Financial Analysis: A Comprehensive Guide for Professionals

Financial analysis involves using financial dataFinancial DataWhere to find data for financial analysts - Bloomberg, CapitalIQ, PitchBook, EDGAR, SEDAR and more sources of financial data for financial analysts online to assess a company’s performance and make recommendations about how it can improve going forward. Financial AnalystsBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! primarily carry out their work in Excel, using a spreadsheet to analyze historical data and make projections of how they think the company will perform in the future. This guide will cover the most common types of financial analysis performed by professionals. Learn more in CFI’s Financial Analysis Fundamentals Course.

Types of Financial Analysis

The most common types of financial analysis are:

- Vertical

- Horizontal

- Leverage

- Growth

- Profitability

- Liquidity

- Efficiency

- Cash Flow

- Rates of Return

- Valuation

- Scenario & Sensitivity

- Variance

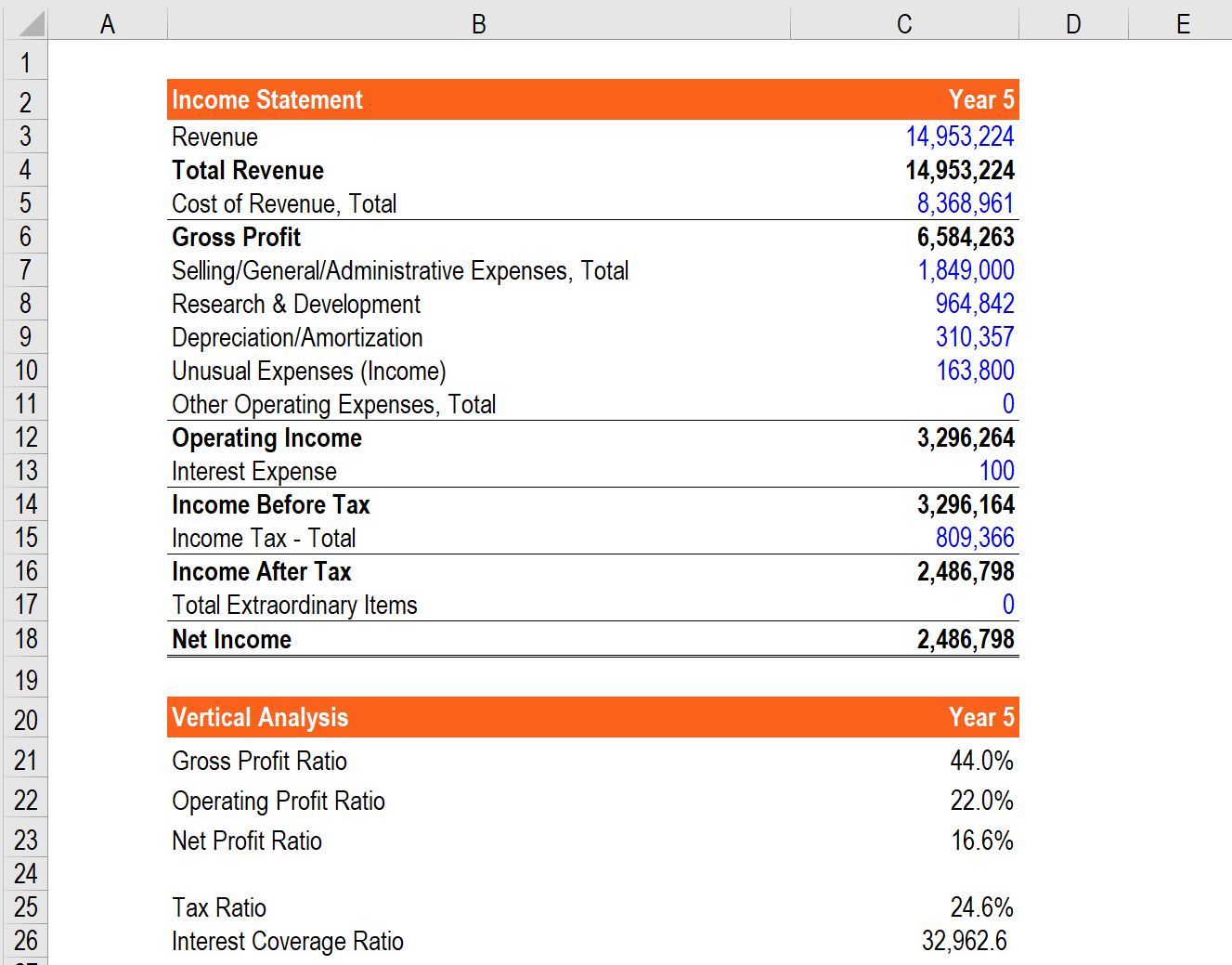

Vertical Analysis

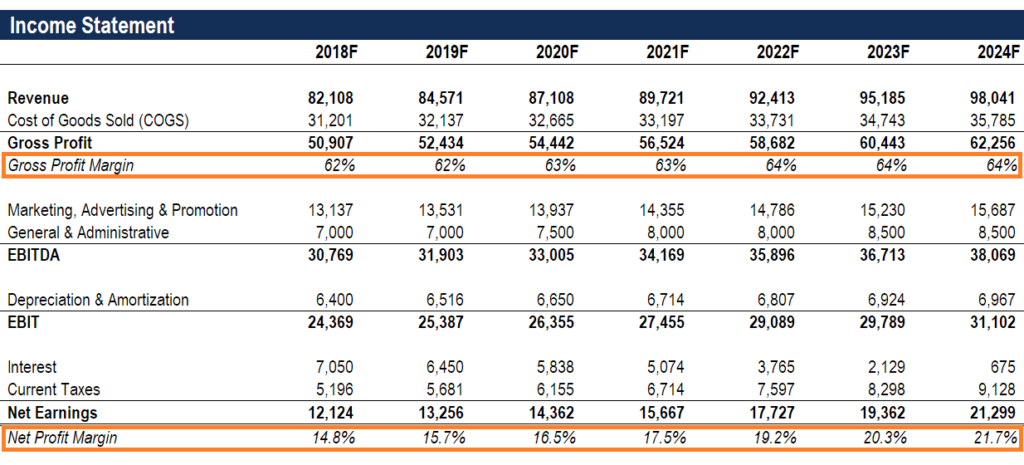

This type of financial analysis involves looking at various components of the income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or and dividing them by revenue to express them as a percentage. For this exercise to be most effective, the results should be benchmarked against other companies in the same industry to see how well the company is performing.

This process is also sometimes called a common-sized income statement, as it allows an analyst to compare companies of different sizes by evaluating their margins instead of their dollars.

