Accounts Receivable Financing: A Comprehensive Guide for Businesses

Accounts receivable financing is a means of short-term funding that a business can draw on using its receivables. It is very useful if a timing mismatch exists between the cash inflows and outflows of the business. AR financing can take various forms, but the three major types are:

- Accounts receivable loans

- FactoringAccounts Receivable FactoringAccounts receivable factoring, also known as factoring, is a financial transaction in which a company sells its accounts receivable to a

- Asset-backed securities

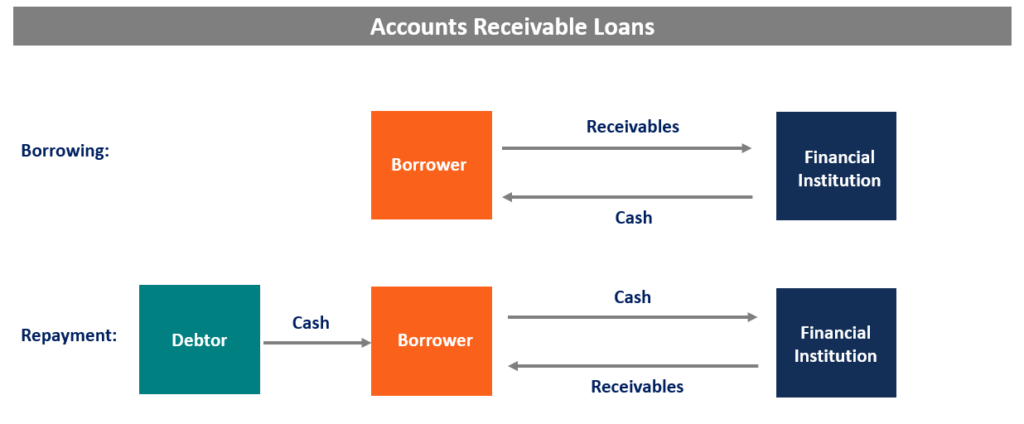

Accounts Receivable Loans

Accounts receivable loans are a source of short-term funding, where the borrower can use their accounts receivables as collateral to raise funds from a bank. The bank would typically lend a fraction – e.g., 80% – of the face value of the receivables. The fraction varies depending on the quality of receivables – the better the quality, the higher the fraction.

The borrower still owns the receivables and is responsible for collecting from their debtors. A business should only use AR loans if it keeps a good relationship with its debtors and is sure of the payments. Otherwise, there is a chance that a business might get squeezed between the bank and the debtor.

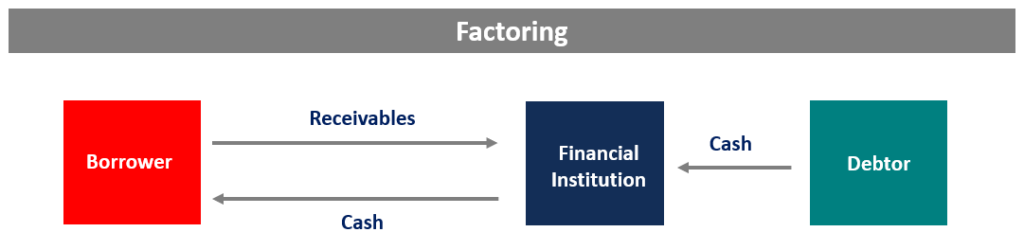

Factoring

Factoring is the most common form of accounts receivable financing for smaller businesses. Under the factoring approach, the borrower sells its receivables to a factoring institution. The receivables are sold at a discount, where the discount depends on the quality of the receivables.

Since it is an outright sale of receivables, the borrower is no longer responsible for the collection process, and the amounts are collected by the factoring organization. Factoring can be expensive, as it typically involves several fees alongside interest expenseInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also. Also, if a business wishes to maintain good relationships with its debtors, then it should use factoring sparingly.

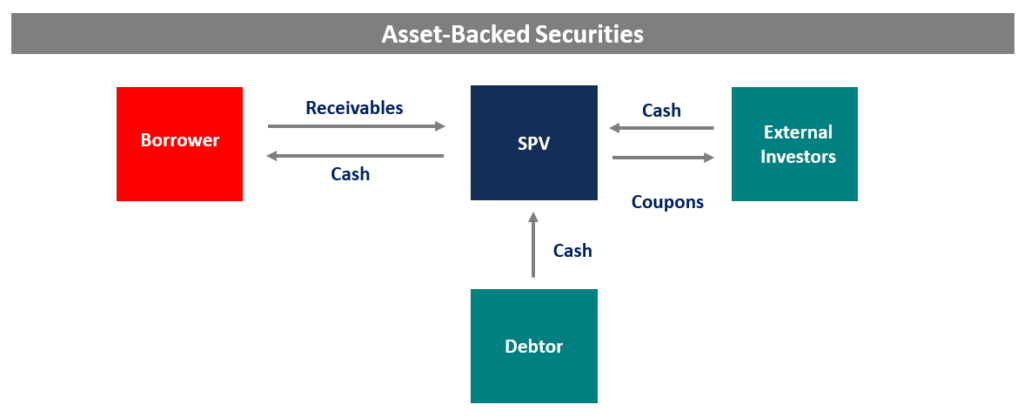

Asset-Backed Securities

Asset-backed securities (ABS) are a form of financing available to larger organizations. An ABS is a fixed-income instrument that makes coupon payments to its investors by deriving its cash flows from a pool of underlying assets. The most common example is that of mortgage-backed securities that use mortgages as their underlying assets.

