Binomial Interest Rate Tree: Definition, Uses & Applications

The binomial interest rate tree is a graphical representation of possible interest rate values at different periods of time, under the assumption that at each time period, the interest rate may either increase or decrease with a certain probability. Essentially, the binomial interest rate tree is concerned with the evolution of short-term interest rates.

Uses of the Binomial Interest Rate Tree

Binomial interest rate trees are primarily used to price bonds (including plain-vanilla bonds, callable bondsCallable BondA callable bond (redeemable bond) is a type of bond that provides the issuer of the bond with the right, but not the obligation, to redeem the bond before its maturity date. The callable bond is a bond with an embedded call option. These bonds generally come with certain restrictions on the call option., and puttable bondsTrading & InvestingCFI's trading & investing guides are designed as self-study resources to learn to trade at your own pace. Browse hundreds of articles on trading, investing and important topics for financial analysts to know. Learn about assets classes, bond pricing, risk and return, stocks and stock markets, ETFs, momentum, technical) and various derivatives whose payoffs are linked to the bonds. The concept of the binomial interest tree also has applications in other pricing models, such as the Black-Derman-Toy model.

Generally, the binomial interest rate tree is a simple and easily understandable approach to projecting future interest rates, which can be used to calculate the price of bonds or derivativesDerivativesDerivatives are financial contracts whose value is linked to the value of an underlying asset. They are complex financial instruments that are. However, the main idea of this model, that the interest rate may either go up or down, may not always properly work in the real world.

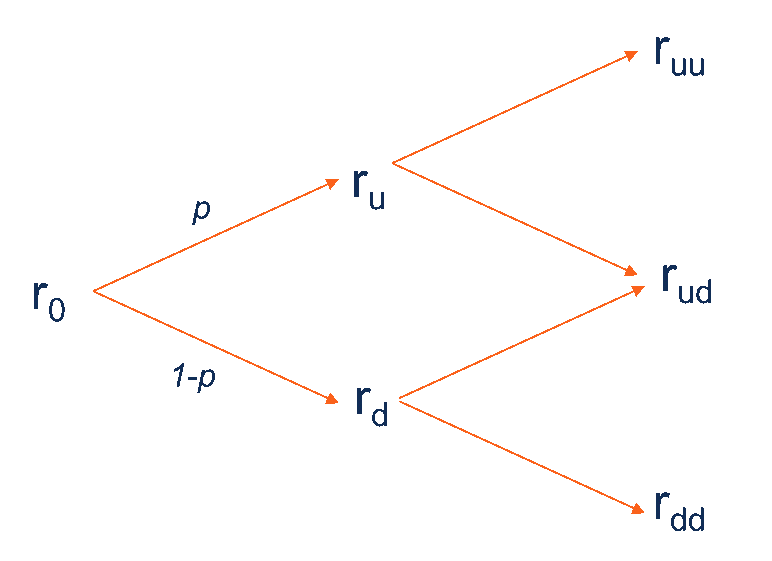

How to Create the Binomial Interest Rate Tree?

The rate tree can be created by following these steps:

- Observe the current interest rate of the relevant security (bond or derivative).

- Determine the probability of the interest rate either going up or down. In most cases, the risk-neutral probability (i.e., the probability of future outcomes adjusted for risk) is used to calculate the future interest rate. Note that if the probability of the interest rate increase equals p, the probability of the interest rate decrease equals (1-p). In addition, the risk-neutral probability can be used for calculating the future rates in all time periods.

- Calculate the forward (future) rates using the determined probability.

- Create the binomial tree using the obtained interest rates. The tree should look like the image above (the binomial interest rate tree for two periods).

Note that similar to other binomial trees, with the binomial interest rate tree, the current price of a bond or derivative must be calculated backward. In other words, we must first calculate the prices of security in the latest periods and then calculate the prices in the previous periods.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Coupon RateCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond.

- Federal ReserveFederal Reserve (The Fed)The Federal Reserve is the central bank of the United States and is the financial authority behind the world’s largest free market economy.

- Floating Interest RateFloating Interest RateA floating interest rate refers to a variable interest rate that changes over the duration of the debt obligation. It is the opposite of a fixed rate.

- Interest Rate SwapInterest Rate SwapAn interest rate swap is a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another

-

Uncovered Interest Rate Parity (UIRP): Explained & Implications

The Uncovered Interest Rate Parity (UIRP) is a financial theory that postulates that the difference in the nominal interest rates between two countries is equal to the relative changes in the foreign

-

Savings Account Interest Rates: What to Expect & How to Maximize Your Returns

When it comes to the interest rate paid on savings accounts, you don't want to be

finance

- Debentures Explained: A Comprehensive Guide to Unsecured Corporate & Government Debt

- Effective Annual Interest Rate (EAR): Understanding & Calculation

- Effective Annual Rate (EAR): Understanding & Calculation

- Fisher Equation Explained: Understanding Inflation & Interest Rates

- Understanding Interest Rates: A Comprehensive Guide

- Interest Rate Parity (IRP): Understanding the Relationship

- Nominal Interest Rate Explained: Definition & Implications

- Swap Rate Explained: Understanding Fixed Exchange Rates in Derivatives

- Understanding the Policy Interest Rate: Its Impact on the Economy

-

Rate of Return vs. Interest Rate: Understanding the Key Differences

Rate of Return vs. Interest Rate: Understanding the Key DifferencesThe rate of return is an internal measure of the return on money invested in a project. The interest rate is the external rate at which money can be borrowed from lenders. Rate of R...

-

Understanding the Net Interest Rate Differential (NIRD)

Understanding the Net Interest Rate Differential (NIRD)Net interest rate differential (NIRD) occurs when there is a difference in interest rates between two countries or regions. It normally takes place in the international foreign exchangeForeign Exchang...