Understanding Equity Statements: A Comprehensive Guide

An equity statement – also referred to as a statement of owner’s equity or statement of changes in equity – is a financial statement that a company is required to prepare along with other important financial documents at the end of a reporting period. In the United States, the statement of changes in equity is also called the statement of retained earningsStatement of Retained EarningsThe statement of retained earnings provides an overview of the changes in a company's retained earnings during a specific accounting cycle. It is structured as an equation, such that it opens with the retained earnings at the beginning of the reporting period, makes adjustments for items such as net income and dividends.

The statement of owner’s equity reports the changes in company equity. The changes that are generally reflected in the equity statement include the earned profits, dividends, inflow of equity, withdrawal of equity, net loss, and so on.

Summary

- Equity, in the simplest terms, is the money shareholders have invested in the business including all accumulated earnings.

- An equity statement is a financial statement that a company is required to prepare along with other important financial documents at the end of the financial year.

- The statement of owner’s equity reports the changes in company equity, from an opening balance to and end of period balance. The changes include the earned profits, dividends, inflow of equity, withdrawal of equity, net loss, and so on.

What is Equity?

Equity, in the simplest terms, is the money shareholders have invested in the business. It constitutes a part of the total capitalCapitalCapital is anything that increases one’s ability to generate value. It can be used to increase value across a wide range of categories, such as financial, social, physical, intellectual, etc. In business and economics, the two most common types of capital are financial and human. invested in the business, which doesn’t belong to debt holders.

Equity on the Balance Sheet

On the company’s balance sheet, shareholder’s equity is represented under the heading “Shareholder’s Equity” or “Stockholder’s Equity.” The section usually comprises three components:

- Share capital

- Retained earnings

- Net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through

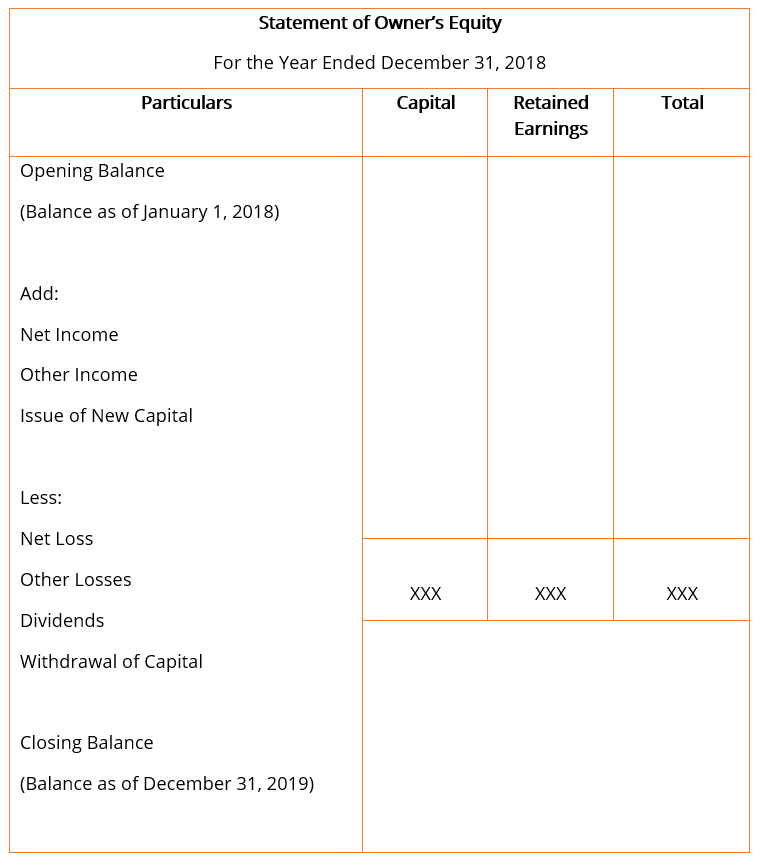

The general format for the statement of owner’s equity, with the most basic line items, usually looks like the one shown below.

Line Items

- Opening Balance: The opening balance is the ending balance of the previous year’s statement of shareholder’s equity. All further additions and subtractions in the current financial year are made to the opening balance in the equity statement.

- Net Income: Net income is the total income earned by the company during the fiscal yearFiscal Year (FY)A fiscal year (FY) is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to formulate annual, after accounting for all operating and non-operating expenses. The value is taken from the income statement, also known as the profit & loss statement, that is prepared at the end of the fiscal year.

- Other Income: All additional income earned by the company that might not have been recognized in the income statement is accounted for on the equity statement. Examples of other income include actuarial or unrealized gains from financial instruments.

- Issue of New Capital: When new shares are issued and when there is an inflow of capital or an addition to the shareholder’s equity in the company, it is added to the total shareholder’s equity.

- Net Loss: Net loss is the loss incurred by the company during the fiscal year as a result of its operations. It reduces the company’s total capital and is hence deducted in the statement of shareholder’s equity.

- Other Loss: Just like other income, the expenses incurred or loss that is incurred by the company but not recognized in the income statement is accounted for in the equity statement. A good example of other comprehensive losses is actuarial or unrealized losses form financial derivatives.

- Dividends: A dividend is a reward or return earned by the shareholders of the company on their investment in the company’s shares. The dividend payments made to the shareholders reduce the total shareholder’s equity of the company and are hence deducted in the statement of shareholder’s equity.

- Withdrawal of Capital: When shares are redeemed or capital is withdrawn from the company, it is shown as a deduction in the statement of shareholder’s equity, as it reduces the total equity of the company.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Dividend PolicyDividend PolicyA company’s dividend policy dictates the amount of dividends paid out by the company to its shareholders and the frequency with which the dividends are paid

- Fiscal Year (FY)Fiscal Year (FY)A fiscal year (FY) is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to formulate annual

- Profit & Loss StatementProfit and Loss Statement (P&L)A profit and loss statement (P&L), or income statement or statement of operations, is a financial report that provides a summary of a

- Three Financial StatementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are

-

Understanding Deficit Equity: Causes, Impacts & Solutions

Deficit equity, more commonly referred to as negative owners' equity, results when the total value of an organization's assets is less than the sum total of its liabilities. In any company, &q

-

Understanding Your Insurance Policy Statement: A Comprehensive Guide

An insurance policy statement is a form outlining the policyholder's insurance coverage. The statement attests that a person had insurance on a specific date. Insurance Policies

Accounting

- Understanding HOA Statements: A Comprehensive Guide

- Understanding Account Statements: A Comprehensive Guide

- Backstop: Understanding Financial Safety Nets and Contingency Funding

- Understanding Equity: A Comprehensive Guide for Investors

- Equity Crowdfunding: A Comprehensive Guide for Startups & Investors

- Understanding Negative Equity: Causes, Risks & Solutions

- Growth Equity: Investing in Expanding Businesses | [Your Company Name]

- Understanding Home Equity: A Comprehensive Guide

- Understanding Bank Statements: A Comprehensive Guide

-

Margin Equity Percentage: Understanding Your Brokerage Loan Limits

Margin Equity Percentage: Understanding Your Brokerage Loan LimitsA brokerage margin account allows an investor to buy stocks and other securities with a portion of the purchase price paid with a margin loan from the broker. A brokerage margin account allow...

-

Understanding Liquid Equity: A Guide to Company Stock

Understanding Liquid Equity: A Guide to Company StockLiquid equities can be bought and sold quickly. Equity is another name for a company stock. When you buy shares in company stock, you take an ownership interest in the company and each share ...