Modified Dietz Return: Calculation & Investment Portfolio Analysis

The Modified Dietz Return is an algebraic method used to calculate the rate of returnRate of ReturnThe Rate of Return (ROR) is the gain or loss of an investment over a period of time copmared to the initial cost of the investment expressed as a percentage. This guide teaches the most common formulas of an investment portfolio based on the cash flows of the portfolio. The method also accounts for the timing of when the cash flows come in and out of the portfolio.

Unlike the Modified Internal Rate of Return and the Internal Rate of Return (IRR)Internal Rate of Return (IRR)The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment., the Modified Dietz Return is not an expected return and is backward-looking, doesn’t use expected value, and calculates the realized return of the portfolio.

Why was the Modified Dietz Return Created?

The Modified Dietz formula was created to better understand and provide more transparency for the return an investment portfolio made. Investment portfolios constantly see cash flows coming in and going out, making it easy to lose track of how much money the portfolio made. Thus, the Modified Dietz Return formula was made to keep track of the timing and magnitude of the cash flows throughout the entire investment horizon.

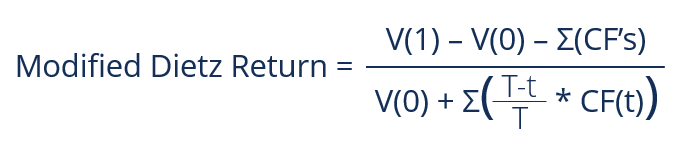

Formula for the Modified Dietz Return

Where:

- V(0) = Value of portfolio at start date

- V(1) = Value of portfolio at end date

- CF’s = Cash flows throughout the investment horizon

- T = Length of the investment horizon

- t = Time of cash flow

- CF(t) = Cash flow at certain time

One of the main components of the formula is its ability to account for the timing of cash flows. The formula accounts for such a fact by taking the sum of the weighted cash flows, weighted by when they occurred throughout the investment horizon.

It is achieved by taking the difference of the length of the investment horizon (T) and the timing of the cash flow (t) and dividing the difference by the investment horizon (T), then by multiplying the result by the magnitude of the cash flow that happened at t; the product will be the weighted cash flow.