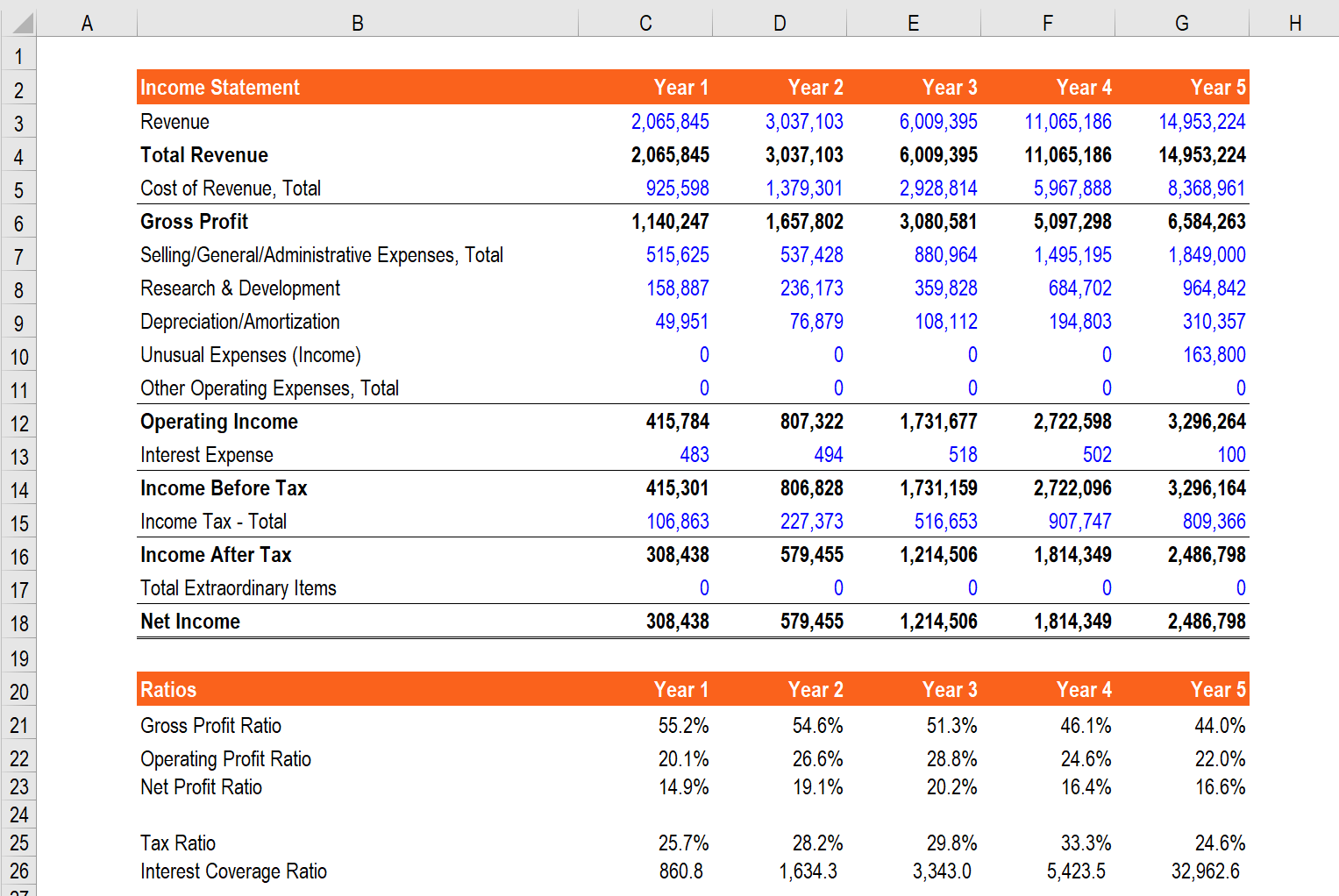

Horizontal Analysis

Horizontal analysis involves taking several years of financial data and comparing them to each other to determine a growth rate. This will help an analyst determine if a company is growing or declining, and identify important trends.

When building financial modelsWhat is Financial ModelingFinancial modeling is performed in Excel to forecast a company's financial performance. Overview of what is financial modeling, how & why to build a model., there will typically be at least three years of historical financial information and five years of forecasted information. This provides 8+ years of data to perform a meaningful trend analysis, which can be benchmarked against other companies in the same industry.

Image: CFI’s Financial Analysis Course.

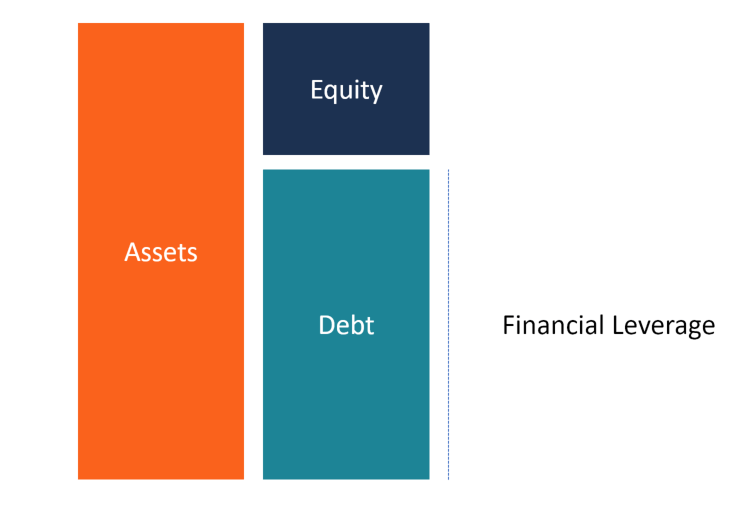

Leverage Analysis

Leverage ratios are one of the most common methods analysts use to evaluate company performance. A single financial metric, like total debt, may not be that insightful on its own, so it’s helpful to compare it to a company’s total equity to get a full picture of the capital structure. The result is the debt/equity ratioDebt to Equity RatioThe Debt to Equity Ratio is a leverage ratio that calculates the value of total debt and financial liabilities against the total shareholder’s equity..

Common examples of ratios include:

- Debt/equityDebt to Equity RatioThe Debt to Equity Ratio is a leverage ratio that calculates the value of total debt and financial liabilities against the total shareholder’s equity.

- Debt/EBITDADebt/EBITDA RatioThe net debt to earnings before interest, taxes, depreciation, and amortization (EBITDA) ratio measures financial leverage and a company’s ability to pay off its debt. Essentially, the net debt to EBITDA ratio (debt/EBITDA) gives an indication as to how long a company would need to operate at its current level to pay off all its debt.

- EBIT/interest (interest coverageInterest Coverage RatioInterest Coverage Ratio (ICR) is a financial ratio that is used to determine the ability of a company to pay the interest on its outstanding debt.)

- Dupont analysisDuPont AnalysisIn the 1920s, the management at DuPont Corporation developed a model called DuPont Analysis for a detailed assessment of the company’s profitability – a combination of ratios, often referred to as the pyramid of ratios, including leverage and liquidity analysis

