Accounts Receivable Factoring: A Comprehensive Guide

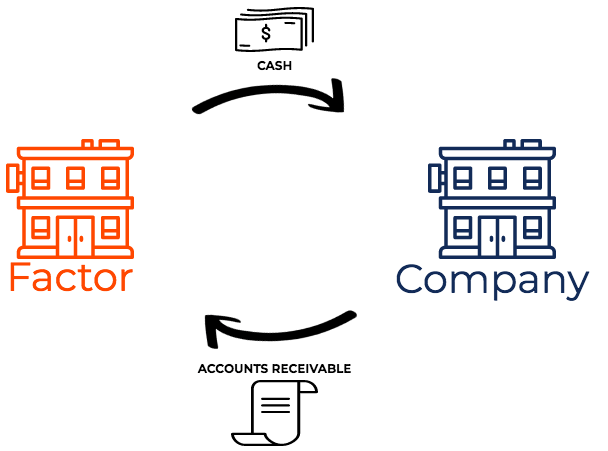

Accounts receivable factoring, also known as factoring, is a financial transaction in which a company sells its accounts receivableAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow to a finance company that specializes in buying receivables at a discount (called a factor). Accounts receivable factoring is also known as invoice factoring or accounts receivable financing.

Understanding How Accounts Receivable Factoring Works

Factoring is a financial transaction in which a company sells its receivables to a financial company (called a factor). The factor collects payment on the receivables from the company’s customers.

Companies choose factoring if they want to receive cash quickly rather than waiting for the duration of the credit termsEffective Annual Interest RateThe Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective. Factoring allows companies to immediately build up their cash balance and pay any outstanding obligations. Therefore, factoring helps companies free up capitalNet Working CapitalNet Working Capital (NWC) is the difference between a company's current assets (net of cash) and current liabilities (net of debt) on its balance sheet. that is tied up in accounts receivable and also transfers the default risk associated with the receivables to the factor.

How Accounts Receivables are Priced by Factoring Companies

Factoring companies charge what is known as a “factoring fee.” The factoring fee is a percentage of the amount of receivables being factored. The rate charged by factoring companies depends on:

- The industry that the company is in

- The volume of receivables to be factored

- The quality and creditworthiness of the company’s customers

- Days outstanding in receivables (average days outstanding)

Additionally, the rate depends on whether it is recourse factoring or non-recourse factoring. Factoring companies usually charge a lower rate for recourse factoring than it does for non-recourse factoring. When the factor is bearing all the risk of bad debts (in the case of non-recourse factoring), a higher rate is charged to compensate for the risk. With recourse factoring, the company selling its receivables still has some liability to the factoring company if some of the receivables prove uncollectible.

In essence, the easier the factoring company feels that collecting the receivables is likely to be, the lower the factoring fee.

Recourse Factoring and Non-Recourse Factoring

Accounts receivable factoring can be without recourse or with recourse.

Here is a comparison between the two:

- Transfer with recourse: In transfer with recourse, the factor can demand money back from the company that transferred receivables if it cannot collect from customers.

- Transfer without recourse: In transfer without recourse, the factor takes on all the risk of uncollectible receivables. The company that transferred receivables has no liability for uncollectible receivables.

An example of recourse factoring and non-recourse factoring is shown below.

Examples of Accounts Receivable Factoring

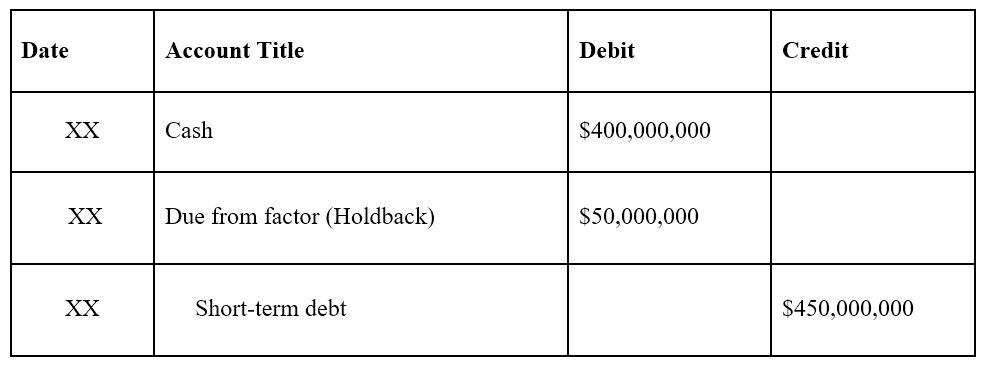

1. Transfer without recourse

Company A transfers $500 million of receivables, without recourse, for proceeds of $400 million. The journal entry would be as follows:

Note: $100 million is considered interest expense. It shows that the company obtained cash flow earlier than it would have if it waited for the receivables to be collected.

