Operating Cash Flow Formula: Calculation & Explanation

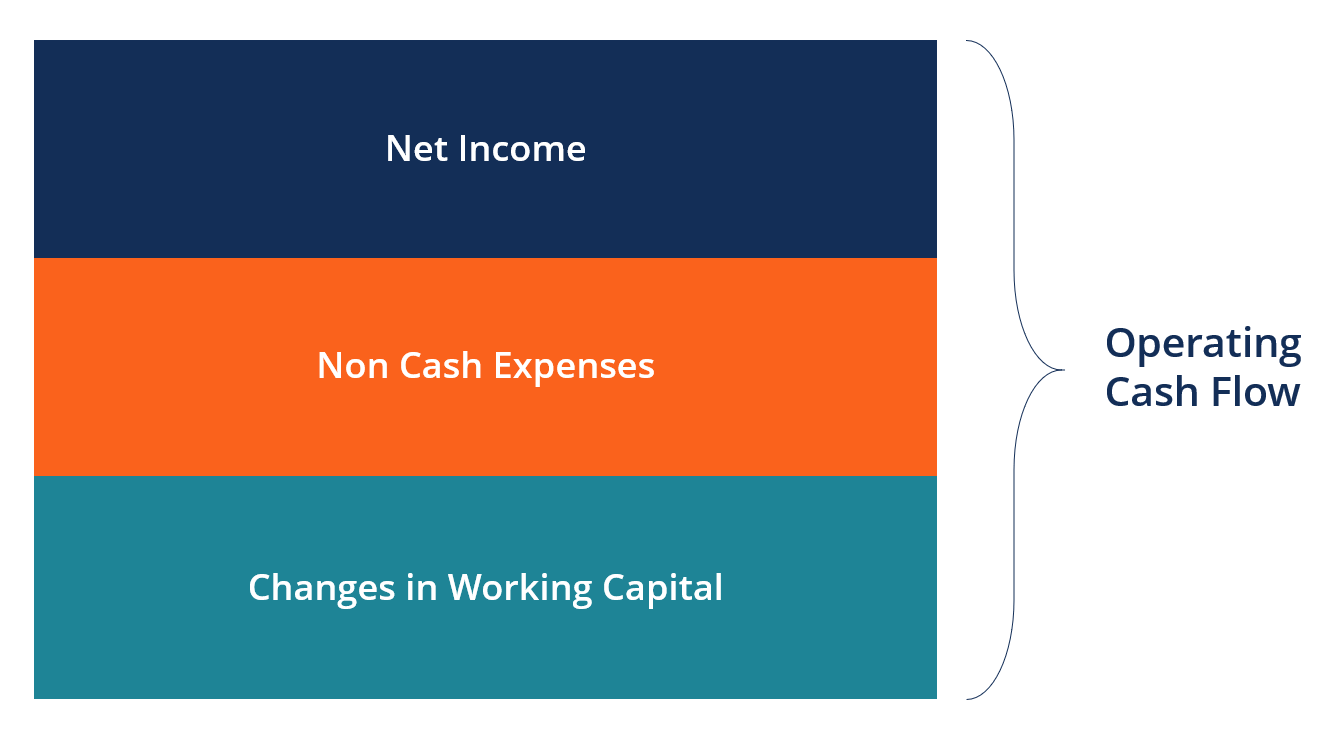

The Operating Cash Flow Formula is used to calculate how much cash a company generated (or consumed) from its operating activities in a period, and is displayed on the Cash Flow StatementCash Flow StatementA cash flow Statement contains information on how much cash a company generated and used during a given period.. The formula for each company will be different, but the basic structure always includes three components: (1) net income, (2) plus non-cash expenses, (3) plus the net increase in net working capital.

Simple Operating Cash Flow Formula

The simple operating cash flow formula is:

Operating Cash Flow = Net Income + All Non-Cash Expenses + Net Increase in Working Capital

The simple formula above can be built on to include many different items that are added back to net income, such as depreciation and amortization, as well as an increase in accounts receivable, inventory, and accounts payable. By making all adjustments to net income, we arrive at the actual, net amount of cash received or consumed by the business.

Learn this formula step by step in CFI’s Financial Analysis Fundamentals Course.

Components of the Operating Cash Flow Formula

Below are the main components explained in more detail:

1. Net Income

Net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through is the net after-tax profit of the business from the bottom of the income statement. It is the link between the income statement and the cash flow statement. To learn more about how the statements are deeply interconnected, read CFI’s guide to linking the three financial statements.

2. Non-Cash Expenses

Non-cash expenses are all accrual-based expenses that are not actually paid for with cash or credit in a given period. The most common examples of non-cash expenses include depreciation, stock-based compensation, impairment charges, and unrealized gains or losses.