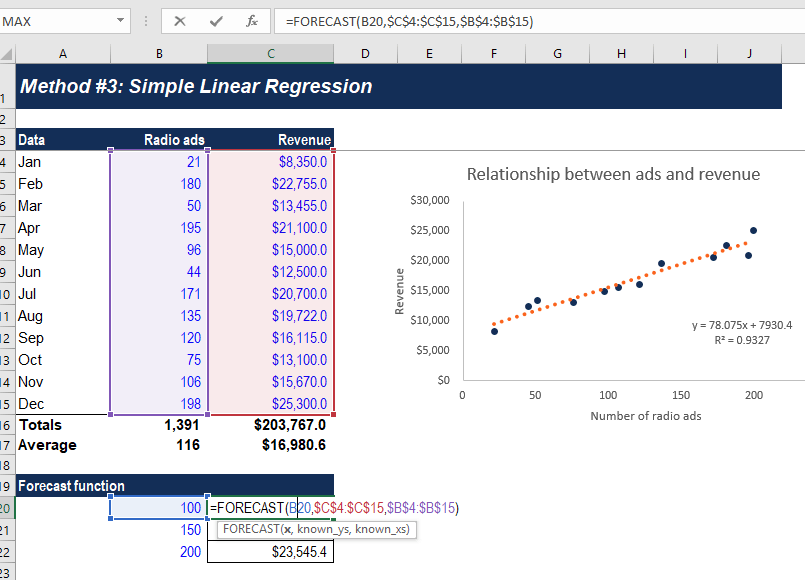

Growth Rates

Analyzing historical growth rates and projecting future ones are a big part of any financial analyst’s job. Common examples of analyzing growth include:

- Year-over-year (YoYYoY (Year over Year)YoY stands for Year over Year and is a type of financial analysis used for comparing time series data. It is useful for measuring growth and detecting trends.)

- Regression analysisRegression AnalysisRegression analysis is a set of statistical methods used to estimate relationships between a dependent variable and one or more independent variables.

- Bottom-up analysis (starting with individual drivers of revenue in the business)

- Top-down analysis (starting with market size and market share)

- Other forecasting methodsForecasting MethodsTop Forecasting Methods. In this article, we will explain four types of revenue forecasting methods that financial analysts use to predict future revenues.

Image: CFI’s Budgeting and Forecasting Course.

Profitability Analysis

Profitability is a type of income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or analysis where an analyst assesses how attractive the economics of a business are. Common examples of profitability measures include:

- Gross marginGross Margin RatioThe Gross Margin Ratio, also known as the gross profit margin ratio, is a profitability ratio that compares the gross profit of a company to its revenue.

- EBITDA marginEBITDA MarginEBITDA margin = EBITDA / Revenue. It is a profitability ratio that measures earnings a company is generating before taxes, interest, depreciation, and amortization. This guide has examples and a downloadable template

- EBIT marginEBIT GuideEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it's found by deducting all operating expenses (production and non-production costs) from sales revenue.

- Net profit marginNet Profit MarginNet Profit Margin (also known as "Profit Margin" or "Net Profit Margin Ratio") is a financial ratio used to calculate the percentage of profit a company produces from its total revenue. It measures the amount of net profit a company obtains per dollar of revenue gained.

Learn more in CFI’s Financial Analysis Fundamentals Course.

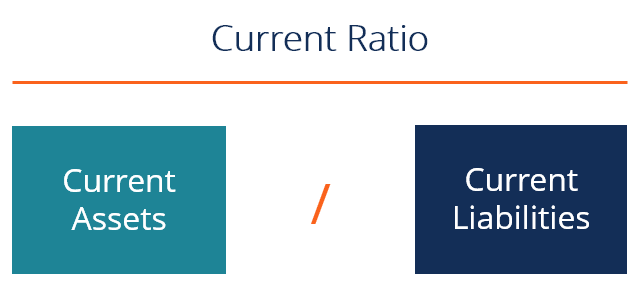

Liquidity Analysis

This is a type of financial analysis that focuses on the balance sheet, particularly, a company’s ability to meet short-term obligations (those due in less than a year). Common examples of liquidity analysis include:

- Current ratioCurrent Ratio FormulaThe Current Ratio formula is = Current Assets / Current Liabilities. The current ratio, also known as the working capital ratio, measures the capability of a business to meet its short-term obligations that are due within a year. The ratio considers the weight of total current assets versus total current liabilities. It indicates the financial health of a company

- Acid testAcid-Test RatioThe Acid-Test Ratio, also known as quick ratio, is a liquidity ratio that measures how sufficient a company's short-term assets can cover current liabilities

- Cash ratioCash RatioThe cash ratio, sometimes referred to as the cash asset ratio, is a liquidity metric that indicates a company’s capacity to pay off short-term debt obligations with its cash and cash equivalents. Compared to other liquidity ratios such as the current ratio and quick ratio, the cash ratio is a stricter, more conservative measure

- Net working capitalNet Working CapitalNet Working Capital (NWC) is the difference between a company's current assets (net of cash) and current liabilities (net of debt) on its balance sheet.

Current Ratio FormulaThe Current Ratio formula is = Current Assets / Current Liabilities. The current ratio, also known as the working capital ratio, measures the capability of a business to meet its short-term obligations that are due within a year. The ratio considers the weight of total current assets versus total current liabilities. It indicates the financial health of a company

Current Ratio FormulaThe Current Ratio formula is = Current Assets / Current Liabilities. The current ratio, also known as the working capital ratio, measures the capability of a business to meet its short-term obligations that are due within a year. The ratio considers the weight of total current assets versus total current liabilities. It indicates the financial health of a company

Efficiency Analysis

Efficiency ratios are an essential part of any robust financial analysis. These ratios look at how well a company manages its assets and uses them to generate revenue and cash flow.

