Costs in Product Costs

Product costs are the costs directly incurred from the manufacturing process. The three basic categories of product costs are detailed below:

1. Direct material

Direct material costs are the costs of raw materials or parts that go directly into producing products. For example, if Company A is a toy manufacturer, an example of a direct material cost would be the plastic used to make the toys.

2. Direct labor

Direct labor costs are the wagesEmployee Stock Ownership Plan (ESOP)An Employee Stock Ownership Plan (ESOP) refers to an employee benefit plan that gives the employees an ownership stake in the company. The employer allocates a percentage of the company’s shares to each eligible employee at no upfront cost. The distribution of shares may be based on the employee’s pay scale, terms of, benefits, and insuranceHMO vs PPO: Which is Better?Getting the best healthcare often requires choosing between an HMO vs PPO. You need to be able to make an informed decision on which plan will work best. that are paid to employees who are directly involved in manufacturing and producing the goods – for example, workers on the assembly line or those who use the machinery to make the products.

3. Manufacturing overhead

Manufacturing overhead costs include direct factory-related costs that are incurred when producing a product, such as the cost of machinery and the cost to operate the machinery. Manufacturing overhead costs also include some indirect costs, such as the following:

- Indirect materials: Indirect materials are materials that are used in the production process but that are not directly traceable to the product. For example, glue, oil, tape, cleaning supplies, etc. are classified as indirect materials.

- Indirect labor: Indirect labor is the labor of those who are not directly involved in the production of the products. An example would be security guards, supervisors, and quality assurance workers in the factory. Their wages and benefits would be classified as indirect labor costs.

Example of Product Costs

Company A is a manufacturer of tables. Its product costs may include:

- Direct material: The cost of wood used to create the tables.

- Direct labor: The cost of wages and benefits for the carpenters to create the tables.

- Manufacturing overhead (indirect material): The cost of nails used to hold the tables together.

- Manufacturing overhead (indirect labor): The cost of wages and benefits for the security guards to overlook the manufacturing facility

- Manufacturing overhead (other): The cost of factory utilities.

Company A produced 1,000 tables. To produce 1,000 tables, the company incurred costs of:

- $12,000 on wood

- $2,000 on wages for carpenters and $500 on wages for security guards to overlook the manufacturing facility

- $100 for a bag of nails to hold the tables together

- $500 for factory rent and utilities

Total product costs: $12,000 (direct material) + $2,000 (direct labor) + $100 (indirect material) + $500 (indirect labor) + $500 (other costs) = $15,100. As this is the cost to produce 1,000 tables, the company has a per unit cost of $15.10 ($15,100 / 1,000 = $15.10).

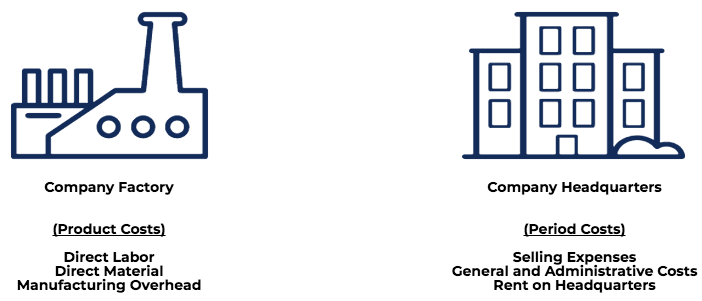

Period Costs

Product costs are costs necessary to manufacture a product, while period costs are non-manufacturing costs that are expensed within an accounting period.

Product Costs Period Costs DefinitionCosts incurred to manufacture a productCosts that are not incurred to manufacture a product and, therefore, cannot be assigned to the productComprises of:Manufacturing and production costsNon-manufacturing costsExamplesRaw material, wages on labor, production overheads, rent on the factory, etc.Marketing costs, sales costs, audit fees, rent on the office building, etc.

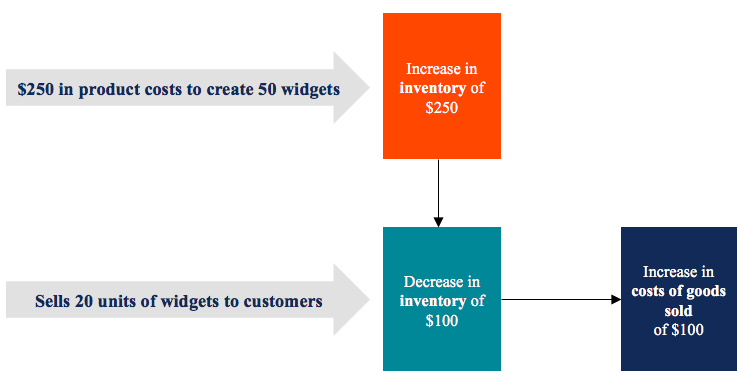

Consider the diagram below:

Costs on Financial Statements

Product costs are treated as inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a (an asset) on the balance sheet and do not appear on the income statement as costs of goods sold until the product is sold.

For example, a company manufactures 50 units of widgets at a unit product cost of $5. On the balance sheet, there would be a $5 x 50 = $250 increase in inventory. If the company sells 20 units of widgets, $5 x 20 = $100 in inventory would be transferred to the cost of goods sold on the income statement while the remaining $150 would remain in inventory on the balance sheet.

Download the Free Template

Enter your name and email in the form below and download the free template now!

More Resources

CFI is a global provider of financial modeling classes and administers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification. To continue learning and advancing your career, these other CFI resources will be helpful:

- Cost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total

- Cost of Goods Sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct

- Operating CycleOperating CycleAn Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale

- Inventory AuditAuditing InventoryAuditing inventory is the process of cross-checking financial records with physical inventory and records. It can be completed by auditors and other

-

Understanding Administrative Expenses: A Comprehensive Guide

Administrative expenses refer to the costs incurred by a company or organization that include, but are not limited to, the salaries and benefitsRemunerationRemuneration is any type of compensation or

-

Understanding Assurance Services: Risk Reduction & Improved Decisions

Assurance services are an independent examination of a company’s processes and controls. Assurance aims to reduce information risk by improving the quality or context of the information. &n

Accounting

- Understanding Agency Costs: Protecting Shareholder Interests

- Understanding Fixed Costs: Definition, Examples & Importance

- Understanding Proceeds: Definition, Types & Calculation

- Understanding Explicit Costs: Definition & Examples

- Understanding Inventoriable Costs: Definition & Examples

- Understanding Business Overheads: Costs & Examples

- Period Costs: Definition, Examples & Impact on Financial Statements

- Understanding Variable Costs: Definition & Examples

- Understanding Switching Costs: Barriers to Customer Loyalty

-

Understanding Accounting Policies: A Guide for Businesses

Understanding Accounting Policies: A Guide for BusinessesAccounting policies are rules and guidelines that are selected by a company for use in preparing and presenting its financial statements. Accounting policies are important, as they set a framework, wh...

-

Understanding Accounting Ratios: A Comprehensive Guide

Understanding Accounting Ratios: A Comprehensive GuideAccounting ratios cover a wide array of ratios that are used by accountants and act as different indicators that measure profitability, liquidityLiquidityIn financial markets, liquidity refers to how ...