Restricted Cash: Definition, Types & Impact on Financial Statements

Restricted cash refers to cash that is held onto by a company for specific reasons and is, therefore, not available for immediate ordinary business use. It can be contrasted with unrestricted cash, which refers to cash that can be used for any purpose.

Quick Summary:

- Restricted cash refers to cash that is held by a company for specific reasons and not available for immediate business use.

- Restricted cash is commonly found on the balance sheet with a description of why the cash is restricted in the accompanying notes to the financial statements.

- Reasons for cash being restricted include bank loan requirements, payment deposits, and collateral pledges.

Restricted Cash on the Balance Sheet

Restricted cash can be commonly found on the balance sheet as a separate line item. For example, the balance sheet may look as follows:

The reason for any restriction is generally revealed in the accompanying notes to the financial statements. Additionally, depending on how long the cash is restricted for, the line item may appear under current assetsCurrent AssetsCurrent assets are all assets that a company expects to convert to cash within one year. They are commonly used to measure the liquidity of a or non-current assets. Cash that is restricted for one year or less is categorized under current assets, while cash restricted for more than a year is categorized as a non-current asset.

Reasons for Restrictions

There are several reasons why cash can be restricted:

1. Bank loan requirements

When a company receives a bank loan, the bank may require that the company reserves (or maintains) a certain amount of cash that will be unavailable for spending.

2. Payment deposits

A company may receive cash from a customer prior to providing services or shipping goods. The customer may require, through a clause in the agreement, that the company cannot spend the cash until the service or order is fulfilled.

3. Collateral pledge

A company may be required by an insurance company to pledge a certain amount of cash as collateral against risk.

4. Paying off debt

A company may set aside a certain amount of cash each quarter to make a payment on long-term debt.

Financial Ratios

Due to the cash not being readily available for use, cash that is restricted is generally excluded in several liquidity ratios. Failure to exclude the cash in the calculation of liquidity ratios will make the company look more liquid than it is and, thereby, be misleading. Examples of liquidity ratios that exclude restricted cash include the cash ratioCash RatioThe cash ratio, sometimes referred to as the cash asset ratio, is a liquidity metric that indicates a company’s capacity to pay off short-term debt obligations with its cash and cash equivalents. Compared to other liquidity ratios such as the current ratio and quick ratio, the cash ratio is a stricter, more conservative measure and the quick ratioQuick RatioThe Quick Ratio, also known as the Acid-test, measures the ability of a business to pay its short-term liabilities with assets readily convertible into cash.

Example

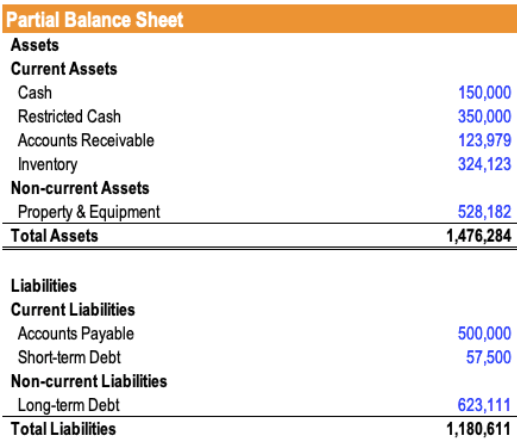

John, a junior analyst, has been instructed by the head of equity research to conduct liquidity analysis of a company. More specifically, he has been asked to determine the current ratio of a company to see if it has enough cash to pay off its short-term obligations. Recall that the quick ratio is calculated as (Cash and Cash Equivalents + Marketable Securities) / Current Liabilities.

The company’s balance sheet is provided as follows:

Under accompanying notes to the financial statementsAudited Financial StatementsPublic companies are obligated by law to ensure that their financial statements are audited by a registered CPA. The purpose of the, John notes that the restricted cash is in relation to a payment deposit where the company agreed with a customer to keep $350,000 in cash until its obligation with the customer is settled. The obligation is expected to settle within a year.

John excludes that cash from his calculations and determines the company’s quick ratio to be $150,000 / ($500,000 + $57,500) = 0.27.

Had John used the restricted cash in his calculation of the quick ratio, he would have gotten a quick ratio of ($150,000 + $350,000) / ($500,000 + $57,000) = 0.90 and mistakenly deemed the company much more liquid than it is.

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Idle CashIdle CashIdle cash is, as the phrase implies, cash that is idle or is not being used in a way that can increase the value of a business. It means that the cash is not earning interest from sitting in savings or a checking account, and is not generating a profit in the form of asset purchases or investments. The cash is simply sitting in a form where it does not appreciate.

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Sinking FundSinking FundA sinking fund is a type of fund that is created and set up purposely for repaying debt. The owner of the account sets aside a certain amount of money regularly and uses it only for a specific purpose. Often, it is used by corporations for bonds and deposits money to buy back issued bonds

- Statement of Cash FlowsStatement of Cash FlowsThe Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements that report the cash

-

Restricted Stock: Definition, Types & How It Works

Restricted stock refers to an award of stock to a person that is subject to conditions that must be met before the stockholderStockholders EquityStockholders Equity (also known as Shareholders Equity)

-

Understanding Stocks: A Beginner's Guide to Share Ownership

When a person owns stock in a company, the individual is called a shareholder and is eligible to claim part of the company’s residual assets and earnings (should the company ever have to dissolv

finance

- Acquirer Definition: Understanding Corporate Acquisitions

- Understanding Cash Consideration in Mergers & Acquisitions

- Understanding Cash Flow: A Comprehensive Guide

- Cash Management: A Comprehensive Guide to Financial Stability

- Cash-on-Cash Return: Definition, Calculation & Importance

- Cash Reserves: Definition, Benefits & Short-Term Needs

- Understanding Financial Ratios: A Comprehensive Guide

- Net Cash: Definition, Calculation & Importance for Businesses

- Accounts Receivable (AR): Definition, Management & Forecasting

-

Parent Company Explained: Definition, Control & Examples

Parent Company Explained: Definition, Control & ExamplesA parent company is a company that owns more than 50% of the outstanding voting shares of another company. Therefore, it controls the other company or companies and can directly influence the business...

-

Profit vs. Cash Flow: Understanding the Key Difference

Profit vs. Cash Flow: Understanding the Key DifferenceUnderstanding the difference between profit vs cash is very important in the finance industry. Profit is defined as revenue less all the expenses of a company in a certain period, while cash flow is c...