Understanding Profit: A Key Financial Metric

Profit is the value remaining after a company’s expenses have been paid. It can be found on an income statement. If the value that remains after expenses have been deducted from revenue is positive, the company is said to have a profit, and if the value is negative, then it is said to have a loss (see: P&L statementProfit and Loss Statement (P&L)A profit and loss statement (P&L), or income statement or statement of operations, is a financial report that provides a summary of a). Other terms that mean the same thing are earnings and income.

Types of Profit

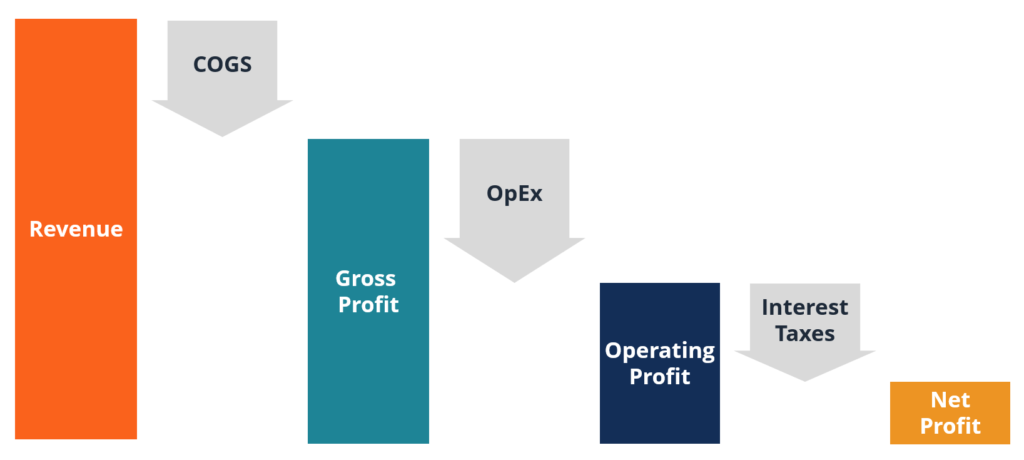

There are three common measures of profit:

1. Gross Profit

Gross profit is the value that remains after the cost of sales, or cost of goods sold (COGS), has been deducted from sales revenue. This is typically the first sub-total on the income statement for most businesses.

2. Operating Profit

Operating profit, also called Earnings Before Interest and Taxes (EBIT)EBIT GuideEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it's found by deducting all operating expenses (production and non-production costs) from sales revenue., is the value that remains after all operating expenses have been deducted from revenue. This is typically the second sub-total on the income statement.

Examples of operating expenses include sales expenses, marketing, advertising, salaries and wages, employee benefits, depreciation, rent, commissions, and any other costs that relate to the ongoing operations of the business.

3. Net Profit

Net profit (also called net income or net earnings) is the value that remains after all expenses, including interest and taxes, have been deducted from revenue. This is the final figure located at the bottom of the income statement.

The net earnings figure includes non-operating expenses such as interest and taxes. It can also be referred to as net income.

