Dual-Class Stock Structures: Understanding Voting Rights & Dividends

Dual-class stocks refer to a stock offering structure within a company. A dual-class structure means that a company offers two types (or classes) of stocks.

The purpose of offering class A and class B stocks, for example, is to differentiate between stocks with different dividend payouts and decidedly different voting rightsVoting SharesVoting shares are shares of a company that entitle the shareholder to vote on key issues of the company. It is generally one vote per share. The shares. In most cases, a company offers one class of stock to the general public. The stock class typically provides more limited voting rights attached compared to the other class of stock.

The additional class of stock is typically reserved for executives within the company, company founders, and family members. If a company issues more than two classes of stocks, one may be offered to executives, and another will be given to founders and family.

The additional stock classes are largely regarded as higher-tier shares because they include more voting power. The shares in the higher-tier class are designed to assist company founders (and their family members) and original investors or employees in easily maintaining their majority control of the company.

Summary

- A dual-class stock structure involves one company offering at least two classes of stock – one class with limited voting power is offered to the public, while company executives and founders receive a class with significantly more voting power.

- Today, many tech companies favor dual-class stock structures, although some exchanges will not list companies utilizing them.

- The controversy surrounding dual-class structures is largely related to the fact that while a small pool of individuals possesses the majority of company control through voting rights, it is the general shareholder population that provides most of the capital and, therefore, is exposed to the most risk.

An Example of Dual-Class Stocks

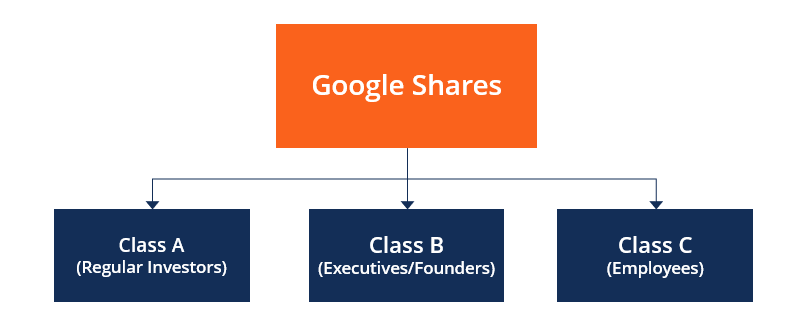

One of the most well-known examples of a dual/multiple class stock structure is that of Google (a subsidiary of Alphabet Inc.). When the massive search engine launched its initial public offering (IPO)Initial Public Offering (IPO)An Initial Public Offering (IPO) is the first sale of stocks issued by a company to the public. Prior to an IPO, a company is considered a private company, usually with a small number of investors (founders, friends, family, and business investors such as venture capitalists or angel investors). Learn what an IPO is in 2004, it claimed a market capitalization ranking in the top 30 around the world.

Because of the fact, the company revealed a stock structure with three classes of shares:

- Class A shares were offered to regular investors; the share class offered one vote per share, as is typically the case with common stock.

- Class B shares were specifically reserved for executives within Google and the company’s founding members; the share class, specifically, rubbed some people the wrong way because it offered ten votes per share to shareholders.

- Class C shares were offered to regular Google employees; the share class provided no voting rights – a rather sharp contrast to the shares granted to key executives.

Another well-known example of dual-class shares is Berkshire Hathaway. Many investors are quite thankful for Warren Buffet’s decision to go with a multiple share class structure because that’s the only way they could ever have invested in Berkshire Hathaway.

Class B stock in Buffet’s conglomerate company is only about $200 a share; however, Berkshire Hathaway Class A goes for around $299,000 a share, which is well out of the price range of most stock investors.

Dual-Class Stocks Throughout History

Dual-class stock structures continue to gain a lot of popularity, specifically in the technology sector. They aren’t a new concept, however. They existed without significant incident until the Dodge Brothers’ automotive company made its IPO and offered only non-voting rights shares to the public.

In response, the New York Stock Exchange (NYSE)New York Stock Exchange (NYSE)The New York Stock Exchange (NYSE) is the largest securities exchange in the world, hosting 82% of the S&P 500, as well as 70 of the biggest outright banned dual-class stock structuring. The exchange was forced to backtrack and reinstate companies with dual-class structures after facing serious competition from other exchanges in the 1980s.

