Effective Annual Interest Rate (EAR): Understanding & Calculation

The Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compoundingCompound Growth RateThe compound growth rate is a measure used specifically in business and investing contexts, that indicates the growth rate over multiple time periods. It is a measure of the constant growth of a data series. The biggest advantage of the compound growth rate is that the metric takes into consideration the compounding effect. over a given period. Simply put, the effective annual interest rate is the rate of interestInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also that an investor can earn (or pay) in a year after taking into consideration compounding.

EAR can be used to evaluate interest payable on a loan or any debt or to assess earnings from an investment, such as a guaranteed investment certificate (GIC) or savings account.

The effective annual interest rate is also known as the effective interest rate (EIR), annual equivalent rate (AER), or effective rate. Compare it to the Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money. which is based on simple interestSimple InterestSimple interest formula, definition and example. Simple interest is a calculation of interest that doesn't take into account the effect of compounding. In many cases, interest compounds with each designated period of a loan, but in the case of simple interest, it does not. The calculation of simple interest is equal to the principal amount multiplied by the interest rate, multiplied by the number of periods..

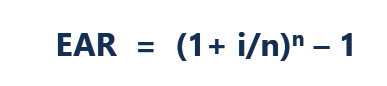

The EAR formula is given below:

Where:

- i = Stated annual interest rate

- n = Number of compounding periods

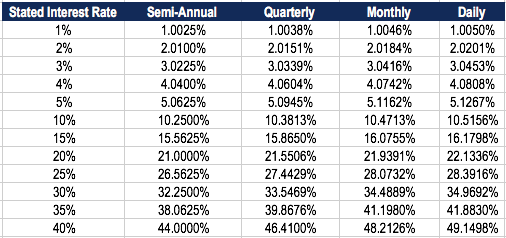

Effective Annual Rate Based on Compounding

The table below shows the difference in the effective annual rate when the compounding periods change.

Table: CFI’s Fixed Income Fundamentals Course

For example, the EAR of a 1% Stated Interest Rate compounded quarterly is 1.0038%.

Importance of Effective Annual Rate

The effective annual interest rate is an important tool that allows the evaluation of the true return on an investment or true interest rate on a loan.

The stated annual interest rate and the effective interest rate can be significantly different, due to compounding. The effective interest rate is important in figuring out the best loan or determining which investment offers the highest rate of return.Internal Rate of Return (IRR)The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

In the case of compounding, the EAR is always higher than the stated annual interest rate.

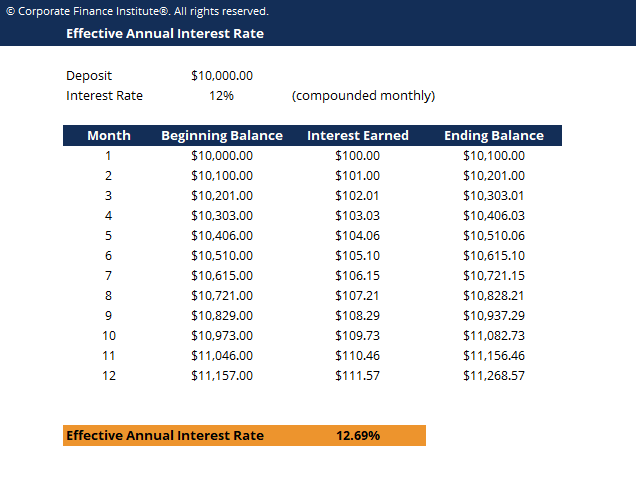

EAR Example

For example, assume the bank offers your deposit of $10,000 a 12% stated interest rate compounded monthly. The table below demonstrates the concept of the effective annual interest rate:

Table: CFI’s Fixed Income Fundamentals Course

Table: CFI’s Fixed Income Fundamentals Course

Month 1 Interest: Beginning Balance ($10,000) x Interest Rate (12%/12 = 1%) = $100

Month 2 Interest: Beginning Balance ($10,100) x Interest Rate (12%/12 = 1%) = $101

The change, in percentage, from the beginning balance ($10,000) to the ending balance ($11,268) is ($11,268 – $10,000)/$10,000 = .12683 or 12.683%, which is the effective annual interest rate. Even though the bank offered a 12% stated interest rate, your money grew by 12.683% due to monthly compounding.

The effective annual interest rate allows you to determine the true return on investment (ROI)ROI Formula (Return on Investment)Return on investment (ROI) is a financial ratio used to calculate the benefit an investor will receive in relation to their investment cost. It is most commonly measured as net income divided by the original capital cost of the investment. The higher the ratio, the greater the benefit earned..

