Vega (Option Greeks): Understanding Option Price Sensitivity

Vega falls under the series of sensitivity measures called the GreeksOption GreeksOption Greeks are financial measures of the sensitivity of an option’s price to its underlying determining parameters, such as volatility or the price of the underlying asset. The Greeks are utilized in the analysis of an options portfolio and in sensitivity analysis of an option. Vega is not a Greek letter; however, it is denoted by the Greek letter nu (ν). The Greeks are measures used to assess derivativesDerivativesDerivatives are financial contracts whose value is linked to the value of an underlying asset. They are complex financial instruments that are and are often referred to as risk measures, hedge parameters, or risk sensitivities. Vega measures an option’s sensitivity to the underlying asset’sAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations. volatilityVolatilityVolatility is a measure of the rate of fluctuations in the price of a security over time. It indicates the level of risk associated with the price changes of a security. Investors and traders calculate the volatility of a security to assess past variations in the prices. It is very important in optionOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price. pricing and is expressed as the change in the value of the option as volatility changes by a 1% increment.

Quick Summary of Points

- Vega measures the sensitivity of the option price to a 1% change in the implied volatility

- Implied volatility refers to the expected volatility of the underlying asset

- Higher volatility generally means a higher extrinsic value priced into the premium of an option

- Vega can be used to assess the potential of an option to increase in value before the expiration date

What is Implied Volatility?

Vega can be thought of as the change in the value of a derivativeDerivativesDerivatives are financial contracts whose value is linked to the value of an underlying asset. They are complex financial instruments that are, to a 1% change in the implied volatility of the underlying asset. To understand what this means, we must first understand what implied volatility is, and how it is measured.

Implied volatility refers to the expected volatilityVolatilityVolatility is a measure of the rate of fluctuations in the price of a security over time. It indicates the level of risk associated with the price changes of a security. Investors and traders calculate the volatility of a security to assess past variations in the prices of the underlying asset. Implied volatility can be shortened to IV or just volatility. A higher IV means there is more uncertainty around the price of the stock. As IV increases, you would expect to see larger swings in the price.

IV is expressed as a percentage change associated with one standard deviationStandard DeviationFrom a statistics standpoint, the standard deviation of a data set is a measure of the magnitude of deviations between values of the observations contained, annualized. An implied volatility of 20% would mean that the standard deviation over the next year would be a 20% change in price. In a normal distributionNormal DistributionThe normal distribution is also referred to as Gaussian or Gauss distribution. This type of distribution is widely used in natural and social sciences. The, it would be a 68.2% probability of a 20% change in price. If the price of the underlying asset is $100, then you would expect the stock to be between $80 and $120 in the next year.

How to Interpret Vega?

Vega is generally positive for both call optionsCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. and put optionsPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option. that have time until the expiration date. Vega measures the sensitivity of the option price to a 1% change in the implied volatility. The units of vega are $/σ; however, like the other Greeks, the units are often left out. An option with a vega of 0.10 would mean that for every 1% change in the IV, the option price should change by $0.10.

There are three main things that affect vega. It is affected by the time until expiration, the strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on relative to the underlying asset’s spot priceSpot PriceThe spot price is the current market price of a security, currency, or commodity available to be bought/sold for immediate settlement. In other words, it is the price at which the sellers and buyers value an asset right now., and the implied volatility. The longer time there is until the expiration of an option, the higher the extrinsic value of the premium. The reason the extrinsic value is the ability to hold the option and the opportunity for the option to gain value as the underlying asset moves in price.

Higher volatilityVolatilityVolatility is a measure of the rate of fluctuations in the price of a security over time. It indicates the level of risk associated with the price changes of a security. Investors and traders calculate the volatility of a security to assess past variations in the prices generally means a higher extrinsic value priced into the premium of an option. The reason for this is that the time value is heavily influenced by the implied volatility. A higher IV means a greater chance for the underlying assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations. to move in price and the option to increase in value before the expiration date.

The option strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on relative to the asset spot priceSpot PriceThe spot price is the current market price of a security, currency, or commodity available to be bought/sold for immediate settlement. In other words, it is the price at which the sellers and buyers value an asset right now. is important too. If an option is very out of the money, the vega tends to be smaller. It is because even if volatility changes, there is still not a very high chance that the option will end up in the money, meaning the price will not show a significant difference.

Let us look at a hypothetical call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. with a premium of $5 and an underlying asset with a price of $100. If the IV is 20% and the vega of the option is 0.10, what would happen to the option price if the IV rose to 22%? The 2% increase should mean that the change in price would be an increase of 2 x 0.10 = $0.20. You would expect the price to increase from $5.00 to $5.20. If the IV instead fell by 2%, you would expect a decrease in the price of $0.20, resulting in a price of $4.80.

What is Vega Used For In Options

Vega can be used in determining the time value of an optionOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.. The extrinsic value is very important in understanding option pricing and can be used to assess the potential of an option to increase in value before the expiration date. An option’s vega will generally not be a static number. As an option’s implied volatility rises or falls, and it moves closer to expiration, the vega changes and traders often monitor vega to assess how an options price might move.

Traders often refer to being longLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). or shortLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). vega. Being long vega means that they are holding a long position and will benefit from a rise in implied volatility. Being short vega means the trader holds a short position and will benefit if the implied volatility falls.