Common efficiency ratios include:

- Asset turnover ratioAsset Turnover RatioThe asset turnover ratio, also known as the total asset turnover ratio, measures the efficiency with which a company uses its assets to produce sales. A company with a high asset turnover ratio operates more efficiently as compared to competitors with a lower ratio.

- Fixed asset turnover ratioFixed Asset TurnoverFixed Asset Turnover (FAT) is an efficiency ratio that indicates how well or efficiently the business uses fixed assets to generate sales. This ratio divides net sales into net fixed assets, over an annual period. The net fixed assets include the amount of property, plant, and equipment less accumulated depreciation

- Cash conversion ratioCash Conversion RatioThe Cash Conversion Ratio (CCR) is a financial management tool used to determine the ratio between the cash flows of a company to its net profit.

- Inventory turnover ratioInventory Turnover RatioThe inventory turnover ratio, also known as the stock turnover ratio, is an efficiency ratio that measures how efficiently inventory is managed. The inventory turnover ratio formula is equal to the cost of goods sold divided by total or average inventory to show how many times inventory is “turned” or sold during a period.

Cash Flow

As they say in finance, cash is king, and, thus, a big emphasis is placed on a company’s ability to generate cash flow. Analysts across a wide range of finance careers spend a great deal of time looking at companies’ cash flow profiles.

The Statement of Cash FlowsStatement of Cash FlowsThe Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements that report the cash is a great place to get started, including looking at each of the three main sections: operating activities, investing activities, and financing activities.

Common examples of cash flow analysis include:

- Operating Cash Flow (OCF)Operating Cash FlowOperating Cash Flow (OCF) is the amount of cash generated by the regular operating activities of a business in a specific time period.

- Free Cash Flow (FCF)Free Cash Flow (FCF)Free Cash Flow (FCF) measures a company’s ability to produce what investors care most about: cash that's available be distributed in a discretionary way.

- Free Cash Flow to the Firm (FCFF)Free Cash Flow to Firm (FCFF)FCFF, or Free Cash Flow to Firm, is cash flow available to all funding providers in a business. debt holders, preferred stockholders, common shareholders

- Free Cash Flow to Equity (FCFE)Free Cash Flow to Equity (FCFE)Free cash flow to equity (FCFE) is the amount of cash a business generates that is available to be potentially distributed to shareholders. It is calculated as Cash from Operations less Capital Expenditures. This guide will provide a detailed explanation of why it’s important and how to calculate it and several

Learn more in CFI’s Financial Analysis Fundamentals Course.

Rates of Return

At the end of the day, investors, lenders, and finance professionals, in general, are focused on what type of risk-adjusted rate of return they can earn on their money. As such, assessing rates of return on investment (ROI) is critical in the industry.

Common examples of rates of return measures include:

- Return on Equity (ROE)Return on Equity (ROE)Return on Equity (ROE) is a measure of a company’s profitability that takes a company’s annual return (net income) divided by the value of its total shareholders' equity (i.e. 12%). ROE combines the income statement and the balance sheet as the net income or profit is compared to the shareholders’ equity.

- Return on Assets (ROA)Return on Assets & ROA FormulaROA Formula. Return on Assets (ROA) is a type of return on investment (ROI) metric that measures the profitability of a business in relation to its total assets.

- Return on invested capital (ROIC)ROICROIC stands for Return on Invested Capital and is a profitability ratio that aims to measure the percentage return that a company earns on invested capital.

- Dividend YieldDividend Yield FormulaThe Dividend Yield is a financial ratio that measures the annual value of dividends received relative to the market value per share of a security. It calculates the percentage of a company’s market price of a share that is paid to shareholders in the form of dividends.. See examples, how to calculate

- Capital GainCapital Gains YieldCapital gains yield (CGY) is the price appreciation on an investment or a security expressed as a percentage. Because the calculation of Capital Gain Yield involves the market price of a security over time, it can be used to analyze the fluctuation in the market price of a security. See calculation and example

- Accounting rate of return (ARR)ARR - Accounting Rate of ReturnAccounting Rate of Return (ARR) is the average net income an asset is expected to generate divided by its average capital cost, expressed as