3. Non-Cash Working Capital

Non-cash working capital is all current assetsCurrent AssetsCurrent assets are all assets that a company expects to convert to cash within one year. They are commonly used to measure the liquidity of a (except for cash) less all current liabilities. An increase in current assets causes a reduction in cash, while an increase in current liabilities cases an increase in cash.

The most common non-cash working capital items include:

- Accounts receivable

- Prepaid expenses

- Inventory

- Accounts payable

- Current portion of long-term debt

- Deferred revenue

Detailed Operating Cash Flow Formula

The detailed operating cash flow formula is:

Operating Cash Flow = Net income + Depreciation and amortization + Stock-based compensation + Other operating expenses and income + Deferred income taxes – Increase in inventory – Increase in accounts receivable + Increase in accounts payable + Increase in accrued expense + Increase in unearned revenue

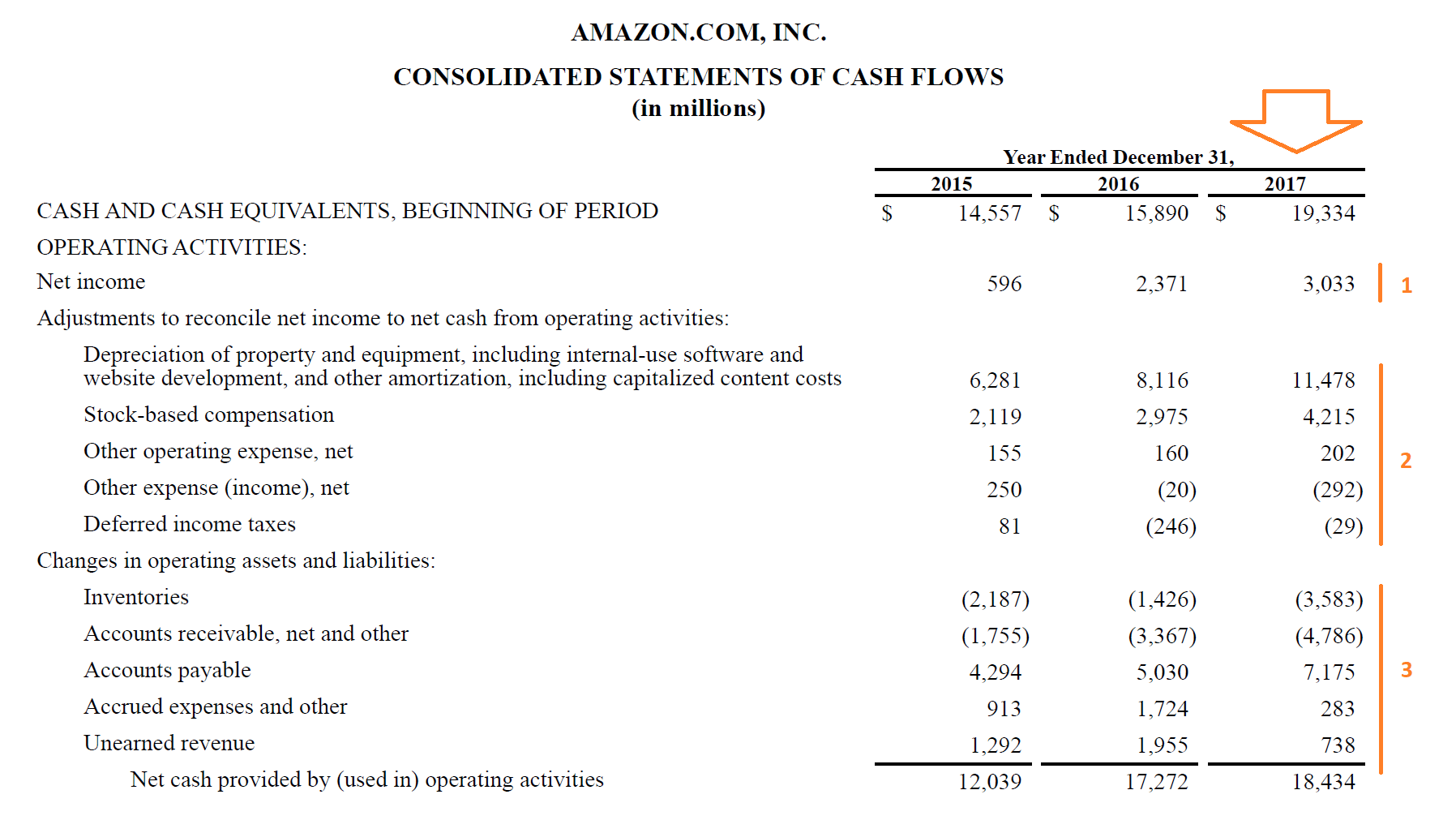

Now that you understand the basic structure of how the math and accounting works, let’s look at a detailed example using Amazon’s 2017 10-k.