Example of Profit

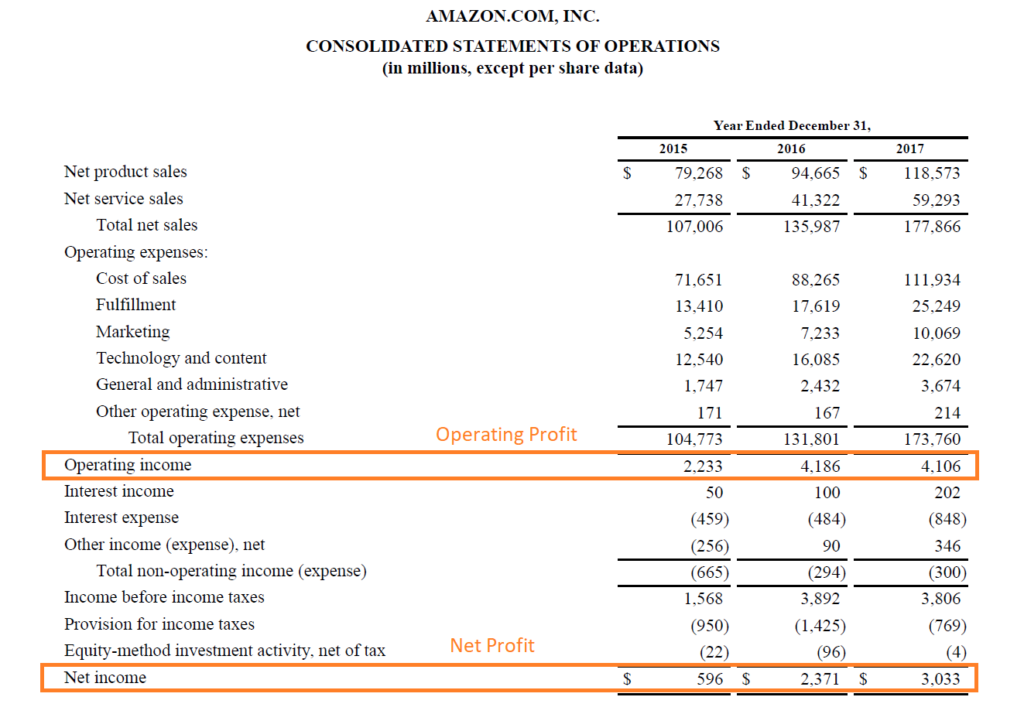

Below is a screenshot of Amazon’s 2017 statement of operation (income statement) from CFI’s Advanced Financial Modeling Course. As you can see, Amazon doesn’t have a gross income subtotal, but it does have an operating income and a net income.

For 2017, by taking net sales of $177.9 billion and subtracting operating expenses of $173.8 billion, you will arrive at the operating income of $4.1 billion. Then, to get to the bottom line, subtract from the amount of interest, taxes, and any other expenses to arrive at the net income of $3.0 billion.

As mentioned previously, it is not a requirement to have a gross profit subtotal, as is the case with Amazon.

Cash Flow vs. Profit

Cash flow and profit are both important metrics when evaluating a company’s performance, and each has its pros and cons as a metric.

Cash flow measures the actual value of cash generated by a company, while income is an accounting figure that uses the accrual principleAccrual PrincipleThe accrual principle is an accounting concept that requires transactions to be recorded in the time period in which they occur, regardless of.

Characteristics of cash flow:

- Shows the actual change in cash over a period of time

- Used in financial modeling and business valuation to calculate the intrinsic value of a firm

- Can be lumpy and uneven depending on the timing of cash inflows and outflows

Characteristics of profit:

- Shows a “smoother” picture of a company’s expenses over time

- Uses accounting principles such as revenue recognition, matching, and accruals

- Includes non-cash expenses such as depreciation, impairment charges, and stock-based compensation

Additional Resources

Thank you for reading this guide to understanding the various metrics of income. CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! designation, designed to transform anyone into a world-class financial analyst. To learn more, these additional CFI resources will be helpful:

- Depreciation MethodsDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits.

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- SG&A ExpensesSG&ASG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing

-

Accounting Profit Explained: Calculation & Importance

Accounting profit is the net income for a company and is calculated by subtracting expenses from revenues, with guidance from the Generally Accepted Accounting Principles (GAAP)GAAPGAAP, G

-

Understanding After-Tax Income: A Comprehensive Guide

After-tax income refers to the net income after deducting all applicable taxes. Therefore, the after-tax income is simply one’s gross income minus taxes. For individuals and corporations, the af

Accounting

- Understanding Accounting Income: A Key Financial Metric

- Accrued Income Explained: Definition & Accounting

- Income Smoothing: Definition, Methods & Implications

- Marginal Profit: Definition, Calculation & Maximization

- Understanding Net Income: A Comprehensive Guide

- Non-Operating Income: Definition, Examples & Significance

- Profit Margin Explained: Types & How to Calculate

- Understanding Revenue: A Comprehensive Guide for Businesses

- Revenue vs. Income: Understanding the Key Differences

-

Understanding Taxable Income: Definition & Calculation

Understanding Taxable Income: Definition & CalculationTaxable income refers to any individual’s or business’ compensation that is used to determine tax liability. The total income amount or gross income is used as the basis to calculate how m...

-

Net Income Explained: A Comprehensive Guide for Businesses & Individuals

Net Income Explained: A Comprehensive Guide for Businesses & IndividualsNet income is revenue minus expenses, interest, and taxes. Here’s what you need to know about net income and why businesses and individuals pay close attention to it.What is net income?Net income is a...