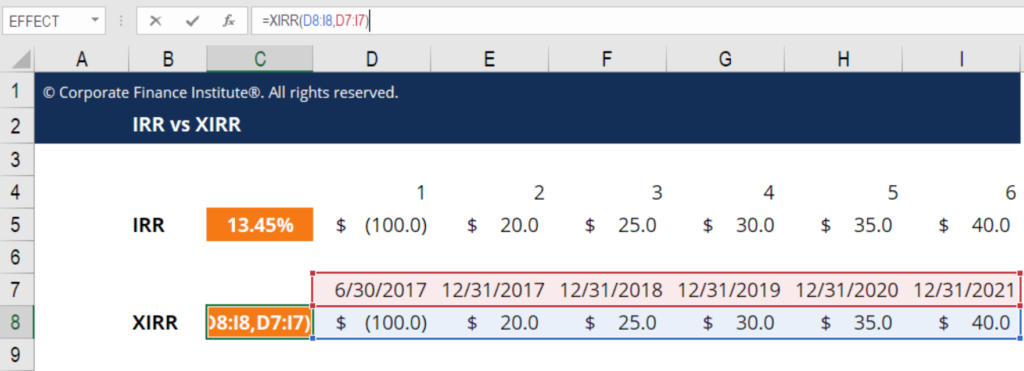

- Internal Rate of Return (IRR)Internal Rate of Return (IRR)The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

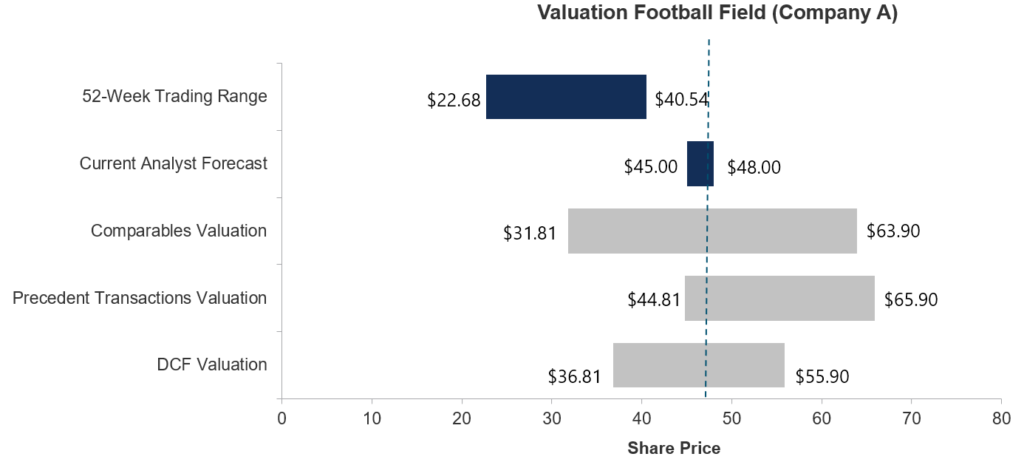

Valuation Analysis

The process of estimating what a business is worth is a major component of financial analysis, and professionals in the industry spend a great deal of time building financial modelsTypes of Financial ModelsThe most common types of financial models include: 3 statement model, DCF model, M&A model, LBO model, budget model. Discover the top 10 types in Excel. The value of a business can be assessed in many different ways, and analysts need to use a combination of methods to arrive at a reasonable estimation.

Approaches to valuation include:

- Cost Approach

- The cost to build/replace

- Relative Value (market approach)

- Comparable company analysisComparable Company AnalysisThis guide shows you step-by-step how to build comparable company analysis ("Comps") and includes a free template and many examples.

- Precedent transactionsPrecedent Transaction AnalysisPrecedent transaction analysis is a method of company valuation where past M&A transactions are used to value a comparable business today.

- Intrinsic Value

- Discounted cash flow analysisDCF Model Training Free GuideA DCF model is a specific type of financial model used to value a business. The model is simply a forecast of a company’s unlevered free cash flow

Learn more in CFI’s Valuation Modeling Course.