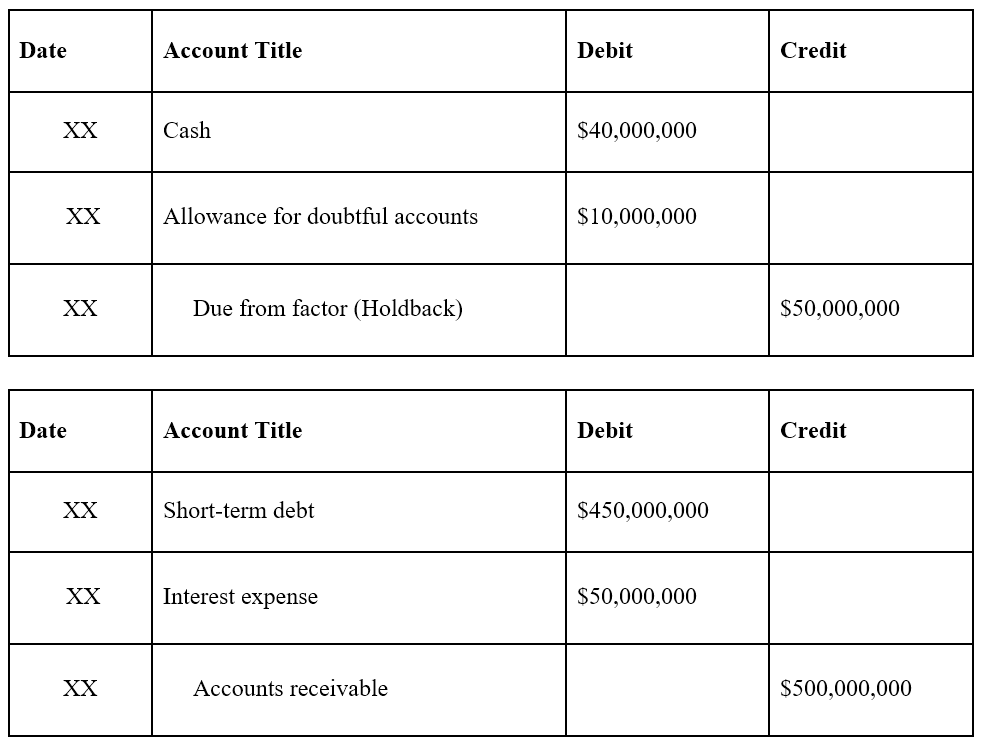

2. Transfer with recourse

Company A transfers $500 million of receivables, with recourse, for proceeds of $450 million less a $50 million holdback. Later on, the factor is able to collect receivables of $490 million ($10 million receivables uncollectible). The journal entries are as follows, with the initial journal entry below:

Note: The account “Due from factor” is the potential payment for possible non-collectibles.

After the factor collected $490 million of receivables ($10 million uncollectible):

More Resources

CFI is the official provider of the global Financial Modeling and Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Sales and Collection CycleSales and Collection CycleThe Sales and Collection Cycle, also known as the revenue, receivables, and receipts (RRR) cycle, is comprised of various classes of

- Allowance for Doubtful AccountsAllowance for Doubtful AccountsThe allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable. The amount represents the value of accounts receivable that a company does not expect to receive payment for.

- Accounts PayableAccounts PayableAccounts payable is a liability incurred when an organization receives goods or services from its suppliers on credit. Accounts payables are

- Notes ReceivablesNotes ReceivableNotes receivable are written promissory notes that give the holder, or bearer, the right to receive the amount outlined in an agreement.

-

Loans Receivable: Understanding and Analyzing Your Balance Sheet

Learning how to read a balance sheet is cruicial for all investors. A company's balance sheet displays the sum of all funds that have been lent out but have not yet been collected. This s

-

Understanding Notes Receivable: A Comprehensive Guide

Notes receivable are a balance sheet item that records the value of promissory notesPromissory NoteA promissory note refers to a financial instrument that includes a written promise from the issuer to

Accounting

- Accounts Payable vs. Accounts Receivable: A Clear Explanation

- Accounts Payable (AP): Definition, Function & Importance

- Accounts Receivable Financing: A Comprehensive Guide for Businesses

- Accounts Receivable (AR): Definition, Management & Forecasting

- Understanding Accounts Receivable Aging: A Comprehensive Guide

- Accounts Receivable Aging Report: Understanding & Analysis

- Accounts Receivable Turnover Ratio: Definition & Calculation

- Understanding Accounts Receivable Quality: A Key Indicator of Financial Health

- Understanding Accounts Receivable (AR): A Comprehensive Guide

-

Understanding the Chart of Accounts: A Comprehensive Guide

Understanding the Chart of Accounts: A Comprehensive GuideThe chart of accounts is a tool that lists all the financial accounts included in the financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance...

-

Closing Entries: A Comprehensive Guide for Accounting

Closing Entries: A Comprehensive Guide for AccountingA closing entry is a journal entryJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits) that is m...