Understanding Liquidity Ratios: A Guide to Short-Term Solvency

A liquidity ratio is a type of financial ratio used to determine a company’s ability to pay its short-term debt obligations. The metric helps determine if a company can use its current, or liquid, assets to cover its current liabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the.

Three liquidity ratios are commonly used – the current ratio, quick ratio, and cash ratio. In each of the liquidity ratios, the current liabilities amount is placed in the denominator of the equation, and the liquid assets amount is placed in the numerator.

Given the structure of the ratio, with assets on top and liabilities on the bottom, ratios above 1.0 are sought after. A ratio of 1 means that a company can exactly pay off all its current liabilities with its current assets. A ratio of less than 1 (e.g., 0.75) would imply that a company is not able to satisfy its current liabilities.

A ratio greater than 1 (e.g., 2.0) would imply that a company is able to satisfy its current bills. In fact, a ratio of 2.0 means that a company can cover its current liabilities two times over. A ratio of 3.0 would mean they could cover their current liabilities three times over, and so forth.

Summary

- A liquidity ratio is used to determine a company’s ability to pay its short-term debt obligations.

- The three main liquidity ratios are the current ratio, quick ratio, and cash ratio.

- When analyzing a company, investors and creditors want to see a company with liquidity ratios above 1.0. A company with healthy liquidity ratios is more likely to be approved for credit.

Types of Liquidity Ratios

1. Current Ratio

Current Ratio = Current Assets / Current Liabilities

The current ratio is the simplest liquidity ratio to calculate and interpret. Anyone can easily find the current assetsCurrent AssetsCurrent assets are all assets that a company expects to convert to cash within one year. They are commonly used to measure the liquidity of a and current liabilities line items on a company’s balance sheet. Divide current assets by current liabilities, and you will arrive at the current ratio.

2. Quick Ratio

Quick Ratio = (Cash + Accounts Receivables + Marketable Securities) / Current Liabilities

The quick ratio is a stricter test of liquidity than the current ratio. Both are similar in the sense that current assets is the numerator, and current liabilities is the denominator.

However, the quick ratio only considers certain current assets. It considers more liquid assets such as cash, accounts receivablesAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow, and marketable securities. It leaves out current assets such as inventory and prepaid expenses because the two are less liquid. So, the quick ratio is more of a true test of a company’s ability to cover its short-term obligations.

3. Cash Ratio

Cash Ratio = (Cash + Marketable Securities) / Current Liabilities

The cash ratio takes the test of liquidity even further. This ratio only considers a company’s most liquid assets – cash and marketable securities. They are the assets that are most readily available to a company to pay short-term obligations.

In terms of how strict the tests of liquidity are, you can view the current ratio, quick ratio, and cash ratio as easy, medium, and hard.

Important Notes

Since the three ratios vary by what is used in the numerator of the equation, an acceptable ratio will differ between the three. It is logical because the cash ratio only considers cash and marketable securitiesMarketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion. in the numerator, whereas the current ratio considers all current assets.

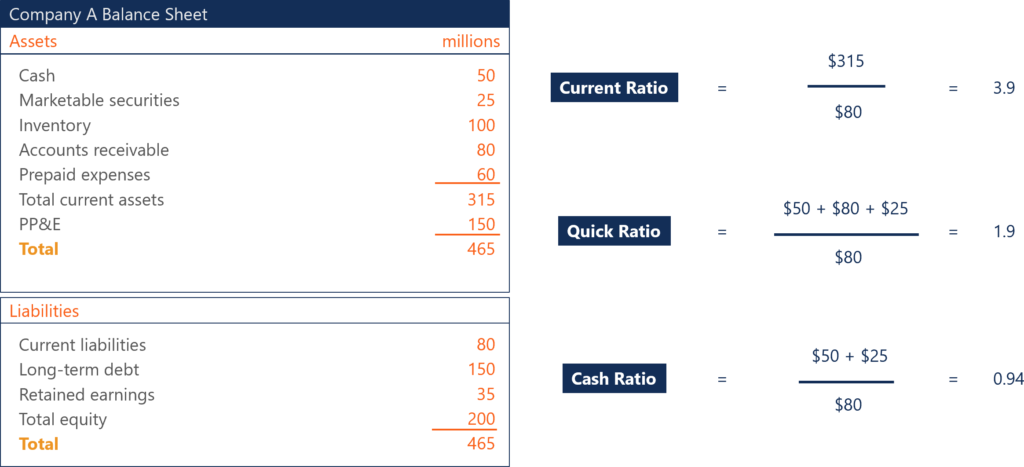

Therefore, an acceptable current ratio will be higher than an acceptable quick ratio. Both will be higher than an acceptable cash ratio. For example, a company may have a current ratio of 3.9, a quick ratio of 1.9, and a cash ratio of 0.94. All three may be considered healthy by analysts and investors, depending on the company.