A large company can securitize some or all of its receivables in a special purpose vehicle (SPV)Special Purpose Vehicle (SPV)A Special Purpose Vehicle/Entity (SPV/SPE) is a separate entity created for a specific and narrow objective, and that is held off-balance sheet. SPV is a; the instrument holds the receivables, collects payments, and passes them through to the investors.

On the other hand, the borrowing company gets money from the investors via the SPV. Again, as in the case of AR loans and factoring, the credit rating of the ABS depends on the quality and diversification level of the receivables.

Factors Affecting the Quality of Receivables

As discussed in the previous sections, the quality of receivables is key in making financing decisions. Below are a few key factors that decide the quality of a basket of receivables:

1. Creditworthiness of the debtor

The credit quality of the debtor is essential, as it is ultimately the debtor who makes the payment. So, a debtor with a poor credit ratingCredit RatingA credit rating is an opinion of a particular credit agency regarding the ability and willingness an entity (government, business, or individual) to fulfill its financial obligations in completeness and within the established due dates. A credit rating also signifies the likelihood a debtor will default. reduces the quality of the basket and increases the cost of borrowing in terms of interest or reduction of the amount being lent.

2. Duration of receivables

The duration, or age, of receivables is the number of days they are outstanding. Long-duration receivables are considered to be of lower quality because the probability of the receivables being paid goes down.

Typically, if a receivable is outstanding for more than 90 days, it is treated as a default. Hence, the shorter the duration of the basket, the lower the cost of financing.

3. Industry of the original account

The industry to which the original debtor belongs is important, as the macro trends within that industry affect the ability of the debtor to make good on their obligations. It is also important because financial institutions may want to restrict their exposure to certain industries.

4. Quality of documentation

The quality of documentation that is associated with the account is also very important, as better documentation quality provides clarity of contracts. It also provides the basis for legal recourse in case of a default. Thus, good and clear documentation improves the quality of the receivables basket.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Asset FinancingAsset FinancingAsset financing is a type of borrowing related to the assets of a company. In asset financing, the company uses its existing inventory, accounts receivable,

- Commercial Loan Documentation TrainingCommercial Loan Documentation TrainingCommercial loan documentation training is formal training provided to financial institutions and credit professionals who are involved in commercial lending

- Asset-Backed Commercial Paper (ABCP)Asset-Backed Commercial Paper (ABCP)An asset-backed commercial paper (ABCP) is a short-term monetary-market debt instrument collateralized by a package of loans.

- Quality of Accounts ReceivablesQuality of Accounts ReceivableThe quality of accounts receivables is the likelihood that the cash flows that are owed to a company in the form of receivables are going to

-

Series B Funding: A Comprehensive Guide for Startups

Series B financing (also known as series B round or series B funding) is one of the stages in the capital-raising process of a startup. Essentially, the series B round is the third stage of startup fi

-

Understanding Accounts Receivable (AR): A Comprehensive Guide

Accounts receivable are cash amounts that clients owe your company. The goods or services have been delivered and the invoice sent. Now, it’s just a matter of time before you receive payment for a job

finance

- Accounts Payable vs. Accounts Receivable: A Clear Explanation

- Accounts Receivable to Sales Ratio: Definition & Analysis

- Debt Financing: A Comprehensive Guide for Businesses

- Vendor Financing: A Comprehensive Guide for Businesses

- Accounts Receivable (AR): Definition, Management & Forecasting

- Understanding Accounts Receivable Aging: A Comprehensive Guide

- Accounts Receivable Aging Report: Understanding & Analysis

- Accounts Receivable Factoring: A Comprehensive Guide

- Understanding Accounts Receivable Quality: A Key Indicator of Financial Health

-

Accounts Payable (AP): Definition, Function & Importance

Accounts Payable (AP): Definition, Function & ImportanceA company’s accounts payable represents its short-term liabilities—invoices owed to suppliers, for example. AP departments are responsible for processing expense...

-

Series A Funding: Definition, Stages & What to Expect

Series A Funding: Definition, Stages & What to ExpectSeries A financing (also known as series A round or series A funding) is one of the stages in the capital-raising process by a startup. Essentially, the series A round is the second stage of startup f...