Certain Asian exchanges, for example, allow dual-class structured companies to be listed, while others do not. However, the trend toward increased competition among stock exchanges worldwide means that more and more exchanges are open to dual-class companies.

In contrast, however, stock index companies – such as Standard & Poor’s – are less inclined to accept dual stock structures and, therefore, do not include companies with a dual-class structure in their stock indices.

The Controversy Surrounding Dual-Class Stocks

There is a sizeable amount of controversy when it comes to dual-class stock structures.

Supporters suggest that a dual-class structure simply enables a company’s founders and executives to set the tone and pace for the company. Due to their position relative to the company, they are likely to use extra voting power to support decisions that favor the company’s long-term survivability and profitability.

Additionally, allowing founders to own a class of shares with more voting rights enables them to retain greater control over the company in order to thwart any potential unwanted takeoverHostile TakeoverA hostile takeover, in mergers and acquisitions (M&A), is the acquisition of a target company by another company (referred to as the acquirer) by going directly to the target company’s shareholders, either by making a tender offer or through a proxy vote. The difference between a hostile and a friendly attempts by using their majority voting shares.

Critics of the dual-class structure argue that a small group of shareholders with super privileged voting rights affords them all the control, while the mass majority of shareholders are still providing the bulk of the capital. Risk distribution is, therefore, unevenly balanced in favor of executives and founders.

More and more, support grows for a sort of middle ground where a dual-class structure can exist but be kept somewhat in check. It can be accomplished in a number of ways, including limiting the amount of time such a structure exists or by letting regular shareholders accumulate additional voting interests.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Corporate StructureCorporate StructureCorporate structure refers to the organization of different departments or business units within a company. Depending on a company’s goals and the industry

- Employee Stock Ownership Plan (ESOP)Employee Stock Ownership Plan (ESOP)An Employee Stock Ownership Plan (ESOP) refers to an employee benefit plan that gives the employees an ownership stake in the company. The employer allocates a percentage of the company’s shares to each eligible employee at no upfront cost. The distribution of shares may be based on the employee’s pay scale, terms of

- Founders StockFounders StockFounders stock refers to the equity that is given to the early founders of an organization. This type of stock differs in a few important ways from common stock sold in the secondary market. Key differences are (1) that founders stock can only be issued at face value, and (2) it comes with a vesting schedule.

- Market CapitalizationMarket CapitalizationMarket Capitalization (Market Cap) is the most recent market value of a company’s outstanding shares. Market Cap is equal to the current share price multiplied by the number of shares outstanding. The investing community often uses the market capitalization value to rank companies

-

Understanding Debt Covenants: A Comprehensive Guide

Debt covenants are restrictions that lendersLender of Last ResortA lender of last resort is the provider of liquidity to financial institutions that are experiencing financial difficulties. In most de

-

Understanding Provisions: A Guide to Financial Liabilities

Provisions represent funds put aside by a company to cover anticipated losses in the future. In other words, provision is a liability of uncertain timing and amount. Provisions are listed on a company

finance

- Understanding Domestic Stocks: A Guide for Investors

- Understanding Stocks: A Beginner's Guide to Share Ownership

- Bonds vs. Stocks: A Comprehensive Guide for Investors

- Understanding FAANG Stocks: A Guide to Tech Giants

- Value Stocks Explained: Investing in Undervalued Companies

- Understanding Stock Buybacks: Methods & Impact on Share Value

- Understanding Stocks: A Beginner's Guide to Ownership & Creation

- Stocks Explained: A Beginner's Guide to Investing

- Treasury Stock: Definition, Purpose, and Implications

-

Authorized Shares: Understanding a Company's Issuance Limit

Authorized Shares: Understanding a Company's Issuance LimitAuthorized shares, or authorized stock, are simply a legally allowed maximum number of shares that a company can issue to investors. The number of authorized shares is specified in the company’s...

-

Cash Reserves: Definition, Benefits & Short-Term Needs

Cash Reserves: Definition, Benefits & Short-Term NeedsCash reserves are funds that companies set aside for use in emergency situations. The cash that is saved is used to cover costs or expenses that are unplanned or unexpected. In most cases, the reserve...