As you can see, it works out to be quite a long formula, but it still consists of the three basic sections we’ve explored at the top of this guide.

Let’s explore each of the three components of the formula and their various line items in more detail:

Learn how to calculate cash flow step by step in CFI’s Financial Analysis Fundamentals Course.

Part 1 – Net Income

This part is very straightforward; it simply begins with Amazon’s 2017 net income of $3,033 million, taken directly from the income statement.

Part 2 – Non Cash Expenses

Here, we have the various non-cash expenses Amazon recorded in 2017:

Depreciation and amortization represent the accrual-based expensing of capital the company invested in maintaining its property, equipment, website, software, etc. Since the cash has already been spent on these items, the expense is added back. There are various depreciation methods a company can use.

Stock-based compensation must be recorded as an expense on the income statement, but there is no actual outflow of cash. Since the company pays the CEO, CFO, and other employees with stock, the company issues shares instead of giving them cash. There is definitely an economic cost to stock-based compensation since it dilutes other shareholders. However, when calculating operating cash flow, it must be added back.

Other operating expenses and other operating income can be found in the notes to the financial statements, and in Amazon’s case, it includes intangible asset amortization expenses, which is very similar to depreciation. Other income refers to foreign currency gains and gains on marketable securities.

Deferred income taxes refer to the difference between the income taxes the company recorded on its income statement and the taxes it actually has paid to the government. Companies calculated two taxes payable figures, one for accrual based financial statements and one for filing tax returns.

Part 3 – Changes in Net Working Capital

Here are the various changes to working capital accounts Amazon experienced in 2017:

Inventory increased by $3,583 million in the period, which resulted in that amount of cash being deducted in the period (since an increase in inventory is a use of cash).

Accounts receivable increased by $4,786 million in the period and thus reduced the cash in the period by that amount since there was more revenue unpaid by customers.

Accounts payable was higher by $7,157 million, with more money owed to suppliers and vendors, which created a positive cash flow benefit for Amazon in 2017.

Finally, accrued expenses increased (a benefit to cash flow) and unearned revenue (also called deferred revenue), when added up, resulted in more operating cash flow in the period for Amazon.

Total Operating Cash Flow

Adding Parts 1, 2 and 3 together, we get the following operating cash flow formula for Amazon:

+ $3,003 million of net income

+ $15,574 million of non-cash expenses added back

– $173 million reduction of cash due to a change in working capital

= $18,343 million of net cash from operating activities

To learn more, check out CFI’s Business Valuation Modeling Course.

Operating Cash Flow Formula vs Free Cash Flow Formula

While the operating cash flow formula is great for assessing how much a company generated from operations, there is one major limitation to the figure. All of the non-cash expenses that are added back are not accounted for in any way.

