Understanding Option Greeks: A Comprehensive Guide

Option Greeks are financial measures of the sensitivity of an option’s price to its underlying determining parameters, such as volatility or the price of the underlying asset. The Greeks are utilized in the analysis of an options portfolio and in sensitivity analysisWhat is Sensitivity Analysis?Sensitivity Analysis is a tool used in financial modeling to analyze how the different values for a set of independent variables affect a dependent variable of an option or portfolio of optionsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.. The measures are considered essential by many investors for making informed decisions in options trading.

Delta, Gamma, Vega, Theta, and Rho are the key option Greeks. However, there are many other option Greeks that can be derived from those mentioned above.

Name Dependent Variable Independent Variable DeltaOption priceValue of underlying assetGammaDeltaValue of underlying assetVegaOption priceVolatilityThetaOption priceTime to maturityRhoOption priceInterest rate

Option Greek Delta

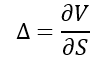

Delta (Δ) is a measure of the sensitivity of an option’s price changes relative to the changes in the underlying asset’s price. In other words, if the price of the underlying assetTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and increases by $1, the price of the option will change by Δ amount. Mathematically, the delta is found by:

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- S – the underlying asset’s price

Keep in mind that we take the first derivativeFutures and ForwardsFuture and forward contracts (more commonly referred to as futures and forwards) are contracts that are used by businesses and investors to hedge against risks or speculate. of the option and underlying asset prices because the derivative is a measure of the rate change of the variable at a given period.

The delta is usually calculated as a decimal number from -1 to 1. Call optionsCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. can have a delta from 0 to 1, while puts have a delta from -1 to 0. The closer the option’s delta to 1 or -1, the deeper in-the-money is the option.

The delta of an option’s portfolio is the weighted average of the deltas of all options in the portfolio.

Delta is also known as a hedge ratio. If a trader knows the delta of the option, he can hedge his position by buying or shorting the number of underlying assets multiplied by delta.

Learn more with Corporate Finance Institute Courses

Gamma

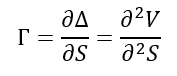

Gamma (Γ) is a measure of the delta’s change relative to the changes in the price of the underlying asset. If the price of the underlying asset increases by $1, the option’s delta will change by the gamma amount. The main application of gamma is the assessment of the option’s delta.

Long options have a positive gamma. An option has a maximum gamma when it is at-the-money (option strike price equals the price of the underlying asset). However, gamma decreases when an option is deep-in-the-money or out-the-money.

Option Greek Vega

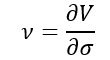

Vega (ν) is an option Greek that measures the sensitivity of an option price relative to the volatility of the underlying asset. If the volatility of the underlying asses increases by 1%, the option price will change by the vega amount.

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- σ – the volatility of the underlying asset

The vega is expressed as a money amount rather than as a decimal number. An increase in vega generally corresponds to an increase in the option value (both calls and puts).

Theta

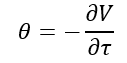

Theta (θ) is a measure of the sensitivity of the option price relative to the option’s time to maturity. If the option’s time to maturity decreases by one day, the option’s price will change by the theta amount. The Theta option Greek is also referred to as time decay.

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- τ – the option’s time to maturity

In most cases, theta is negative for options. However, it may be positive for some European options. Theta shows the most negative amount when the option is at-the-money.

Learn more with Corporate Finance Institute Courses

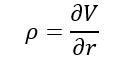

Rho

Rho (ρ) measures the sensitivity of the option price relative to interest rates. If a benchmark interest rate increases by 1%, the option price will change by the rho amount. The rho is considered the least significant among other option Greeks because option prices are generally less sensitive to interest rate changes than to changes in other parameters.

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- r – interest rate

Generally, call options have a positive rho, while the rho for put options is negative.

Related Readings

Thank you for reading CFI’s explanation of Option Greeks. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following resources:

- Guide to BetaBetaThe beta (β) of an investment security (i.e. a stock) is a measurement of its volatility of returns relative to the entire market. It is used as a measure of risk and is an integral part of the Capital Asset Pricing Model (CAPM). A company with a higher beta has greater risk and also greater expected returns.

- Leverage RatiosLeverage RatiosA leverage ratio indicates the level of debt incurred by a business entity against several other accounts in its balance sheet, income statement, or cash flow statement. Excel template

- Trading MechanismsTrading MechanismsTrading mechanisms refer to the different methods by which assets are traded. The two main types of trading mechanisms are quote driven and order driven trading mechanisms

- Variance AnalysisVariance AnalysisVariance analysis can be summarized as an analysis of the difference between planned and actual numbers. The sum of all variances gives a

-

LEAPS Explained: Understanding Long-Term Equity Options

LEAPS (Long-Term Equity Anticipation Security) are options for terms that are longer than those of the most common options on equities and indices. Around 2,500 equities and 20 indices make LEAPS avai

-

Understanding Momentum Indicators in Trading

Momentum indicators are tools utilized by traders to get a better understanding of the speed or rate at which the price of a securityPublic SecuritiesPublic securities, or marketable securities, are i

invest

- Call Options: A Comprehensive Guide for Investors

- Understanding Delta: A Key Risk Measure in Derivatives

- Understanding Digital Options: A Comprehensive Guide for Traders

- Understanding Exercise Price in Options Trading

- Knock-In Options Explained: A Comprehensive Guide

- Knock-Out Options: A Comprehensive Guide

- Naked Options: Risks, Rewards, and How They Work

- Understanding Near-The-Money Options: A Comprehensive Guide

- Put Options Explained: A Comprehensive Guide for Investors

-

Donchian Channels: A Comprehensive Guide for Traders

Donchian Channels: A Comprehensive Guide for TradersDonchian Channels are a channel-based technical analysisTechnical Analysis - A Beginners GuideTechnical analysis is a form of investment valuation that analyses past prices to predict future price act...

-

Understanding Equity Derivatives: A Comprehensive Guide

Understanding Equity Derivatives: A Comprehensive GuideEquity derivatives are financial products/instruments whose value is derived from the increase or decrease in the underlying assets, i.e., equity stocks or shares in the secondary marketSecondary Mark...