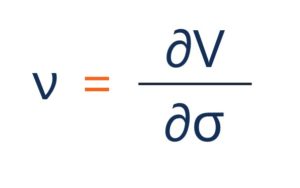

How is Vega Calculated?

The general form of vega can be represented by:

Where:

- ∂ – the first derivative

- V – the option’s price (theoretical value)

- σ – the volatility of the underlying asset

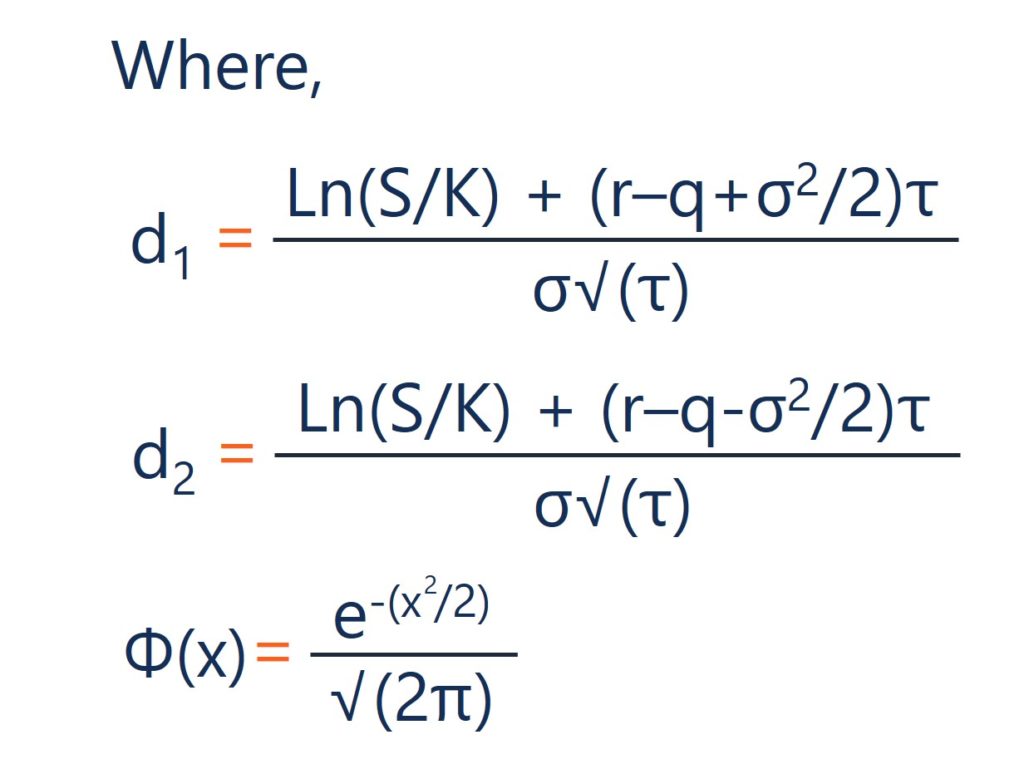

Under the Black-Scholes model, the calculation for vega is given by:

Where:

- S – the stock price

- K – the strike price

- r – the risk-free rate

- q – the annual dividend yield

- τ – time until expiration

- σ – the volatility

Additional Resources

Thank you for reading CFI’s article on vega. If you would like to learn about related concepts, check out CFI’s other resources:

- Option GreeksOption GreeksOption Greeks are financial measures of the sensitivity of an option’s price to its underlying determining parameters, such as volatility or the price of the underlying asset. The Greeks are utilized in the analysis of an options portfolio and in sensitivity analysis of an option

- DeltaDelta (Δ)Delta is a risk sensitivity measure used in assessing derivatives. It is one of the many measures that are denoted by a Greek letter. The series of risk

- ThetaTheta (Θ)Theta is a sensitivity measurement used in assessing derivatives. It is one of the measures denoted by a Greek letter. The series of risk and sensitivity

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

-

Understanding At-The-Money (ATM) Options: A Comprehensive Guide

At the money (ATM) describes a situation when the strike price of an option is equal to the underlying asset’s current market price. It is a concept of moneyness, which describes the position be

-

Understanding Option Intrinsic Value: A Clear Explanation

Intrinsic value for call options is literally the difference between the price of the market and the strike price (or exercise price), as long as the market is above the strike price. The intrin

invest

- Call Options: A Comprehensive Guide for Investors

- Understanding Delta: A Key Risk Measure in Derivatives

- Understanding Digital Options: A Comprehensive Guide for Traders

- Understanding Exercise Price in Options Trading

- Knock-In Options Explained: A Comprehensive Guide

- Knock-Out Options: A Comprehensive Guide

- Naked Options: Risks, Rewards, and How They Work

- Understanding Near-The-Money Options: A Comprehensive Guide

- Put Options Explained: A Comprehensive Guide for Investors

-

Understanding Put-Call Parity: A Comprehensive Guide

Put-call parity is an important concept in options Options: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certa...

-

Understanding Strike Price: Options Trading Explained

Understanding Strike Price: Options Trading ExplainedThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on whether they hold a call optionCall OptionA call option, com...