Cross Guarantee: Definition, Purpose & Examples

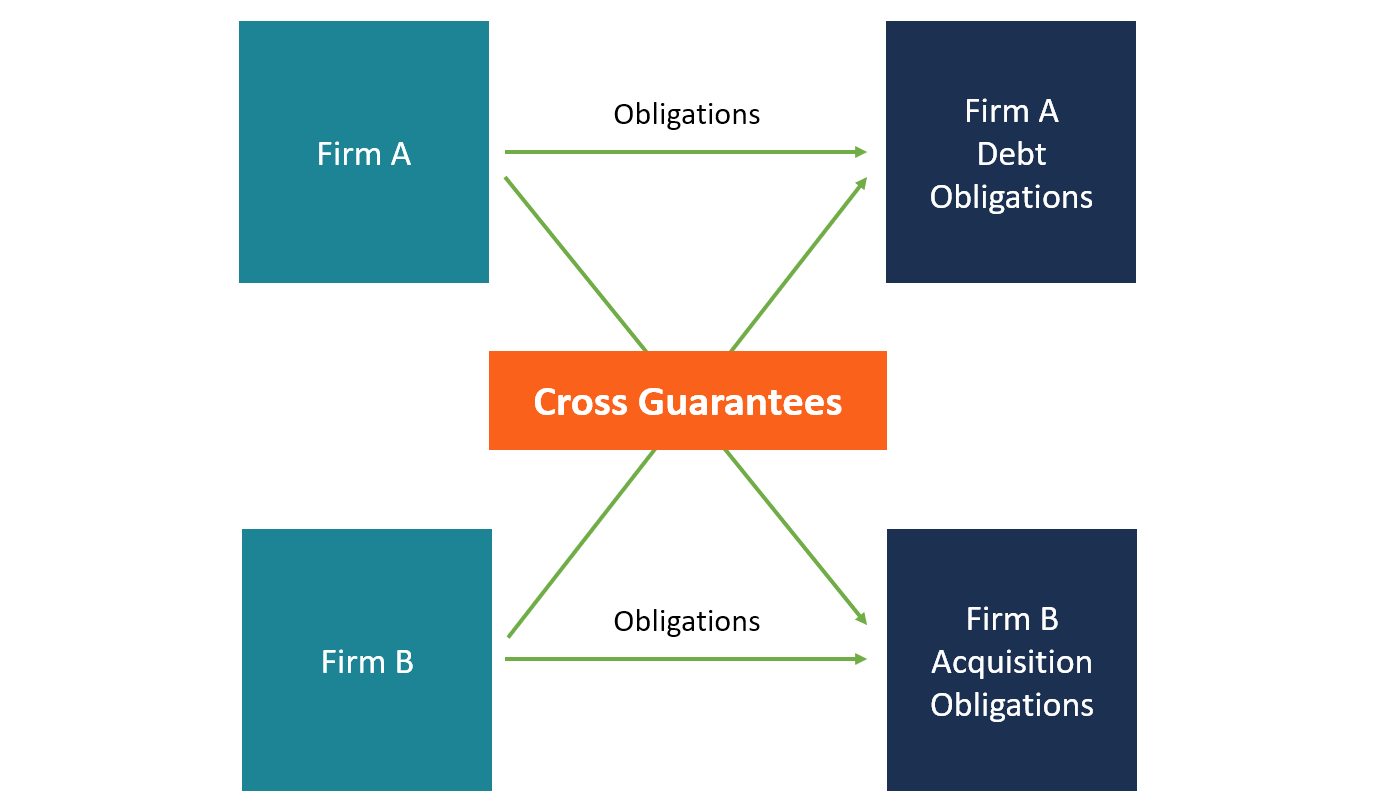

A cross guarantee refers to an arrangement between two or more related companies to provide a guarantee to each other’s obligations. Such a guarantee is commonly made among companies trading under the same group or between a parent company and its subsidiaries. A cross guarantee protects the company that incurred a liability (such as a loanBridge LoanA bridge loan is a short-term form of financing that is used to meet current obligations before securing permanent financing. It provides immediate cash flow when funding is needed but is not yet available. A bridge loan comes with relatively high interest rates and must be backed by some form of collateral) from losing its assets if it defaults on its obligations.

If one company in a group of companies borrows a loan from a bank and the other related companies provide the cross guarantee, the lender receives assurance that the loan will be repaid. If the borrower fails to make principal and interest paymentsInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also on time, the lender may require the guarantors to repay the loan on behalf of the borrower.

How a Cross Guarantee Works

In a cross guarantee agreement, the giver of the guarantee is referred to as the “guarantor” while the person or entity to whom the guarantee is given is referred to as the “obligee” or “creditor.” The person or entity whose payment is secured by the guarantee is referred to as the “principal” or “obligor.” For a public companyPrivate vs Public CompanyThe main difference between a private vs public company is that the shares of a public company are traded on a stock exchange, while a private company's shares are not., the shareholders may be required to approve a cross guarantee before it can take effect.

One of the ways that a cross guarantee works is when a parent and its subsidiarySubsidiaryA subsidiary (sub) is a business entity or corporation that is fully owned or partially controlled by another company, termed as the parent, or holding, company. Ownership is determined by the percentage of shares held by the parent company, and that ownership stake must be at least 51%. guarantee each other’s financial obligations. The parent company commits to paying the lenders if the subsidiary fails to make the agreed payments according to its agreement with a lender. Sometimes, the guarantor may choose to guarantee only a portion of the loan.

