Understanding Modified Duration: A Key Bond Valuation Metric

Modified duration, a formula commonly used in bond valuations, expresses the change in the value of a security due to a change in interest ratesFloating Interest RateA floating interest rate refers to a variable interest rate that changes over the duration of the debt obligation. It is the opposite of a fixed rate.. In other words, it illustrates the effect of a 100-basis point (1%) change in interest rates on the price of a bond.

Modified duration illustrates the concept that bond prices and interest rates move in opposite directions – higher interest rates lower bond prices, and lower interest rates raise bond prices.

Formula for Modified Duration

The formula for modified duration is as follows:

Where:

- Macaulay Duration is the weighted average number of years an investor must maintain his or her position in the bond where the present value (PV) of the bond’s cash flow equals the amount paid for the bond. In other words, it is the time it would take for an investor to retrieve the money initially invested in the bond

- YTM stands for Yield to MaturityYield to Maturity (YTM)Yield to Maturity (YTM) – otherwise referred to as redemption or book yield – is the speculative rate of return or interest rate of a fixed-rate security. and is the total return on a bond if held until maturity

- n is the number of coupon periods per year.

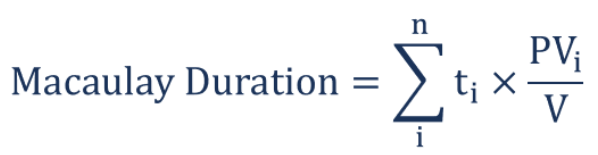

Understanding the Macaulay Duration

In order to arrive at the modified duration of a bond, it is important to understand the numerator component – the Macaulay duration – in the modified duration formula.

The Macaulay duration is the weighted average of time until the cash flows of a bond are received. In layman’s term, the Macaulay duration measures, in years, the amount of time required for an investor to be repaid his initial investment in a bond. A bond with a higher Macaulay duration will be more sensitive to changes in interest rates.

The formula for Macaulay duration is as follows:

Where:

- ti is the time period

- PVi is the present value of the time-weighted cash flow

- V is the present value of all cash flow.

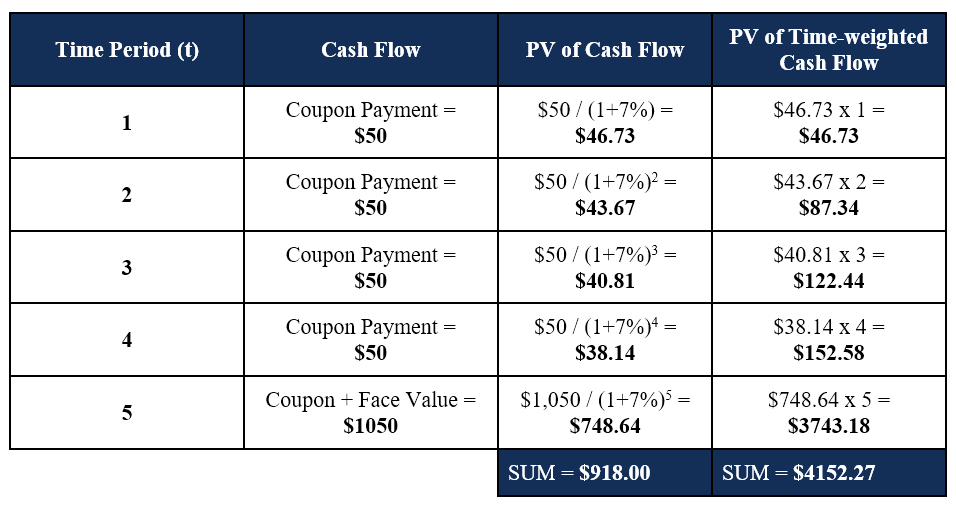

Below is an example of calculating Macaulay duration on a bond.

Example of Macaulay Duration

Tim holds a 5-year bond with a face value of $1,000 and an annual coupon rateCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond. of 5%. The current rate of interest is 7%, and Tim would like to determine the Macaulay duration of the bond. The calculation is given below:

The Macaulay duration for the 5-year bond is calculated as $4152.27 / $918.00 = 4.52 years.

Putting it Together

Now that we understand and know how to calculate the Macaulay duration, we can determine the modified duration.

Using the example above, we simply insert the figures into the formula to determine the modified duration:

The modified duration is 4.22.

Interpreting the Modified Duration

How do we interpret the result above? Recall that modified duration illustrates the effect of a 100-basis point (1%) change in interest rates on the price of a bond.

Therefore,

- If interest rates increase by 1%, the price of the 5-year bond will decrease by 4.22%.

- If interest rates decrease by 1%, the price of the 5-year bond will increase by 4.22%.

The modified duration provides a good measurement of a bond’s sensitivity to changes in interest rates. The higher the Macaulay duration of a bond, the higher the resulting modified duration and volatility to interest rate changes.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- Effective DurationEffective DurationEffective duration is the sensitivity of a bond's price against the benchmark yield curve. One way to assess the risk of a bond is to estimate the

- DURATION Function in ExcelDURATION FunctionThe DURATION function is categorized under Excel Financial functions. It helps to calculate the Macauley Duration. The function calculates the duration of a security that pays interest on a periodic basis with a par value of $100.

- Equity vs Fixed IncomeEquity vs Fixed IncomeEquity vs Fixed Income. Equity and fixed income products are financial instruments that have very important differences every financial analyst should know. Equity investments generally consist of stocks or stock funds, while fixed income securities generally consist of corporate or government bonds.

-

Asset Swap Explained: Definition, OTC Trading & Key Concepts

An asset swap is a derivative contract between two parties that swap fixed and floating assets. The transactions are done over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of

-

Understanding Bond Pricing: Key Factors & Valuation

Bond pricing is an empirical matter in the field of financial instrumentsPublic SecuritiesPublic securities, or marketable securities, are investments that are openly or easily traded in a market. The

invest

- Understanding Bond Duration: A Key Fixed Income Metric

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Dollar Duration: A Guide for Bond Investors

- Understanding Duration Drift in Asset-Liability Management

- Effective Duration Explained: Bond Price Sensitivity

- Understanding Key Rate Duration: A Guide for Bond Investors

- Macaulay Duration: Understanding Bond Interest Rate Risk

- Understanding Noncallable Securities: A Comprehensive Guide

-

Amortized Bonds: Understanding Principal Repayment

Amortized Bonds: Understanding Principal RepaymentAn amortized bond is a bond with the principal amount – otherwise known as face value –regularly paid down over the life of the bond. The bond’s principal is divided up according to ...

-

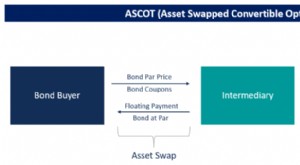

ASCOT Options: Understanding Asset-Swapped Convertible Options

ASCOT Options: Understanding Asset-Swapped Convertible OptionsThe term ASCOT is short for Asset Swapped Convertible Option Transaction. It is an American style call option to buy back a convertible bond. It falls under the category of financial products called s...