Download the Free Template

Enter your name and email in the form below and download the free template shown above now!

How to Calculate the Effective Interest Rate?

To calculate the effective interest rate using the EAR formula, follow these steps:

1. Determine the stated interest rate

The stated interest rate (also called the annual percentage rate or nominal rate) is usually found in the headlines of the loan or deposit agreement. Example: “Annual rate 36%, interest charged monthly.”

2. Determine the number of compounding periods

The compounding periods are typically monthly or quarterly. The compounding periods may be 12 (12 months in a year) and 4 for quarterly (4 quarters in a year).

For your reference:

- Monthly = 12 compounding periods

- Quarterly = 4 compounding periods

- Bi-Weekly = 26 compounding periods

- Weekly = 52 compounding periods

- Daily = 365 compounding periods

3. Apply the EAR Formula: EAR = (1+ i/n)n – 1

Where:

- i = Stated interest rate

- n = Compounding periods

Example

To calculate the effective annual interest rate of a credit card with an annual rate of 36% and interest charged monthly:

1. Stated interest rate: 36%

2. Number of compounding periods: 12

Therefore, EAR = (1+0.36/12)^12 – 1 = 0.4257 or 42.57%.

Why Don’t Banks Use the Effective Annual Interest Rate?

When banks are charging interest, the stated interest rate is used instead of the effective annual interest rate. This is done to make consumers believe that they are paying a lower interest rate.

For example, for a loan at a stated interest rate of 30%, compounded monthly, the effective annual interest rate would be 34.48%. Banks will typically advertise the stated interest rate of 30% rather than the effective interest rate of 34.48%.

When banks are paying interest on your deposit account, the EAR is advertised to look more attractive than the stated interest rate.

For example, for a deposit at a stated rate of 10% compounded monthly, the effective annual interest rate would be 10.47%. Banks will advertise the effective annual interest rate of 10.47% rather than the stated interest rate of 10%.

Essentially, they show whichever rate appears more favorable.

Related Reading

CFI is a global provider of financial modeling courses and financial analyst certificationBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!. To continue developing your career as a financial professional, check out the following additional CFI resources:

- Expected ReturnExpected ReturnThe expected return on an investment is the expected value of the probability distribution of possible returns it can provide to investors. The return on the investment is an unknown variable that has different values associated with different probabilities.

- Basis PointsBasis Points (BPS)Basis Points (BPS) are the commonly used metric to gauge changes in interest rates. A basis point is 1 hundredth of one percent.

- Capital Gains YieldCapital Gains YieldCapital gains yield (CGY) is the price appreciation on an investment or a security expressed as a percentage. Because the calculation of Capital Gain Yield involves the market price of a security over time, it can be used to analyze the fluctuation in the market price of a security. See calculation and example

- Weighted Average Cost of Capital (WACC)WACCWACC is a firm’s Weighted Average Cost of Capital and represents its blended cost of capital including equity and debt.

-

Understanding the Overnight Interest Rate: A Comprehensive Guide

The overnight rate refers to the interest rate that depository institutions (e.g., banks or credit unionsCredit UnionA credit union is a type of financial organization that is owned and governed by it

-

Prime Rate Explained: Understanding Interest Rates for Businesses & Consumers

The term “prime rate” (also known as the prime lending rate or prime interest rate) refers to the interest rate that large commercial banks charge on loans and products held by their custo

finance

- Effective Annual Interest Rate (EAR): Understanding & Calculation

- Understanding AER: Annual Equivalent Rate Explained

- Understanding Annual Percentage Yield (APY): A Comprehensive Guide

- Binomial Interest Rate Tree: Definition, Uses & Applications

- Effective Annual Rate (EAR): Understanding & Calculation

- Fisher Equation Explained: Understanding Inflation & Interest Rates

- Nominal Interest Rate Explained: Definition & Implications

- Swap Rate Explained: Understanding Fixed Exchange Rates in Derivatives

- Understanding the Policy Interest Rate: Its Impact on the Economy

-

Understanding Interest Rate Risk: Definition & Impact

Understanding Interest Rate Risk: Definition & ImpactInterest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (...

-

Interest Rate Swaps: A Comprehensive Guide

Interest Rate Swaps: A Comprehensive GuideAn interest rate swap is a type of a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another, based on a specified principal amount. I...