Understanding Prepaid Expenses: Definition & Accounting

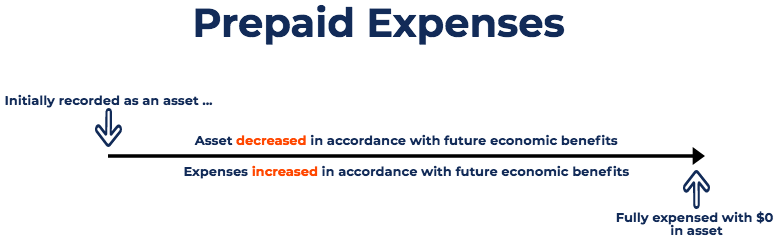

Prepaid expenses represent expendituresExpenditureAn expenditure represents a payment with either cash or credit to purchase goods or services. An expenditure is recorded at a single point in that have not yet been recorded by a company as an expense, but have been paid for in advance. In other words, prepaid expenses are expenditures paid in one accounting period, but will not be recognized until a later accounting period. Prepaid expenses are initially recorded as assets, because they have future economic benefits, and are expensed at the time when the benefits are realized (the matching principle).

Summary

- Prepaid expenses are future expenses that are paid in advance and hence recognized initially as an asset.

- As the benefits of the expenses are recognized, the related asset account is decreased and expensed.

- The most common types of prepaid expenses are prepaid rent and prepaid insurance.

Common Reasons for Prepaid Expenses

The two most common uses of prepaid expenses are rent and insurance.

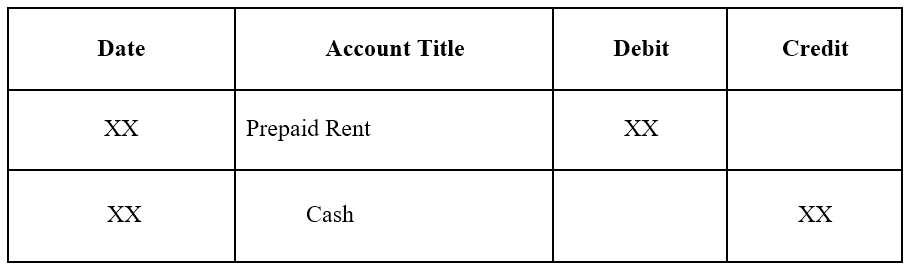

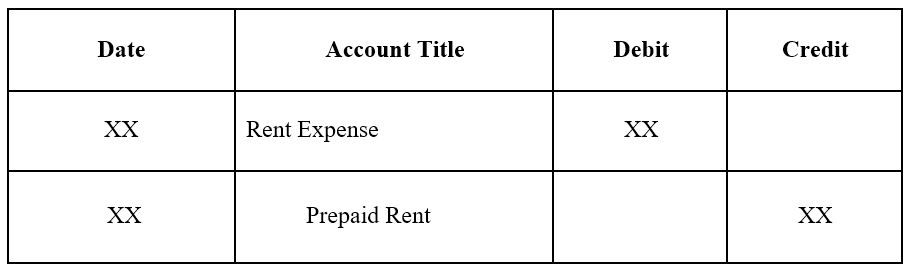

1. Prepaid rent is rent paid in advance of the rental period. The journal entries for prepaid rent are as follows:

Initial journal entry for prepaid rent:

Adjusting journal entry as the prepaid rent expires:

