Quick Ratio: Understanding Your Business's Short-Term Liquidity

The Quick Ratio, also known as the Acid-test or Liquidity ratio, measures the ability of a business to pay its short-term liabilities by having assets that are readily convertible into cashCash EquivalentsCash and cash equivalents are the most liquid of all assets on the balance sheet. Cash equivalents include money market securities, banker's acceptances. These assets are, namely, cash, marketable securities,Marketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion. and accounts receivableAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow. These assets are known as “quick” assets since they can quickly be converted into cash.

The Quick Ratio Formula

Quick Ratio = [Cash & equivalents + marketable securities + accounts receivable] / Current liabilities

Or, alternatively,

Quick Ratio = [Current Assets – Inventory – Prepaid expenses] / Current Liabilities

Example

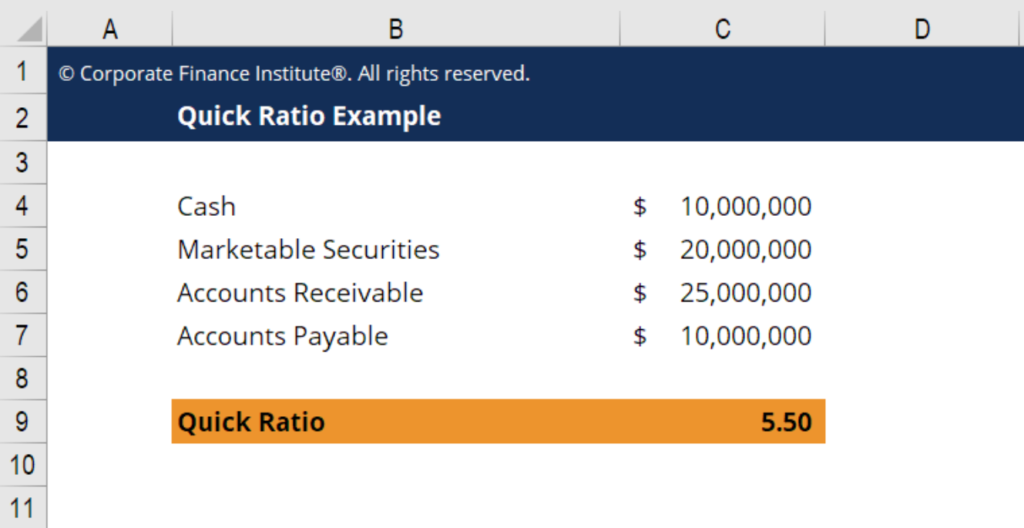

For example, let’s assume a company has:

- Cash: $10 Million

- Marketable Securities: $20 Million

- Accounts Receivable: $25 Million

- Accounts Payable: $10 Million

This company has a liquidity ratio of 5.5, which means that it can pay its current liabilities 5.5 times over using its most liquid assets. A ratio above 1 indicates that a business has enough cash or cash equivalents to cover its short-term financial obligations and sustain its operations.

The formula in cell C9 is as follows = (C4+C5+C6) / C7

This formula takes cash, plus securities, plus AR, and then divides that total by AP (the only liability in this example).

The result is 5.5.

Download the Free Template

Enter your name and email in the form below and download the free template now!

What’s Included and Excluded?

Generally speaking, the ratio includes all current assets, except:

- Prepaid expenses – because they can not be used to pay other liabilities

- Inventory – because it may take too long to convert inventory to cash to cover pressing liabilities

As you can see, the ratio is clearly designed to assess companies where short-term liquidity is an important factor. Hence, it is commonly referred to as the Acid Test.

The Quick Ratio In Practice

The quick ratio is the barometer of a company’s capability and inability to pay its current obligations. Investors, suppliers, and lenders are more interested to know if a business has more than enough cash to pay its short-term liabilities rather than when it does not. Having a well-defined liquidity ratio is a signal of competence and sound business performance that can lead to sustainable growth.

To learn more about this ratio and other important metrics, check out CFI’s course on performing financial analysis.

Quick Ratio vs Current Ratio

The quick ratio is different from the current ratio,FinanceCFI's Finance Articles are designed as self-study guides to learn important finance concepts online at your own pace. Browse hundreds of articles! as inventory and prepaid expense accounts are not considered in quick ratio because, generally speaking, inventories take longer to convert into cash and prepaid expense funds cannot be used to pay current liabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the. For some companies, however, inventories are considered a quick asset – it depends entirely on the nature of the business, but such cases are extremely rare.

Additional Resources

Thank you for reading this guide to understanding the Acid Test as a measure of a company’s liquidity. CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! for financial modeling analysts. This program focuses heavily on Excel, accounting, and financial modeling skills.

To keep learning and advancing your career as a financial analyst, these additional CFI resources will help you on your way:

- Profitability RatiosProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit

- Forward PE RatioForward P/E RatioThe Forward P/E ratio divides the current share price by the estimated future earnings per share. P/E ratio example, formula, and Excel template.

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Financial Modeling Best Practices GuideFinancial Modeling Best PracticesThis article is to provide readers information on financial modeling best practices and an easy to follow, step-by-step guide to building a financial model.

-

Calmar Ratio: Measuring Risk-Adjusted Investment Performance

The Calmar ratio is a formula that measures the performance of an investment fund – such as a hedge fundHedge FundA hedge fund, an alternative investment vehicle, is a partnership where investor

-

Portfolio Turnover Ratio: Definition, Calculation & Significance

The portfolio turnover ratio is the rate of which assets in a fund are bought and sold by the portfolio managers. In other words, the portfolio turnover ratio refers to the percentage change of the as

finance

- Acid-Test Ratio: Understanding Your Company's Short-Term Liquidity

- Advertising to Sales Ratio: Measuring Ad Effectiveness & ROI

- Understanding the CAPE Ratio: A Guide to Cyclically Adjusted P/E

- Current Ratio: Definition, Calculation & Financial Health

- Debt-to-Assets Ratio: Definition, Calculation & Risk Assessment

- Operating Ratio: Definition, Calculation & Importance

- Reserve Ratio Explained: Understanding Bank Reserves

- Understanding the Retention Ratio: Reinvesting for Growth

- Sharpe Ratio: Calculate & Interpret Investment Performance

-

![Shareholder Equity Ratio: Definition & Calculation | [Your Company Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815180064_S.png) Shareholder Equity Ratio: Definition & Calculation | [Your Company Name]

Shareholder Equity Ratio: Definition & Calculation | [Your Company Name]The shareholder equity ratio is a ratio that shows the amount of a company’s assets that have been financed using the owner’s equity instead of debt. It shows the portion of shareholders&r...

-

Treynor Ratio: Understanding Risk-Adjusted Portfolio Performance

Treynor Ratio: Understanding Risk-Adjusted Portfolio PerformanceThe Treynor Ratio is a portfolio performance measure that adjusts for systematic riskSystematic RiskSystematic risk is that part of the total risk that is caused by factors beyond the control of a spe...