Jumbo CDs: Rates, Benefits & Requirements - [Year]

Jumbo certificates of deposit are usually defined as CDs with balances in excess of $100,000. However, some banks only describe CDs with balances in excess of $1 million as jumbo CDs. The rates paid on jumbo CDs are often higher than the rates available on CDs with smaller balances.

Certificates of Deposit

When you purchase a certificate of deposit you sign a time deposit contract and agree to leave you deposited funds at the bank or credit union for a specific period of time. In return, the financial institution issuing the CD agrees to pay you a fixed rate of interest. Your CD matures at the end of the contract, and at that point you can make withdrawals or additions during a 7- to 10-day grace period. When the grace period ends, any remaining funds roll over into a new CD term.

Loans

Banks use money held in CDs to fund loans. Banks with large deposit bases can fund more loans, and therefore banks offer high interest rates on jumbo CDs in order to attract more deposit money. However, banks also fund loans with money borrowed from the Federal Reserve. When interest rates are low, banks can borrow money inexpensively from the Reserve and do not have to rely on CD money to fund loans. Consequently, banks only offer good rates on jumbo CDs if federal borrowing rates are high.

Insurance

The Federal Deposit Insurance Corporation insures funds held in bank deposit accounts up to $250,000 per person per bank. Funds held at credit unions are insured to the same level by the National Credit Union Administration. Prior to 2008, the FDIC only insured deposits up to $100,000, which meant that earnings on jumbo CDs were not protected. Therefore, in the past, jumbo CD holders were exposing themselves to some risk in the pursuit of higher returns.

Brokerage CDs

Some jumbo CDs take the form of brokerage CDs. These are CDs that banks sell to investment firms. CDs held in brokerage accounts, unlike other securities, are protected by FDIC coverage. Jumbo brokerage CDs typically have term times of just 6 months and are nonrenewable, which means you get your money back when the CD term ends. Some jumbo brokerage CDs are also callable, which means the issuing bank can cancel the CD and give you a return of premium before the CD term ends.

-

Prime Rate Explained: Understanding Interest Rates for Businesses & Consumers

The term “prime rate” (also known as the prime lending rate or prime interest rate) refers to the interest rate that large commercial banks charge on loans and products held by their custo

-

Understanding Recovery Rate: A Key Metric in Credit Risk

Recovery rate, commonly used in credit risk management, refers to the amount recovered when a loan defaults. In other words, the recovery rate is the amount, expressed as a percentage, recovered from

budgeting

- Understanding CD Interest Rates: What's a Good Rate in 2024?

- Hurdle Rate: Definition, Calculation & Importance for Investors

- Understanding Interest Rates: A Comprehensive Guide

- Jumbo CDs: Higher Rates & Deposits Explained

- Understanding Rate of Return: A Comprehensive Guide

- Understanding Dividend Yield: A Comprehensive Guide

- Ex-Ante: Understanding Predictions in Finance

- Understanding LIBOR: What It Is and How It Works

- Understanding Burn Rate: A Key Metric for Startup Success

-

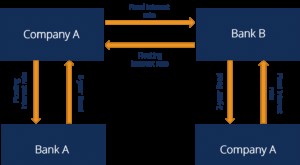

Interest Rate Swaps: A Comprehensive Guide

Interest Rate Swaps: A Comprehensive GuideAn interest rate swap is a type of a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another, based on a specified principal amount. I...

-

Understanding the Overnight Interest Rate: A Comprehensive Guide

Understanding the Overnight Interest Rate: A Comprehensive GuideThe overnight rate refers to the interest rate that depository institutions (e.g., banks or credit unionsCredit UnionA credit union is a type of financial organization that is owned and governed by it...