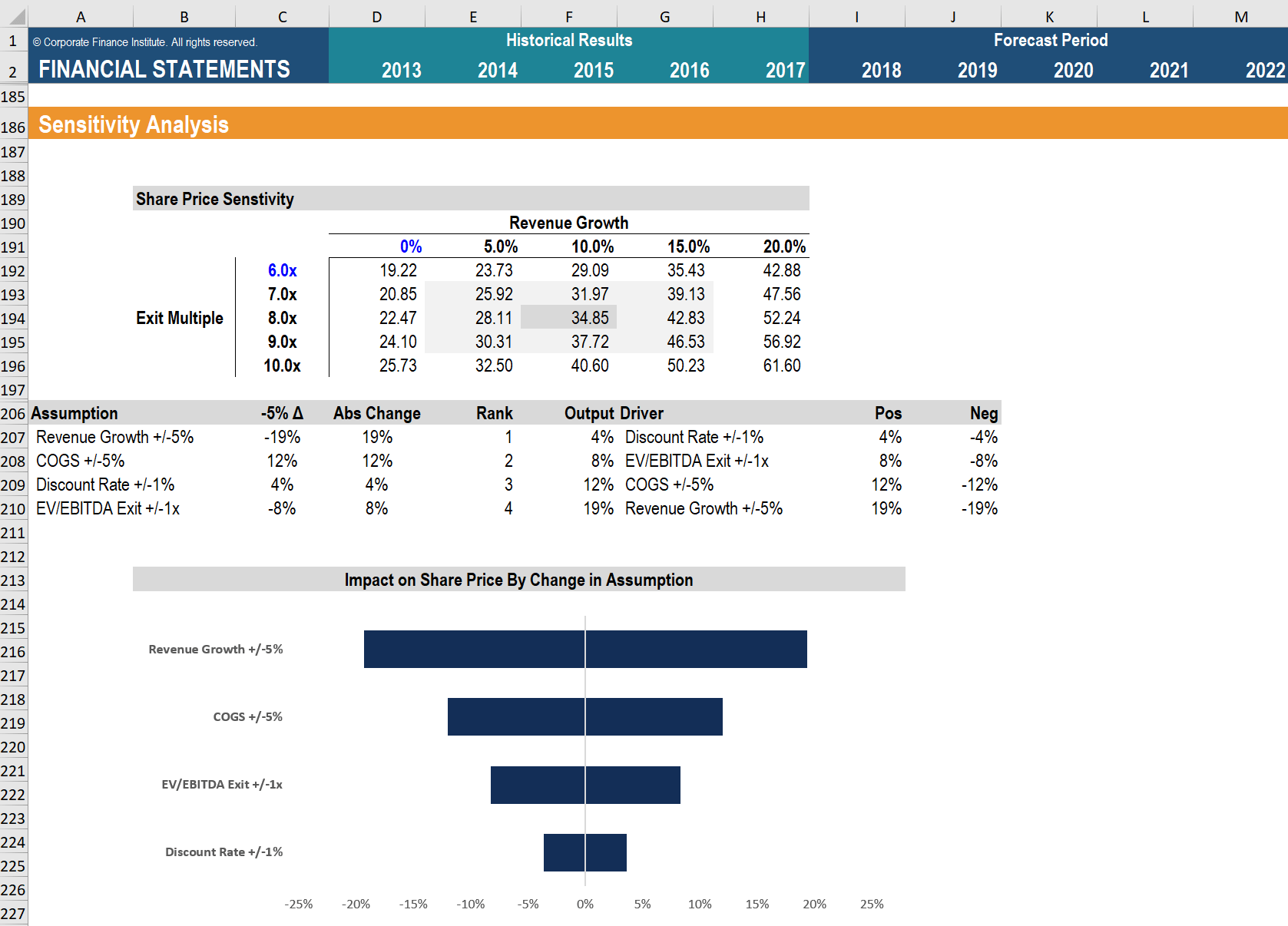

Scenario & Sensitivity Analysis

Another component of financial modeling and valuation is performing scenario and sensitivity analysisWhat is Sensitivity Analysis?Sensitivity Analysis is a tool used in financial modeling to analyze how the different values for a set of independent variables affect a dependent variable as a way of measuring risk. Since the task of building a model to value a company is an attempt to predict the future, it is inherently very uncertain.

Building scenarios and performing sensitivity analysis can help determine what the worst-case or best-case future for a company could look like. Managers of businesses working in financial planning and analysis (FP&A)FP&A RoleThe Financial Planning & Analysis (FP&A) role is gaining greater importance today as it helps bring out crucial analysis on business performance. An FP&A role is no longer limited to management reporting but it also requires lots of business insights so that the top management will often prepare these scenarios to help a company prepare its budgets and forecasts.

Investment analysts will look at how sensitive the value of a company is as changes in assumptions flow through the model using Goal SeekGoal SeekThe Goal Seek Excel function (What-if-Analysis) is a method of solving for a desired output by changing an assumption that drives it. The function uses a trial and error approach to back-solving the problem by plugging in guesses until it arrives at the answer. It is used for performing sensitivity analysis in Excel and Data TablesData TablesData tables are used in Excel to display a range of outputs given a range of different inputs. They are commonly used in financial modeling and analysis to assess a range of different possibilities for a company, given uncertainty about what will happen in the future..

Check out CFI’s Sensitivity Analysis Course to learn more!

