Net Interest Margin (NIM): Definition & Importance

Financial intermediaries in the economy deal extensively with borrowing and lending, and the net interest margin is the net benefit of lending.

Net interest margin is the difference between the interest income generated and the amount of interest paid out to lenders. It is an industry-specific profitability ratioProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit for banks and other financial institutions that lend out interest-earning assets.

Summary

- Net interest margin is a measure of profitability for banks and financial institutions. It refers to the difference between interest received and interest paid.

- Interest rates in the economy significantly affect the financial net interest margin.

- A positive net interest margin indicates that the bank is efficiently investing, whereas a negative net interest margin implies inefficient investing.

Net Interest Margin Formula

Interest Revenue

Interest revenue is generated through interest payments the bank receives on outstanding loans. It is made up of credit lines and loans on the financial institution’s balance sheet.

Interest Expense

Interest expense is the price the lender charges the borrower in a financing transaction. It is the cost of borrowing money. It is the interest that accumulates on outstanding liabilities. Common examples include customer deposits and wholesale financing.

Average Earning Assets

A company’s earning assets are investments that produce income without any significant effort on its owner’s part. Some popular earning assets are stocks, bondsBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period., certificates of deposits, notes, etc.

To calculate the average earning assets, simply take the average of the beginning and ending asset balance.

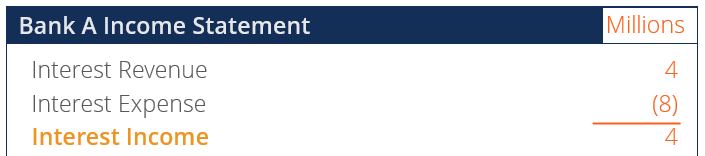

Negative Net Interest Margin Example

Over the fiscal year, Bank A collected $4 million in interest from its clients. In the same period, Bank A needed to pay $8 million in interest to a reinsurance companyReinsurance CompaniesReinsurance companies, also known as reinsurers, are companies that provide insurance to insurance companies. In other words, reinsurance companies are companies that receive insurance liabilities from insurance companies.. Bank A’s average earning assets in the fiscal year was $20 million.

A net interest margin of -20% indicates that Bank A is losing more money than it is making on its own investments. Therefore, Bank A’s capital was used inefficiently.

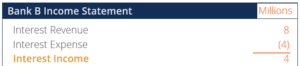

Positive Net Interest Margin Example

Over the fiscal year, Bank B collected $8 million in interest from its clients. In the same period, Bank B needed to pay $4 million in interest to a reinsurance company. Bank B’s average earning assets in the fiscal year was $20 million.

A net interest margin of 20% indicates that Bank B is earning more money from receiving interest payments than paying interest. Therefore, Bank B’s capital was used efficiently.