Importance of Liquidity Ratios

1. Determine the ability to cover short-term obligations

Liquidity ratios are important to investors and creditors to determine if a company can cover their short-term obligations, and to what degree. A ratio of 1 is better than a ratio of less than 1, but it isn’t ideal.

Creditors and investors like to see higher liquidity ratios, such as 2 or 3. The higher the ratio is, the more likely a company is able to pay its short-term bills. A ratio of less than 1 means the company faces a negative working capital and can be experiencing a liquidity crisis.

2. Determine creditworthiness

Creditors analyze liquidity ratios when deciding whether or not they should extend credit to a company. They want to be sure that the company they lend to has the ability to pay them back. Any hint of financial instability may disqualify a company from obtaining loans.

3. Determine investment worthiness

For investors, they will analyze a company using liquidity ratios to ensure that a company is financially healthy and worthy of their investment. Working capital issues will put restraints on the rest of the business as well. A company needs to be able to pay its short-term bills with some leeway.

Low liquidity ratios raise a red flag, but “the higher, the better” is only true to a certain extent. At some point, investors will question why a company’s liquidity ratios are so high. Yes, a company with a liquidity ratio of 8.5 will be able to confidently pay its short-term bills, but investors may deem such a ratio excessive. An abnormally high ratio means the company holds a large amount of liquid assets.

For example, if a company’s cash ratio was 8.5, investors and analysts may consider that too high. The company holds too much cash on hand, which isn’t earning anything more than the interest the bank offers to hold their cash. It can be argued that the company should allocate the cash amount towards other initiatives and investments that can achieve a higher return.

With liquidity ratios, there is a balance between a company being able to safely cover its bills and improper capital allocation. Capital should be allocated in the best way to increase the value of the firm for shareholders.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Current DebtCurrent DebtOn a balance sheet, current debt is debts due to be paid within one year (12 months) or less. It is listed as a current liability and part of

- Quick RatioQuick RatioThe Quick Ratio, also known as the Acid-test, measures the ability of a business to pay its short-term liabilities with assets readily convertible into cash

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Ratio AnalysisRatio AnalysisRatio analysis refers to the analysis of various pieces of financial information in the financial statements of a business. They are mainly used by external analysts to determine various aspects of a business, such as its profitability, liquidity, and solvency.

-

Quick Ratio: Understanding Your Business's Short-Term Liquidity

The Quick Ratio, also known as the Acid-test or Liquidity ratio, measures the ability of a business to pay its short-term liabilities by having assets that are readily convertible into cashCash Equiva

-

Reserve Ratio Explained: Understanding Bank Reserves

The reserve ratio – also known as bank reserve ratio, bank reserve requirement, or cash reserve ratio – is the percentage of deposits a financial institution must hold in reserve as cash.

finance

- Grocery Store Liquidity Ratio: Understanding Industry Standards

- Cash Ratio: Understanding Your Company's Short-Term Liquidity

- Current Ratio: Definition, Calculation & Financial Health

- Understanding Liquidity in Financial Markets: A Comprehensive Guide

- Understanding Liquidity Ratios: A Guide to Short-Term Solvency

- Hedge Ratio: A Comprehensive Guide to Risk Management

- Volatility Ratio: Understanding Price Changes for Trading & Investing

- Understanding Current Assets: Definition & Importance

- Understanding Current Debt: Definition & Implications

-

Liquidity Premium: Definition, Calculation & Investment Implications

Liquidity Premium: Definition, Calculation & Investment ImplicationsA liquidity premium compensates investors for investing in securities with low liquidity. Liquidity refers to how easily an investment can be sold for cash. T-billsTreasury Bills (T-Bills)Treasury Bil...

-

Operating Ratio: Definition, Calculation & Importance

Operating Ratio: Definition, Calculation & ImportanceThe operating ratio is a measure of efficiency that is used by management to determine day-to-day operational performance. This metric compares operating expenses, also known as OPEX, to net sales. Th...