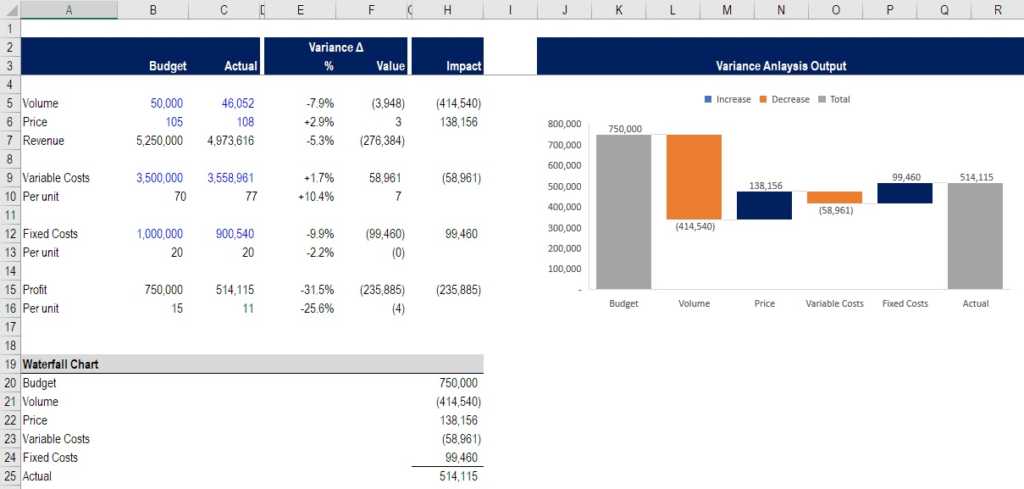

Variance Analysis

Variance analysisVariance AnalysisVariance analysis can be summarized as an analysis of the difference between planned and actual numbers. The sum of all variances gives a is the process of comparing actual results to a budgetTypes of BudgetsThere are four common types of budgeting methods that companies use: (1) incremental, (2) activity-based, (3) value proposition, and (4) or forecastFinancial ForecastingFinancial forecasting is the process of estimating or predicting how a business will perform in the future. This guide on how to build a financial forecast. It is a very important part of the internal planning and budgeting process at an operating company, particularly for professionals working in the accounting and finance departments.

The process typically involves looking at whether a variance was favorable or unfavorable and then breaking it down to determine what the root cause of it was. For example, a company had a budget of $2.5 million of revenue and had actual results of $2.6 million. This results in a $0.1 million favorable variance, which was due to higher than expected volumes (as opposed to higher prices).

Learn more in CFI’s Budgeting and Forecasting Course.

Financial Analysis Best Practices

All of the above methods are commonly performed in Excel using a wide range of formulas, functions, and keyboard shortcutsShortcutsExcel shortcuts guide - all the most important Excel shortcuts to save you time and speed up your financial modeling. Master these shortcuts to become. Analysts need to be sure they are using best practices when performing their work, given the enormous value that’s at stake and the propensity of large data sets to have errors.

Best practices include:

- Being extremely organized with data

- Keeping all formulasFinancial Modeling Formulas and calculations as simple as possible

- Making notes and comments in cells

- Auditing and stress testing spreadsheets

- Having several individuals review the work

- Building in redundancy checks

- Using data tables and charts/graphsTypes of GraphsTop 10 types of graphs for data presentation you must use - examples, tips, formatting, how to use them for effective communication and in presentations. to present data

- Making sound, data-based assumptions

- Extreme attention to detail, while keeping the big picture in mind

Video Explanation of Types of Financial Analysis

Watch this short video to quickly understand the twelve different types of financial analysis covered in this guide.

Additional Resources

Thank you for reading this CFI guide to types of financial analysis. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification, designed to transform anyone into a world-class analyst. To learn more and continue advancing your career, these additional CFI resources will be helpful:

- Comparable Company AnalysisComparable Company AnalysisThis guide shows you step-by-step how to build comparable company analysis ("Comps") and includes a free template and many examples.

- Financial RatiosFinancial RatiosFinancial ratios are created with the use of numerical values taken from financial statements to gain meaningful information about a company

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

-

Comprehensive Financial Planning: Your Path to Financial Security

A financial plan is a document that covers an individual’s current financial situation, short-term and long-term economic goals, and an in-depth strategy to achieve the goals. A finan

-

Understanding Financial Systems: Institutions & Key Players

A financial system is a network of financial institutions – such as insurance companies, stock exchanges, and investment banksList of Top Investment BanksList of the top 100 investment banks in

finance

- Understanding Auditors: Roles, Responsibilities & Audit Processes

- Common Size Analysis: A Comprehensive Guide for Financial Statement Analysis

- Contribution Analysis: Understanding Profitability & Cost Management

- Credit Analysis: A Comprehensive Guide to Assessing Credit Risk

- EBITDARM Explained: A Comprehensive Guide to Financial Analysis

- Eurocurrency Explained: What It Is & How It Works

- Horizontal Analysis: Understanding Financial Trends & Growth

- Ratio Analysis: A Comprehensive Guide to Financial Statement Insights

- Vertical Analysis: A Comprehensive Guide to Financial Statement Analysis

-

Financial Mathematics: Applications & Quantitative Finance Explained

Financial Mathematics: Applications & Quantitative Finance ExplainedFinancial mathematics describes the application of mathematics and mathematical modeling to solve financial problems. it is sometimes referred to as quantitative financeQuantitative FinanceQuantitativ...

-

Understanding Financial Performance: A Comprehensive Overview

Understanding Financial Performance: A Comprehensive OverviewFinancial performance is a complete evaluation of a company’s overall standing in categories such as assets, liabilities, equity, expenses, revenue, and overall profitability. It is measured thr...