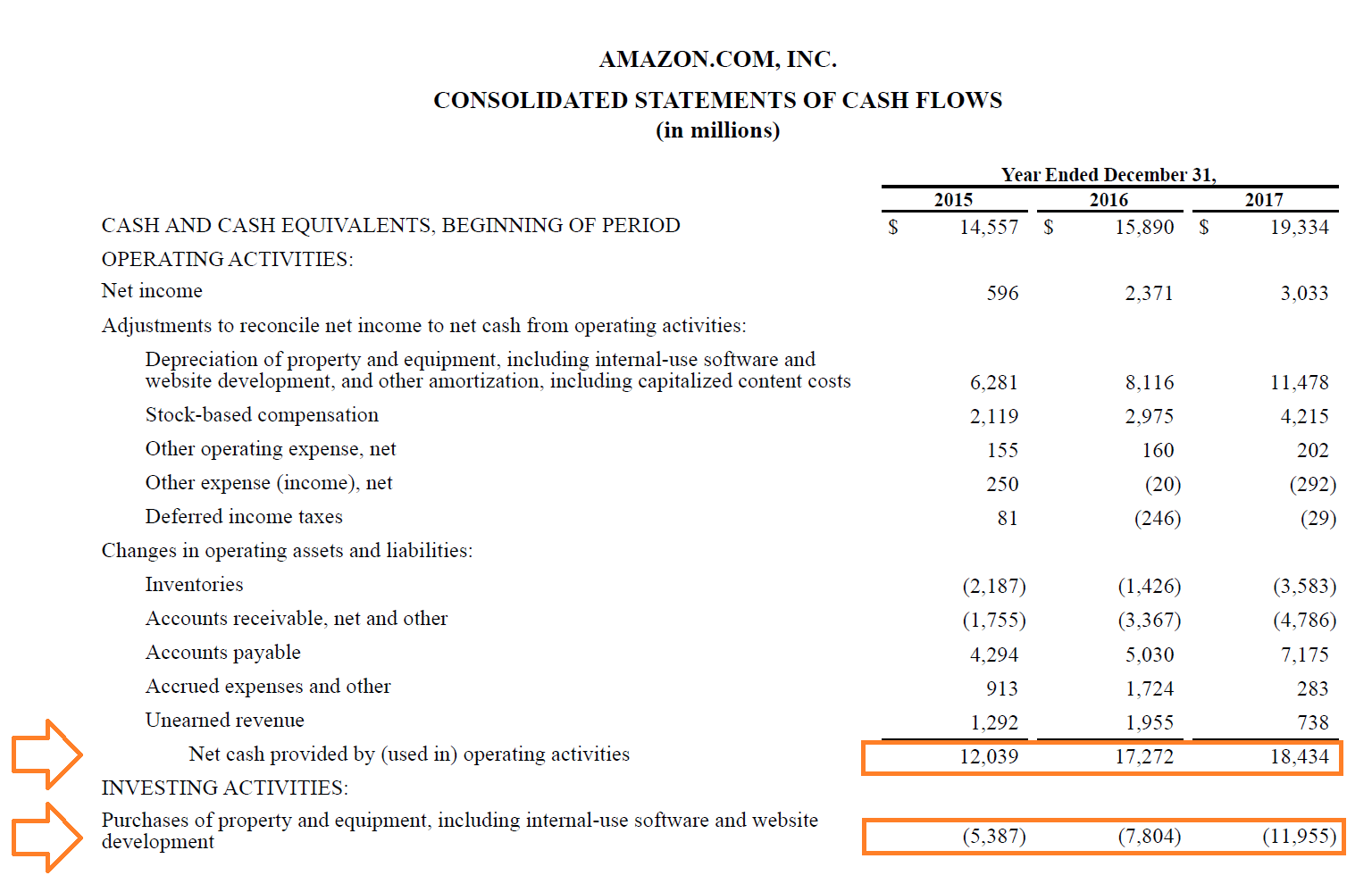

The offsetting effect of depreciation and amortization is capital expenditures. By taking capital expenditures into account, we are using the Free Cash Flow (FCF) formula.

The FCF formula is Free Cash Flow = Operating Cash Flow – Capital Expenditures.

In 2017, free cash flow is calculated as $18,343 million minus $11,955 million, which equals $6,479 million. This represents the amount of cash generated after reinvestment was made back into the business.

To learn more, check out CFI’s Business Valuation Modeling Course.

Additional Resources

Thank you for reading this guide to understanding the Operating Cash Flow Formula, and how cash flow from operations is calculated and what it means.

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Business Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

- Enterprise Value vs Equity ValueEnterprise Value vs Equity ValueEnterprise value vs equity value. This guide explains the difference between the enterprise value (firm value) and the equity value of a business. See an example of how to calculate each and download the calculator. Enterprise value = equity value + debt - cash. Learn the meaning and how each is used in valuation

- FCFF vs FCFEFCFF vs FCFEThere are two types of Free Cash Flows: Free Cash Flow to Firm (FCFF), commonly referred to as Unlevered Free Cash Flow; and Free Cash Flow to Equity (FCFE), commonly referred to as Levered Free Cash Flow. It is important to understand the difference between FCFF vs FCFE as the discount rate and numerator of valuation

- Types of Financial ModelsTypes of Financial ModelsThe most common types of financial models include: 3 statement model, DCF model, M&A model, LBO model, budget model. Discover the top 10 types

-

Operating Ratio: Definition, Calculation & Importance

The operating ratio is a measure of efficiency that is used by management to determine day-to-day operational performance. This metric compares operating expenses, also known as OPEX, to net sales. Th

-

Understanding Unconventional Cash Flow: A Comprehensive Guide

An unconventional cash flow profile is a series of cash flowsCash FlowCash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term

Accounting

- Understanding Cash Flow: A Comprehensive Guide

- Cash Flow to Debt Ratio: Understanding and Calculation

- Understanding the Operating Cash Flow Ratio: A Key Liquidity Metric

- Operating Cash to Debt Ratio: Understanding Financial Health

- Price-to-Cash Flow Ratio (P/CF): Definition & Analysis

- Understanding Cash Flow from Operations: A Comprehensive Guide

- Understanding Operating Cash Flow (OCF): A Comprehensive Guide

- Understanding the Statement of Cash Flows: A Comprehensive Guide

- Understanding Operating Cash Flow: A Key Metric for Investment

-

Understanding Conventional Cash Flow: Definitions and Examples

Understanding Conventional Cash Flow: Definitions and ExamplesConventional cash flow is a series of cash flows which, over time, go in one direction. It means that if the initial transaction is an outflow, then it will be followed by successive periods of inward...

-

EBIT Explained: Understanding Earnings Before Interest & Taxes

EBIT Explained: Understanding Earnings Before Interest & TaxesEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statementIncome StatementThe Income Statement is one of a companys core financial statements...