Asset Swap Explained: Definition, OTC Trading & Key Concepts

An asset swap is a derivative contract between two parties that swap fixed and floating assets. The transactions are done over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of securities between two counter-parties executed outside of formal exchanges and without the supervision of an exchange regulator. OTC trading is done in over-the-counter markets (a decentralized place with no physical location), through dealer networks. based on an amount and terms agreed upon by both sides of the transaction.

Essentially, asset swaps can be used to substitute the fixed coupon interest rates of a bond with LIBOR-adjusted floating rates. The goal of the swap is to change the form of the cash flow on the reference asset to hedge against different types of risks. The risks include interest risk, credit riskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally,, and more.

Normally, an asset swap starts with the investor acquiring a bond position. Then, the investor will swap the fixed rate of the bond with a floating rate through the bank. It means that the investor will be paying the fixed rate to the bank, but they will be receiving a floating rate, usually based on LIBORLIBORLIBOR, which is an acronym of London Interbank Offer Rate, refers to the interest rate that UK banks charge other financial institutions for from the bank.

Summary

- An asset swap is a derivative contract between two parties that swap fixed and floating assets.

- In an asset swap, an investor will pay a fixed rate to the bank and receive a floating rate in return.

- Asset swaps serve to hedge against different risks on the reference asset.

How It Works

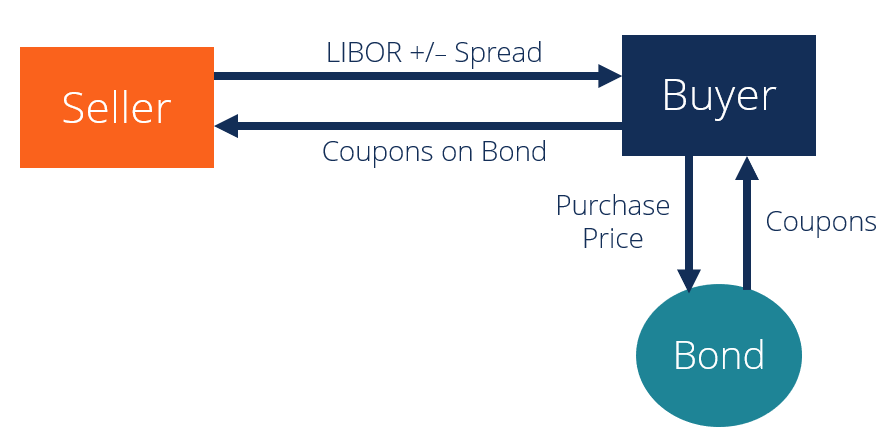

Let’s say a buyer wants to buy a bond but is intimidated by the credit risk of default or bankruptcyBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts of the company. For example, the buyer might want to purchase an oil & gas corporate bond for ten years but is afraid of a possible default around Year 5. Naturally, the buyer would want to hedge against such a credit risk, so they would enter into an asset swap.

Let’s break the swap down into two steps.

There are two main parties involved: 1) the buyer/investor, and 2) the bond seller.

Step 1: To start, the bond buyer buys the bond from the bond seller for the “dirty price” (full price at par plus accrued interest).

Step 2: The bond buyer and seller will negotiate a contract that results in the buyer paying fixed coupons to the seller equivalent to the bond coupon rates in exchange for the seller providing the buyer with LIBOR-based floating coupons. The value of the swap would be the spread that the seller pays over or under LIBOR. It is based on two things:

- The coupon values of the asset compared to the market rate.

- The accrued interest and the clean price premium or discount compared to par value.

The swap shares the same maturity as the original coupon. It means that in the event of the bond defaulting, the buyer will still receive the LIBOR-based floating coupon +/- the spread from the seller.

Let us refer to the original oil and gas corporate bond example. Assume, in Year 5, the bond does default. Even though the bond will no longer pay the fixed coupons, the bank will still need to continuously pay the buyer the floating rate until maturity. This is how the buyer hedges against the original risk.

Example of an Asset Swap

Let’s look at a specific example with actual numbers. We are looking at a risky bond with the following information.

- Currency: USD

- Issue: March 31, 2020

- Maturity: March 31, 2025

- Coupon: 7% (annual rate)

- Price (Dirty)*: 105%

- Swap Rate: 6%

- Price Premium: 0.5%

- Credit Rating: BBB

*Dirty Price: The cost of a bond that includes accrued interest based on the coupon rate.

Let us break down our example with the steps listed above.

Step 1: The buyer will pay 105% of the par value, in addition to 7% fixed coupons. We assume the swap rate is 6%. When the buyer enters into the swap with the seller, the buyer will pay the fixed coupons in return for the LIBOR +/– spread.

Step 2: The asset swap price (the spread) is calculated through the fixed coupon rate, the swap rate, and the price premium. Here, the fixed coupon rate is 7%, the swap rate is 6%, and the price premium during the swap’s lifetime is 0.5%.

Asset Spread = Fixed Coupon Rate – Swap Rate – Price Premium

Asset Spread = 7% – 6% – 0.5% = 0.5%

Steps 1 and 2 will result in a net spread of 0.5%. The asset swap will be quoted as LIBOR + 0.5% (or LIBOR plus 50 bps).

Let us say, for example, that the bond defaults in 2022 even though there are still three years left until maturity in 2025. Remember that the swap shares the same maturity as the coupon. It means that although the bond will no longer pay coupons, the seller will continue paying the buyer with the LIBOR + 0.5% until 2025. It an example of the buyer successfully hedging against credit risk.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

- Applicable Federal Rate (AFR)Applicable Federal Rate (AFR)The applicable federal rate (AFR) is the interest rate that applies to personal loans. It is the minimum rate applicable to such loans under U.S. law.

- Credit SpreadCredit SpreadCredit spread is the difference between the yield (return) of two different debt instruments with the same maturity but different credit ratings.

- Probability of DefaultProbability of DefaultProbability of Default (PD) is the probability of a borrower defaulting on loan repayments and is used to calculate the expected loss from an investment.

- Guide to Commodity TradingGuide to Commodity Trading SecretsSuccessful commodity traders know the commodity trading secrets and distinguish between trading different types of financial markets. Trading commodities is different from trading stocks.

-

Amortized Bonds: Understanding Principal Repayment

An amortized bond is a bond with the principal amount – otherwise known as face value –regularly paid down over the life of the bond. The bond’s principal is divided up according to

-

Asset Swap Explained: Definition, OTC Trading & Key Concepts

An asset swap is a derivative contract between two parties that swap fixed and floating assets. The transactions are done over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of

invest

- ASCOT Options: Understanding Asset-Swapped Convertible Options

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Noncallable Securities: A Comprehensive Guide

- Samurai Bonds: A Guide to Understanding Yen-Denominated Corporate Debt

- Swaptions Explained: Understanding Interest Rate Option Contracts

- Treasury Bonds: A Comprehensive Guide to U.S. Government Debt

- Variance Swaps: Understanding Volatility Derivatives

- Zero-Coupon Bonds: Definition, How They Work & Examples

-

Understanding Bond Accretion: A Comprehensive Guide

Understanding Bond Accretion: A Comprehensive GuideAccretion is a finance term that refers to the increment in the value of a bond after purchasing it at a discount and holding it until the maturity date. A bond is said to be purchased at a discount p...

-

Understanding Amortizable Bond Premiums: A Comprehensive Guide

Understanding Amortizable Bond Premiums: A Comprehensive GuideAn amortizable bond premium refers to the excess amount paid for a bond over its face value or par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a...