Also, when the loan is too large for one company to guarantee, several related companies may offer to cover a pro rata portion of the total loan. If the obligor is unable to make the agreed-upon repayments, each of the guarantors will be responsible for meeting the loan repayment.

Guarantee Agreement

A guarantee agreement is an agreement under which a guarantor agrees to take responsibility for another entity’s financial obligations in the event that that entity is unable to meet the obligations at the agreed time. The agreement also outlines the specific areas that the guarantor promises to provide the guarantee, in the event that it does not guarantee the whole loan.

The guarantee agreement gives the lender an upper hand in the transaction, and the agreement can be executed in a court of law. In essence, the court may view the guarantee agreement as an indemnity bond that compensates the obligee for any losses resulting from the principal’s failure to make periodic payments as required. Therefore, the guarantee agreement serves as an additional form of security.

Disclosure Requirements for Cross Guarantees

According to the Financial Accounting Standards Board (FASB) Interpretation 45, guarantors of financial obligations are required to disclose and record such promises. The guarantor is required to record the fair value of the guarantee as a liability in its books of accounts. The entry should be made at the start of the period when the company provided the guarantee to another. However, Interpretation 45 exempts certain types of companies, such as leasing and insurance companies that provide guarantees in their ordinary course of business.

The FASB requirement also exempts parent companies that are providing a guarantee to their subsidiaries from recording such promises as a liability in their balance sheet. The parent company must, however, disclose the nature of the guarantee, the maximum liability if the company is required to pay the obligor’s debt, and the steps that the guarantor will use to recover the money from the obligor. If the guarantor and the obligor are unrelated companies, the transaction should be recorded in the balance sheet as a liability.

Practical Example of a Cross Guarantee

ABC Company is the parent company of XYZ Company. Subsidiary XYZ intends to acquire new proprietary technology for its motorcycle assembly plant. The technology will cost the company approximately $10 million. NMN Bank already agreed to loan the $10 million to Subsidiary XYZ, on condition that the company receives a guarantee from another company.

As a result, XYZ approached its parent company ABC to become its guarantor for the loan. ABC then agreed to the request and signed a guarantee agreement outlining the amount guaranteed and conditions of the guarantee.

Downstream Guarantee vs. Upstream Guarantee

Downstream and upstream guarantees are the main forms of cross guarantee that involve a parent company and its subsidiaries.

A downstream guarantee is a guarantee provided by the parent company for its subsidiary company, to assure lenders that the subsidiary will honor its financial obligations. In the event that the subsidiary is unable to make its loan repayments, the parent company commits to repay the loan on behalf of the subsidiary.

On the other hand, an upstream guarantee is a form of guarantee in which a subsidiary guarantees its parent company’s debts. An upstream guarantee occurs when the parent company does not own enough assets to pledge as collateral for a loan and includes the subsidiary’s assets to expand its collateral.

Related Readings

Thank you for reading CFI’s explanation of a cross guarantee. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Bridge LoanBridge LoanA bridge loan is a short-term form of financing that is used to meet current obligations before securing permanent financing. It provides immediate cash flow when funding is needed but is not yet available. A bridge loan comes with relatively high interest rates and must be backed by some form of collateral

- Debt CovenantsDebt CovenantsDebt covenants are restrictions that lenders (creditors, debt holders, investors) put on lending agreements to limit the actions of the borrower (debtor).

- Financing ContingencyFinancing ContingencyFinancing contingency refers to a clause that expresses that the offer is contingent on the buyer securing financing for the property.

- Personal GoodwillPersonal GoodwillPersonal goodwill is the intangible value that arises from the efforts or reputation of a business owner or other individual. It means that the value is only associated with the person working within an organization and not the business itself. In accounting and finance, goodwill is an intangible asset

-

Understanding Vouchers: A Guide to Accounts Payable Documents

A voucher is an internal document within a company that is issued by the accounts payable Accounts PayableAccounts payable is a liability incurred when an organization receives goods or services from

-

Holding Companies: Definition, Purpose & How They Work

A holding company is a company that doesn’t conduct any operations, ventures, or other active tasks for itself. Instead, it exists for the purpose of owning assets. In other words, the company d

finance

- Acquirer Definition: Understanding Corporate Acquisitions

- Understanding Clawbacks: Protecting Stakeholders from Failed Performance

- Financial Guarantee: Definition, Types & How They Work

- Understanding Financial Gearing: Debt & Leverage Explained

- Understanding Guarantees: Protecting Lenders and Borrowers

- Letter of Guarantee: Definition, Purpose & How It Works

- Leverage in Finance: Strategies, Types & Risks

- Parent Company Explained: Definition, Control & Examples

- Understanding Cross-Holding: Risks & Implications

-

Goodwill in Accounting: Definition & Value

Goodwill in Accounting: Definition & ValueIn accounting, goodwill is an intangible assetIntangible AssetsAccording to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible as...

-

OIBDA Explained: Understanding Operating Income Before Depreciation & Amortization

OIBDA Explained: Understanding Operating Income Before Depreciation & AmortizationOIBDA is an abbreviation for Operating Income Before Depreciation and Amortization. It is a non-GAAP measure of the financial performance of a company during a specific period of time while excluding ...