Ratio Analysis: A Comprehensive Guide to Financial Statement Insights

Ratio analysis is a popular technique of financial analysis. It is used to visualize and extract information from financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are. It focuses on ratios that reflect the profitability, efficiency, financing leverageLeverageLverage is a strategy that companies use to increase assets, cash flows, and returns, though it can also magnify losses. There are two main types of leverage, and other vital information about a business. The ratios can be used for both horizontal analysis and vertical analysis. While they are a popular form of analysis, there are many limitations of ratio analysis that financial analystsBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! should be aware of.

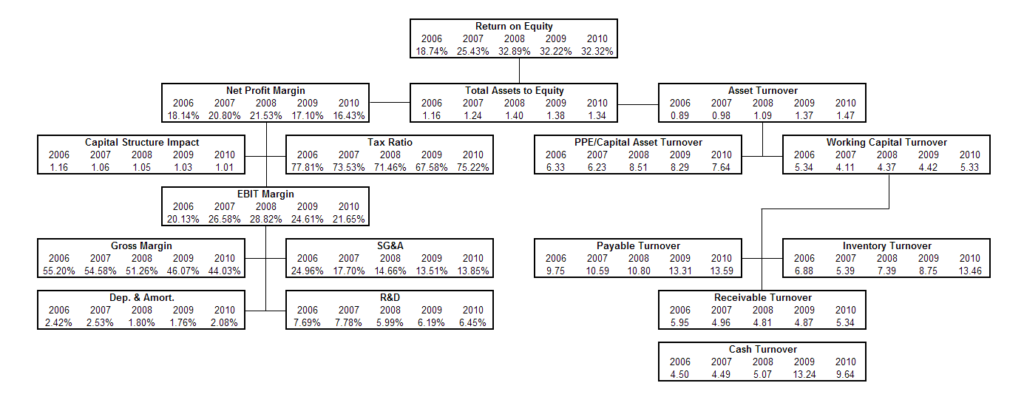

Image: Pyramid of Ratios from CFI’s Financial Analysis Course.

One of the key factors in ratio analysis is the comparison to the benchmark companies of an industry. This type of financial analysis can be useful to both internal managementCorporate StructureCorporate structure refers to the organization of different departments or business units within a company. Depending on a company’s goals and the industry and outsider analysts of the company, as it provides significant insights from the financial statements.

As with any financial analysis technique, there are several limitations of ratio analysis. It is crucial to know these limitations to avoid misleading conclusions.

What are the limitations of ratio analysis?