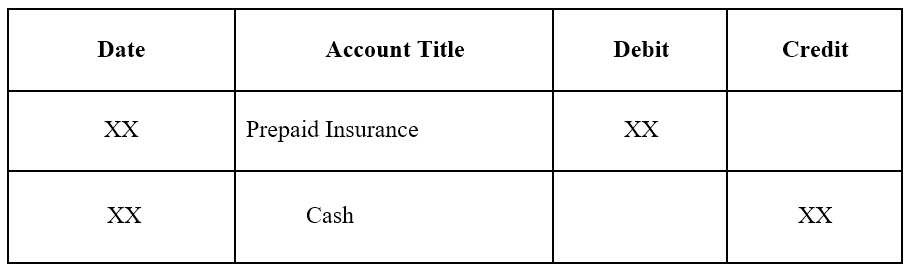

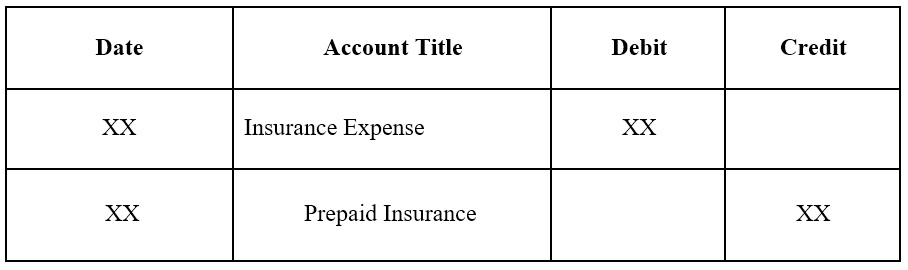

2. Prepaid insurance is insurance paid in advance and that has not yet expired on the date of the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting..

Initial journal entry for prepaid insurance:

Adjusting journal entry as the prepaid insurance expires:

Prepaid Expenses Example

We will look at two examples of prepaid expenses:

Example #1

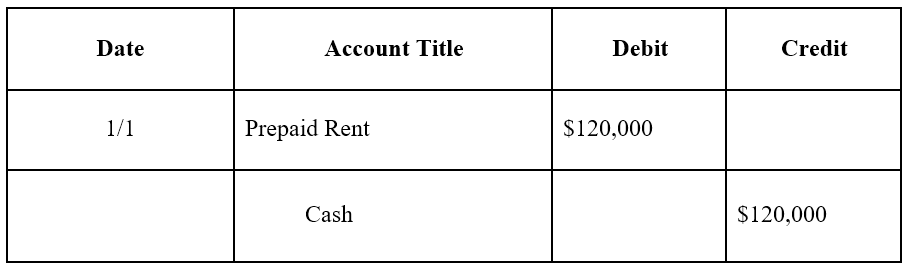

Company A signs a one-year lease on a warehouse for $10,000 a month. The landlord requires that Company A pays the annual amount ($120,000) upfront at the beginning of the year.

The initial journal entryJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits) for Company A would be as follows:

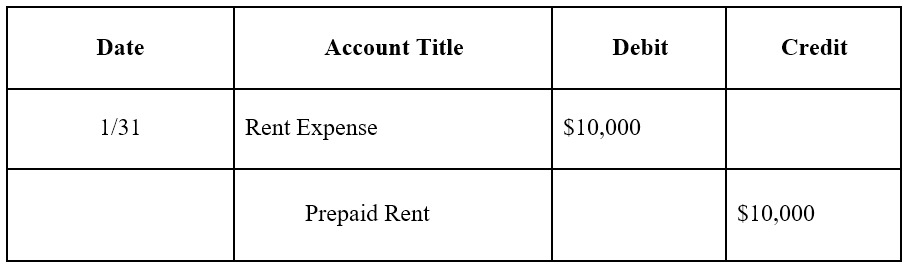

At the end of one month, Company A would’ve used up one month of its lease agreement. Therefore, prepaid rent must be adjusted:

Note: One month corresponds to $10,000 ($120,000 x 1/12) in rent.

The adjusting journal entry is done each month, and at the end of the year, when the lease agreement has no future economic benefits, the prepaid rent balance would be 0.

Example #2

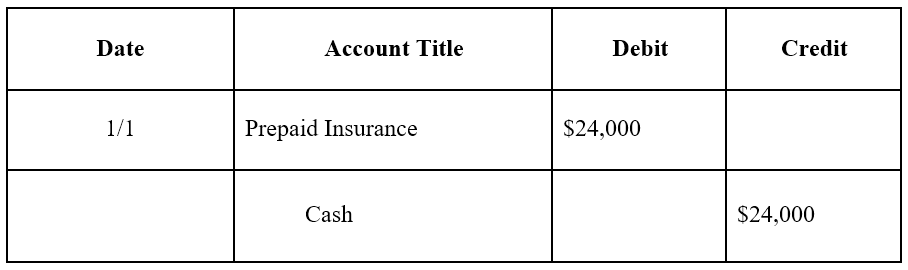

Upon signing the one-year lease agreement for the warehouse, the company also purchases insurance for the warehouse. The company pays $24,000 in cash upfront for a 12-month insurance policy for the warehouse.

