Understanding Cash Consideration in Mergers & Acquisitions

Cash consideration is the purchase of the outstanding stock shares of a company using cash as the form of payment. An all-cash offer is one way that an acquirer may use to acquire a stake in another company during a merger or acquisitionMergers Acquisitions M&A ProcessThis guide takes you through all the steps in the M&A process. Learn how mergers and acquisitions and deals are completed. In this guide, we'll outline the acquisition process from start to finish, the various types of acquirers (strategic vs. financial buys), the importance of synergies, and transaction costs transaction. Cash consideration is usually preferred by shareholders, although they may, depending on the offer, sometimes prefer other forms of consideration, such as stock or debt instruments.

Also, in a competitive bidding process, shareholders are more likely to accept cash consideration over other forms of payments since cash would not affect the future performance of the combined company. Another scenario where cash consideration may be accepted is when shareholders are uncertain about the viability of the deal, and the acquirer decides to offer a premium priceTakeover PremiumTakeover premium is the difference between the market value (or estimated value) of the company and the actual price to acquire it. using cash only.

How It Works

Cash consideration is the use of cash as a payment option in exchange for an asset or during a merger or acquisition transaction. The transaction is made solely without using other forms of financing such as debtDebtDebt is the money borrowed by one party from another to serve a financial need that otherwise cannot be met outright. Many organizations use debt to procure goods and services that they can’t manage to pay for with cash. or acquirer stock. Cash consideration may be used as a form of payment in the following two types of transactions:

1. Corporate acquisition

In corporate acquisitions, the acquirer can purchase the target company through an all-cash deal. This means that the acquirer will not offer its own stock to the shareholders of the target company, and the equity section of the balance sheet will remain unchanged. Instead, the acquirer will use cash to purchase a majority of the company’s shares.

An all-cash transaction benefits the acquirer in a competitive bidding process since the seller is more likely to consider an all-cash deal rather than other purchase offers that include debt financing. For the seller, accepting cash consideration means that they will forfeit any gains generated by the appreciation of the acquirer’s stocks.

2. Real estate

When purchasing real estateReal EstateReal estate is real property that consists of land and improvements, which include buildings, fixtures, roads, structures, and utility systems. Property rights give a title of ownership to the land, improvements, and natural resources such as minerals, plants, animals, water, etc., the seller may offer cash consideration as the only form of payment for the transaction. It means that the transaction will not include other forms of payment such as a mortgage or debt financing. The seller of the property is likely to accept an all-cash deal over other payment methods even if the latter are higher-priced than the former.

This is because the seller knows that the cash offer is likely to close quickly, and they will receive the whole selling price at closing. The buyer must provide proof of funds during the negotiation process as an assurance to the seller that they are committed to, and capable of, closing the transaction.

Limitations of Cash Consideration

Although cash consideration is preferred over other forms of consideration, it will result in the loss of earning power on the money due to taxation. The sale of shares of the target company is a taxable event. The target’s shareholders will need to pay a tax percentage on the amount of money received from the sale of their holding.

Even if the acquirer pays a premium price for the purchase of the majority of shares of the target company, the tax will eat into this payment. Therefore, shareholders may be better off accepting a stock-for-stock transaction since it is not a taxable event.

Alternatives to Cash Consideration

When executing a merger or acquisition transaction, the seller may offer the following forms of considerations:

1. Acquisition with stock

A stock-for-stock payment is a transaction where the acquirer offers to exchange all shares that shareholders hold in the target company for shares in the acquirer’s company. Shareholders prefer an all-stock payment when they do not want to pay tax on the gains generated. The tax on the profits earned is only recognized when the shareholders decide to dispose of the stake given as compensation for the target company’s shares.

The tax is calculated on the profits earned by a shareholder, which is the difference between the selling price received and the cost basis of the shares. Accepting a stock-for-stock form of payment will mean that the shareholders will not benefit from the short-term liquidity offered by an all-cash deal.

2. Paying with debt

An acquirer may decide to use debt as part of the financing structure for the merger or acquisition transaction. The sellers benefit from debt financing because they will be exempted from paying taxes until the debt payments have been made. Usually, before accepting a structure that includes debt, the seller must confirm that the buyer is in a stable financial condition and will not go bankrupt in the near future.

In case the seller accepts the transaction and the buyer is declared bankrupt soon after, the seller would be classified among other shareholders. They will receive payments last after other senior debtholders have been paid.

Related Readings

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Arm’s Length TransactionArm’s Length TransactionAn arm’s length transaction, also known as the arm’s length principle (ALP), indicates a transaction between two independent parties in which both parties are acting in their own self-interest. Both buyer and seller are independent, possess equal bargaining power, and are not under pressure or duress

- Definitive Purchase AgreementDefinitive Purchase AgreementA Definitive Purchase Agreement (DPA) is a legal document that records the terms and conditions between two companies that enter into an agreement for a merger, acquisition, divestiture, joint venture, or some form of strategic alliance. It is a mutually binding contract

- Negotiated SaleNegotiated SaleA negotiated sale is a technique of offering bonds where the issuing entity and an interested underwriter negotiate the terms of the sale with the buyer. It is sometimes preferred over competitive bidding due to its speed, flexibility, efficiency, and level of confidentiality between the issuer and the underwriter.

- Tender OfferTender OfferA tender offer is a proposal that an investor makes to the shareholders of a publicly traded company. The offer is to tender, or sell, their shares for a specific price at a predetermined time. In some cases, the tender offer may be made by more than one person, such as a group of investors or another business. Tender offers are a commonly used means of acquisition

-

Net Cash: Definition, Calculation & Importance for Businesses

Net cash refers to the position of a company with regard to its liquidity position. To calculate net cash, a company will need to deduct its current liabilities from its cash balance. Liabilities are

-

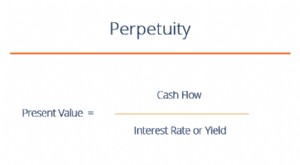

Perpetuity Explained: Understanding Infinite Cash Flows

Perpetuity in the financial system is a situation where a stream of cash flowValuationFree valuation guides to learn the most important concepts at your own pace. These articles will teach you busines

finance

- Bitcoin Cash (BCH): A Comprehensive Overview - Features, History & Future

- Understanding Cash Flow: A Comprehensive Guide

- Cash Management: A Comprehensive Guide to Financial Stability

- Cash-on-Cash Return: Definition, Calculation & Importance

- Cash Ratio: Understanding Your Company's Short-Term Liquidity

- Cash Sweep: Reduce Debt & Maximize Earnings | [Your Company Name]

- Disbursement Explained: Definition, Impact & Accounting Implications

- Understanding Liquidity in Financial Markets: A Comprehensive Guide

- Profit vs. Cash Flow: Understanding the Key Difference

-

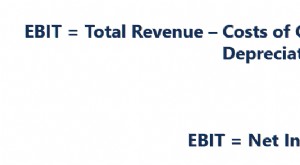

EBIT Explained: Understanding Earnings Before Interest & Taxes

EBIT Explained: Understanding Earnings Before Interest & TaxesEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statementIncome StatementThe Income Statement is one of a companys core financial statements...

-

Understanding Idle Cash: Definition & Impact on Business Finance

Understanding Idle Cash: Definition & Impact on Business FinanceIdle cash is, as the phrase implies, cash that is idle or is not being used in a way that can increase the value of a business. It means that the cash is not earning interestSimple InterestSimple inte...