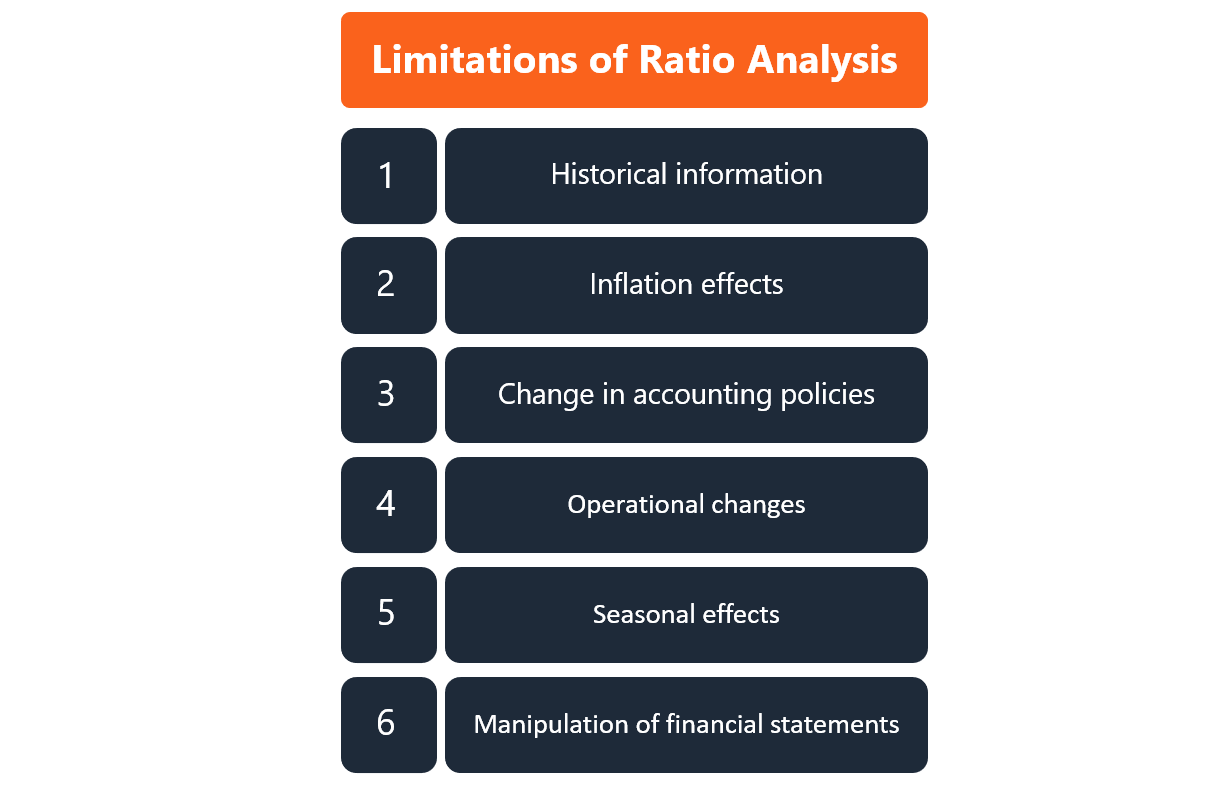

Some of the most important limitations of ratio analysis include:

- Historical Information: Information used in the analysis is based on real past results that are released by the company. Therefore, ratio analysis metrics do not necessarily represent future company performance.

- Inflationary effects: Financial statements are released periodically and, therefore, there are time differences between each release. If inflationInflationInflation is an economic concept that refers to increases in the price level of goods over a set period of time. The rise in the price level signifies that the currency in a given economy loses purchasing power (i.e., less can be bought with the same amount of money). has occurred in between periods, then real prices are not reflected in the financial statements. Thus, the numbers across different periods are not comparable until they are adjusted for inflation.

- Changes in accounting policies: If the company has changed its accounting policies and procedures, this may significantly affect financial reporting. In this case, the key financial metrics utilized in ratio analysis are altered and the financial results recorded after the change are not comparable to the results recorded prior to the change. It is up to the analyst to be up to date with changes to accounting policies. Changes made are generally found in the notes to the financial statements section.

- Operational changes: A company may significantly change its operational structure, anything from their supply chain strategy to the product that they are selling. When significant operational changes occur, the comparison of financial metrics before and after the operational change may lead to misleading conclusions about the company’s performance and future prospects.

- Seasonal effects: An analyst should be aware of seasonal factors that could potentially result in limitations of ratio analysis. The inability to adjust the ratio analysis to the seasonality effects may lead to false interpretations of the results from the analysis.

- Manipulation of financial statements: Ratio analysis is based on information that is reported by the company in its financial statements. This information may be manipulated by the company’s management to report a better result than its actual performance. Hence, ratio analysis may not accurately reflect the true nature of the business, as the misrepresentation of information is not detected by simple analysis. It is important that an analyst is aware of these possible manipulations and always complete extensive due diligenceDue DiligenceDue diligence is a process of verification, investigation, or audit of a potential deal or investment opportunity to confirm all relevant facts and financial information, and to verify anything else that was brought up during an M&A deal or investment process. Due diligence is completed before a deal closes. before reaching any conclusions.

Additional resources

Thank you for reading CFI’s guide to the limitations of ratio analysis. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Financial Modeling Best PracticesFinancial Modeling Best PracticesThis article is to provide readers information on financial modeling best practices and an easy to follow, step-by-step guide to building a financial model.

- Financial Analysis Ratios GlossaryFinancial Analysis Ratios GlossaryGlossary of terms and definitions for common financial analysis ratios terms. It's important to have an understanding of these important terms.

- Profitability RatiosProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit

- Sensitivity AnalysisWhat is Sensitivity Analysis?Sensitivity Analysis is a tool used in financial modeling to analyze how the different values for a set of independent variables affect a dependent variable

-

Financial Literacy: Understanding Key Concepts & Skills

Financial literacy is the cognitive understanding of financial components and skills such as budgeting, investing, borrowing, taxation, and personal financial management. The absence of such skil

-

Financial Mathematics: Applications & Quantitative Finance Explained

Financial mathematics describes the application of mathematics and mathematical modeling to solve financial problems. it is sometimes referred to as quantitative financeQuantitative FinanceQuantitativ

finance

- Understanding Auditors: Roles, Responsibilities & Audit Processes

- Understanding the CAPE Ratio: A Guide to Cyclically Adjusted P/E

- Cash Ratio: Understanding Your Company's Short-Term Liquidity

- Common Size Analysis: A Comprehensive Guide for Financial Statement Analysis

- Common Size Ratios: Understanding and Application

- Contribution Analysis: Understanding Profitability & Cost Management

- Horizontal Analysis: Understanding Financial Trends & Growth

- Financial Analysis: A Comprehensive Guide for Professionals

- Vertical Analysis: A Comprehensive Guide to Financial Statement Analysis

-

Understanding Your Financial Health: A Comprehensive Guide

Understanding Your Financial Health: A Comprehensive GuideFinancial health is a basic measure of the soundness of an individual’s finances – essentially, it’s about what kind of financial shape you’re in overall. You may also view it ...

-

Financial Inclusion: Definition, Benefits & Impact

Financial Inclusion: Definition, Benefits & ImpactFinancial inclusion refers to the provision of equally available and affordable access to financial services for everyone, regardless of their level of income. It applies to providing services to both...