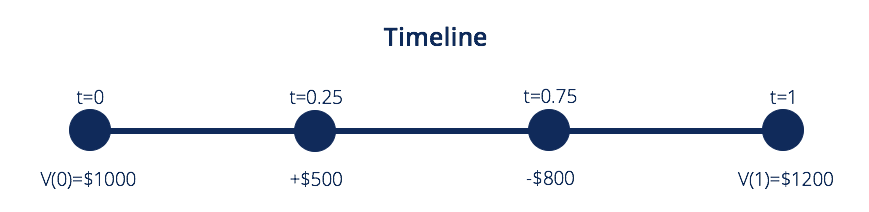

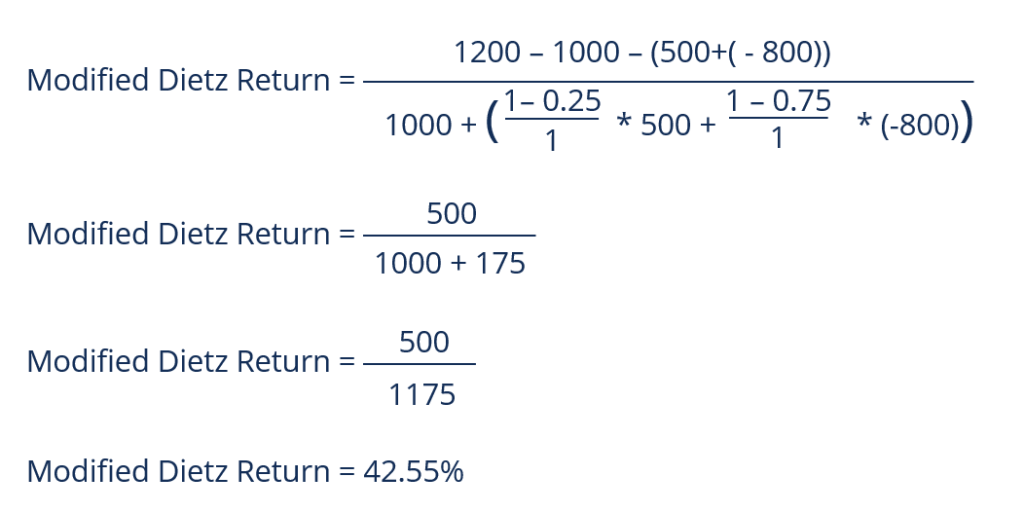

Practical Example

An individual invests $1,000 in an investment portfolio for one year. At the end of the year, the portfolio rose in value to $1,200. During the investment horizon, at the end of the first three months, the investor deposited $500 into the portfolio.

However, at the end of the nine-month period, the investor withdrew $800. To understand the portfolio’s performance, the investor must calculate the rate of return that accounts for the timing of the withdrawals and deposits made.

Thus:

- V(0) = 1000

- V(1) = 1200

- CF25 = 500

- CF75 = -800

- T = 1 year

Disadvantages of the Modified Dietz Return

The Modified Dietz Return formula exhibits disadvantages when one or more large cash flows occur during the investment period or when the investment is very volatile, and experiences returns that are significantly non-linear. Another disadvantage is that the investor needs to know the value of the investment both at the beginning and end of the investment horizon.

Additionally, the investor must adopt a way to keep track of the cash flows coming in and out of the portfolio. It is important to know when to use the Modified Dietz Return to get an accurate understanding of how the investment portfolio performed.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money.

- Modified Internal Rate of Return (MIRR)Modified Internal Rate of Return (MIRR)The modified internal rate of return (commonly denoted as MIRR) is a financial measure that helps to determine the attractiveness of an investment and that can be used to compare different investments. Essentially, the modified internal rate of return is a modification of the internal rate of return (IRR) formula

- Portfolio ManagerPortfolio ManagerPortfolio managers manage investment portfolios using a six-step portfolio management process. Learn exactly what does a portfolio manager do in this guide. Portfolio managers are professionals who manage investment portfolios, with the goal of achieving their clients’ investment objectives.

- Return on Investment (ROI)Return on Investment (ROI)Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments.

-

Why Investing Matters: Building Wealth & Financial Security

Your financial goals should determine the content of your financial portfolio. Many Americans lack an understanding of financial markets and how to begin an investment program. More important

-

Decoding Finance: A Simple Guide to Investment Terms

So many financial terms are often thrown around and used in every-day conversation, but do you really know what they mean? Our What the Finance series simplifies financial terms so you fe

invest

- MIRR: Understanding the Modified Internal Rate of Return

- Understanding Return on Investment (ROI): A Comprehensive Guide

- Understanding Portfolio Active Return: Definition & Calculation

- Annual Return: Definition, Calculation & Understanding

- Holding Period Return (HPR): Definition & Calculation

- K-Ratio Explained: Measuring Investment Growth & Consistency

- Understanding the Modified Dietz Method (MDM) for Portfolio Returns

- Nominal Rate of Return: Definition & Calculation

- Understanding Return on Investment (ROI): A Comprehensive Guide

-

Korea Investment Corporation (KIC): A Comprehensive Overview

Korea Investment Corporation (KIC): A Comprehensive OverviewThe Korea Investment Corporation (KIC) is a sovereign wealth fundTop 5 Sovereign Wealth FundsSovereign Wealth Funds (SWF) are pools of income – generally derived from staple commodities – ...

-

Dogs of the Dow: A Simple & Potentially Profitable Investment Strategy

Dogs of the Dow: A Simple & Potentially Profitable Investment StrategyThe Dogs of the Dow investment strategy is one that was created by Michael Higgins and was first illustrated in his book called Beating the Dow. This investment strategy is one of the simplest s...