The initial journal entry for Company A would be as follows:

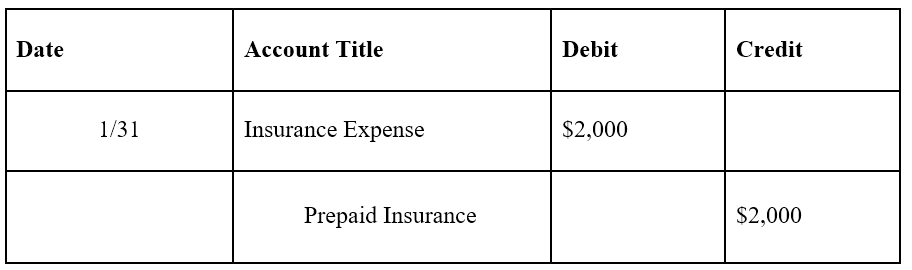

At the end of one month, Company A would have used up one month of its insurance policy. Therefore, prepaid insurance must be adjusted:

Note: One month corresponds to $2,000 ($24,000 x 1/12) in insurance policy.

The adjusting journal entry is done each month, and at the end of the year, when the insurance policy has no future economic benefits, the prepaid insurance balance would be 0.

Effect of Prepaid Expenses on Financial Statements

The initial journal entry for a prepaid expense does not affect a company’s financial statements. For example, refer to the first example of prepaid rent. The initial journal entry for prepaid rent is a debit to prepaid rent and a credit to cash.

These are both asset accounts and do not increase or decrease a company’s balance sheet. Recall that prepaid expenses are considered an asset because they provide future economic benefits to the company.

The adjusting journal entry for a prepaid expense, however, does affect both a company’s income statement and balance sheet. Refer to the first example of prepaid rent. The adjusting entry on January 31 would result in an expense of $10,000 (rent expense) and a decrease in assets of $10,000 (prepaid rent).

The expense would show up on the income statement while the decrease in prepaid rent of $10,000 would reduce the assets on the balance sheet by $10,000.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Cost Behavior AnalysisCost Behavior AnalysisCost behavior analysis refers to management’s attempt to understand how operating costs change in relation to a change in an organization’s

- Cost StructureCost StructureCost structure refers to the types of expenses that a business incurs, and is typically composed of fixed and variable costs. Fixed costs remain unchanged

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

-

Understanding Financial Statements: A Comprehensive Guide

Financial statements are the records of a company’s financial condition and activities during a period of time. Financial statements show the financial performance and strength of a companyCorpo

-

Headline Earnings: Understanding Core Business Performance

Headline earnings are a restatement of a company’s profit that removes the effect of one-time charges, write-downs, cost-cutting, and other extraordinary items like tax liabilities. Another way

Accounting

- Impact of Unadjusted Prepaid Expenses on Financial Statements

- Understanding Operating Expenses (OpEx): A Comprehensive Guide

- Understanding Business Erosion: Causes, Risks & Prevention

- Understanding Non-Cash Expenses: A Comprehensive Guide

- Understanding Accounts Expenses: A Comprehensive Guide

- Understanding Accrued Expenses: A Comprehensive Guide

- Understanding Administrative Expenses: A Comprehensive Guide

- Understanding Maintenance Expenses: A Comprehensive Guide

- Understanding Operating Expenses (OPEX): A Comprehensive Guide

-

Understanding Business Expenses: A Comprehensive Guide

Understanding Business Expenses: A Comprehensive GuideBusinesses incur various types of expenses. An expense is a type of expenditure that flows through the income statementIncome StatementThe Income Statement is one of a companys core financial statemen...

-

Understanding Financial Assets: Definitions & Types

Understanding Financial Assets: Definitions & TypesFinancial assets refer to assets that arise from contractual agreements on future cash flowsCash Flow StatementA cash flow Statement contains information on how much cash a company generated an...