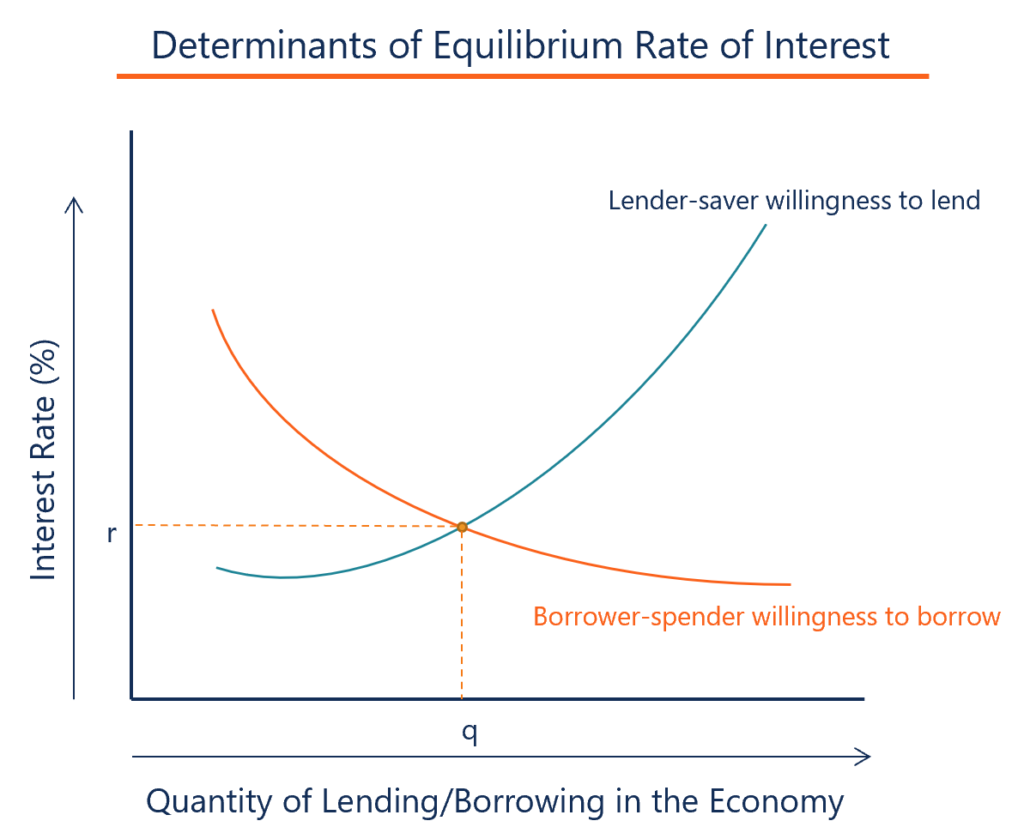

Interest Rates in the Economy and the Net Interest Margin

The net interest margin of financial intermediaries is directly related to interest rates in the economy. Interest rates in the economy move according to the economy’s business cycle. A major factor in the net interest margin is whether there is a greater demand for borrowing or saving.

Low Interest Rates

Low interest rates in the economy lead to greater net interest margins for financial intermediaries. When market interest rates fall, the funding costs of banks rapidly fall relative to their interest income, and ultimately, net interest income increases.

When interest rates fall, the demand for loans increases, and the supply of deposits decreases. It drives the volume of larger lending amounts and lower deposit volumes, therefore improving interest income. Ultimately, net interest margins will drastically increase and gradually decline over time.

High Interest Rates

High interest rates in the economy lead to smaller net interest margins for financial intermediaries. When market interest rates increase, the banks’ funding costs rapidly increase relative to their interest income and will reduce net interest income.

When interest rates rise, the demand for savings accountsSavings AccountA savings account is a typical account at a bank or a credit union that allows an individual to deposit, secure, or withdraw money when the need arises. A savings account usually pays some interest on deposits, although the rate is quite low. increases relative to loans, and the net interest margin decreases. It is because the bank will have greater interest payments than interest receivable.

Net Interest Spread vs. Net Interest Margin

Net interest spread is the nominal average between borrowing and lending rates. However, it fails to consider that earning assets and the funds borrowed may be different in terms of instrument composition and volume. Alternatively, the net interest margin is a profitability metric that contrasts a bank’s interest earnings with its payments to customers.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Financial IntermediaryFinancial IntermediaryA financial intermediary refers to an institution that acts as a middleman between two parties in order to facilitate a financial transaction. The institutions that are commonly referred to as financial intermediaries include commercial banks, investment banks, mutual funds, and pension funds.

- Expected ReturnExpected ReturnThe expected return on an investment is the expected value of the probability distribution of possible returns it can provide to investors. The return on the investment is an unknown variable that has different values associated with different probabilities.

- Interest IncomeInterest IncomeInterest income is the amount paid to an entity for lending its money or letting another entity use its funds. On a larger scale, interest income is the amount earned by an investor’s money that he places in an investment or project.

- Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money.

-

Margin Accounts: Borrowing to Invest & Increase Buying Power

A margin account refers to a type of brokerage account that investors use where they can borrow funds to purchase financial products. Investors are required to pay a monthly interest rate on the amoun

-

Margin Debt Explained: Understanding Brokerage Loans for Investing

Margin debt represents the amount that an investor owes a broker in their margin account. When a broker approves a margin account for an investor, the margin account is granted a line of credit that c

finance

- Understanding Add-On Interest: How It Works & Loan Payments

- EBITDA Margin: Definition, Calculation & Importance

- Understanding Interest: Costs & Rewards of Borrowing and Lending

- Understanding Interest Income: A Comprehensive Guide

- Understanding Interest Rates: A Comprehensive Guide

- Net Interest Income (NII): Definition & Calculation

- Net Interest Margin (NIM): Definition & Importance

- Net Profit Margin: Definition, Calculation & Importance

- Net Interest Margin (NIM): Definition & Importance

-

Understanding Maintenance Margin: A Guide for Investors

Understanding Maintenance Margin: A Guide for InvestorsMaintenance margin is the total amount of capital that must remain in an investment account in order to hold an investment or trading positionLong and Short PositionsIn investing, long and short posit...

-

Margin Trading Explained: Borrowing Money to Invest

Margin Trading Explained: Borrowing Money to InvestThe term “margin” refers to the amount deposited with a brokerage when borrowing money to buy securities. When an investor buys securities on margin, it means they are using borrowed money...