Accounts Receivable Aging Report: Understanding & Analysis

An accounts receivable aging report or receivable aging report refers to a summary of all receivables due from customers at any given point in time. The report breaks down receivables due from all customers into different aging categories based on the number of days since the respective invoices were raised.

A company should be worried if the accounts receivable aging report identifies that many accounts are outstanding for long periods of time. It can be considered a sign that the company is incurring excessive risk by extending credit termsCredit Conditions Credit conditions represent the terms used by lenders, such as banks, during the due diligence process for lending capital to potential borrowers. In other to customers that are unlikely to pay. Alternatively, it may also indicate that the business is inefficient at collecting payments.

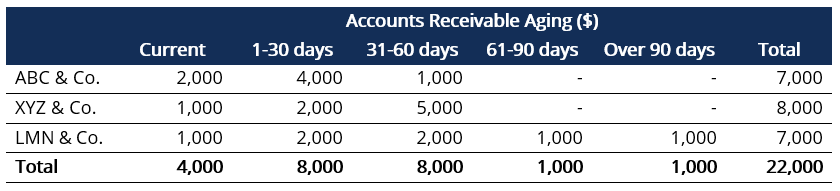

In the example above, if we assume that the company’s credit policy is 60 days, then customers ABC & Co. and XYZ & Co. appear to be within the company’s credit period for all customers. However, LMN & Co. appears to delay its payments to the company.

Summary

- The accounts receivable aging report is a great tool to identify working capital issues.

- The report can be used to help set credit policies and monitor customer credit quality.

- Avoid looking at the report in isolation; instead, look at trends.

How to Use an Accounts Receivable Aging Report?

One must start by looking at the largest balances and understand if the amounts are within the specified credit period or if they have been outstanding for a longer time. The user can also consider using the Pareto Principle, or the 80/20 Principle, which states that about 80% of the effects come from 20% of the causes, i.e., 80% of the amounts overdue may be attributed to 20% of the customers.

Uses of the Accounts Receivable Aging Report

For Management

The accounts receivable aging report can be used by management in different ways, including the following:

- Understanding the speed of collection of receivables from customers

- Understanding the financial health of customers

- Estimating allowance for doubtful accountsAllowance for Doubtful AccountsThe allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable. The amount represents the value of accounts receivable that a company does not expect to receive payment for.

The report also serves as a basis for management to adjust the credit period for customers and incentivize customers to clear their outstanding dues by giving cash discounts for early payments.

For External Stakeholders

The accounts receivable aging report can be used by various external stakeholders. For example:

- Lenders of the company can use the report to assess the company’s short-term solvency and working capitalWorking Capital CycleThe Working Capital Cycle for a business is the length of time it takes to convert the total net working capital (current assets less current requirements.

- Investors (equity and preferred) can use the report to evaluate both the short-term and long-term solvency and quality of the company’s customers.

- In some cases, even tax authorities use the receivables aging report to learn more about the sales cycle and repayment timeline of the company’s customers. They also check whether the policy for calculating the allowance for doubtful accounts is in line with the credit policy.

Allowance for Doubtful Accounts

The accounts receivable aging report is useful in determining the allowance for doubtful accounts. The report helps to estimate the value of bad debts to be written off in the company’s financial statements.

Management can apply a fixed percentage of default to each category based on the number of days since the respective invoice was raised. The aggregate of the products from each category can provide an estimate regarding uncollectible receivables. Invoices that have been due for longer periods of time have a higher probability of defaultProbability of DefaultProbability of Default (PD) is the probability of a borrower defaulting on loan repayments and is used to calculate the expected loss from an investment..

In the example above, the company has $12,000 of accounts receivables that have been outstanding for less than 30 days. Typically, the accounts are assumed to have high collectability. Thus, the company can assume that none of the accounts will be doubtful.

Next, based on prior experience, the company knows that accounts outstanding for 31-60 days typically have a 2% rate of default. Then, accounts that have been outstanding for 60-90 days have a 4% rate of default, and any older accounts have an 8% rate of default. Using the default rates and the numbers in the example above, we can calculate the company’s allowance for doubtful accounts, as shown below:

Allowance for Doubtful Accounts = (0% x 12,000) + (2% x 8,000) + (4% x 1,000) + (8% x 1,000) = $280

Based on the calculation above, we can see that the company’s allowance for doubtful accounts comes to $280.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Accounts Payable vs Accounts ReceivableAccounts Payable vs Accounts ReceivableIn accounting, accounts payable and accounts receivable are sometimes confused with the other. The two types of accounts are very similar in

- Cash Conversion CycleCash Conversion CycleThe Cash Conversion Cycle (CCC) is a metric that shows the amount of time it takes a company to convert its investments in inventory to cash. The cash conversion cycle formula measures the amount of time, in days, it takes for a company to turn its resource inputs into cash. Formula

- How to Record Payment in AccountingHow to Record Payments in AccountingRecording payments in accounting can otherwise be referred to as "accounts payable," which means the total amount a given company owes to

- Template – Aging ReportAging Report TemplateThis aging report template will help you categorize accounts receivables based on how long invoices have been outstanding.

-

Understanding the Chart of Accounts: A Comprehensive Guide

The chart of accounts is a tool that lists all the financial accounts included in the financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance

-

Closing Entries: A Comprehensive Guide for Accounting

A closing entry is a journal entryJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits) that is m

Accounting

- Understanding Open Credit Accounts: What You Need to Know

- Accounts Payable vs. Accounts Receivable: A Clear Explanation

- Accounts Payable (AP): Definition, Function & Importance

- Accounts Receivable (AR): Definition, Management & Forecasting

- Understanding Accounts Receivable Aging: A Comprehensive Guide

- Accounts Receivable Factoring: A Comprehensive Guide

- Accounts Receivable Turnover Ratio: Definition & Calculation

- Understanding Accounts Receivable Quality: A Key Indicator of Financial Health

- Understanding Accounts Receivable (AR): A Comprehensive Guide

-

Understanding the Accounting Cycle: A Comprehensive Guide

Understanding the Accounting Cycle: A Comprehensive GuideThe accounting cycle is the holistic process of recording and processing all financial transactions of a company, from when the transaction occurs, to its representation on the financial statementsThr...

-

Understanding Accounts Expenses: A Comprehensive Guide

Understanding Accounts Expenses: A Comprehensive GuideAn expense in accounting is the money spent, or costs incurred, by a business in their effort to generate revenues. Essentially, accounts expenses represent the cost of doing business; they are the su...