Understanding the Operating Cycle: Definition & Importance

An Operating Cycle (OC) refers to the days required for a business to receive inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a, sell the inventory, and collect cash from the sale of the inventory. This cycle plays a major role in determining the efficiency of a business.

Formula

The OC formula is as follows:

Operating Cycle = Inventory Period + Accounts Receivable Period

Where:

- Inventory Period is the amount of time inventory sits in storage until sold.

- Accounts Receivable Period is the time it takes to collect cash from the sale of the inventory.

Uses of the Operating Cycle Formula

Using the Operating Cycle formula above:

- The Inventory Period is calculated as follows:

Inventory Period = 365 / Inventory Turnover

Where the formula for Inventory Turnover is:

Inventory Turnover = Cost of Goods Sold / Average Inventory

- The Accounts Receivable Period is calculated as follows:

Accounts Receivable Period = 365 / Receivables Turnover

Where the formula for Receivables Turnover is:

Receivables Turnover = Credit Sales / Average Accounts Receivable

Therefore, the detailed formula for OC is:

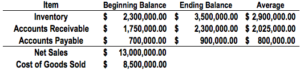

Sample Calculation

Calculating the OC with the data provided above:

- Inventory Turnover: $8,500,000 / $2,900,000 = 2.931

- Inventory Period: 365 / 2.931 = 124.53

- Receivables Turnover: $13,000,000 / $2,025,000 = 6.419

- Accounts Receivable Period: 365 / 6.419 = 56.862

Operating Cycle = 124.53 + 56.862 = 181.38 = 182 days

Importance of the Operating Cycle

The OC offers an insight into a company’s operating efficiency. A shorter cycle is preferred and indicates a more efficient and successful business. A shorter cycle indicates that a company is able to recover its inventory investment quickly and possesses enough cash to meet obligations. If a company’s OC is long, it can create cash flowCash FlowCash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period. There are many types of CF problems.

A company can reduce its OC in two ways:

- Speed up the sale of its inventory: If a company is able to quickly sell its inventory, the OC should decrease.

- Reduce the time needed to collect receivables: If a company is able to quickly collect credit sales more quickly, the OC would decrease.

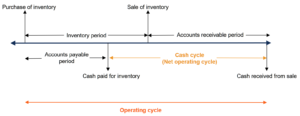

Net Operating Cycle (Cash Cycle) vs Operating Cycle

The operating cycle (OC) is often confused with the net operating cycle (NOC). The NOC is also known as the cash conversion cycle or cash cycle and indicates how long it takes a company to collect cash from the sale of inventory. To differentiate the two:

- Operating Cycle: The length of time between the purchase of inventory and the cash collected from the sale of inventory.

- Net Operating Cycle: The length of time between paying for inventory and the cash collected from the sale of inventory.

Additionally, the formula for the NOC is as follows:

Net Operating Cycle = Inventory Period + Accounts Receivable Period – Accounts Payable Period

The difference between the two formulas lies in NOC subtracting the accounts payable period. This is done because the NOC is only concerned with the time between paying for inventory to the cash collected from the sale of inventory.

The following image illustrates the difference between the cycles:

Other Resources

CFI’s mission is to help anyone in the world become a great financial analyst through the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! designation. To continue learning and advancing your career, these free CFI resources will be helpful:

- Business Life CycleBusiness Life CycleThe business life cycle is the progression of a business in phases over time, and is most commonly divided into five stages

- Day Sales InventoryDays Sales in Inventory (DSI)Days Sales in Inventory (DSI), sometimes known as inventory days or days in inventory, is a measurement of the average number of days or time

- Inventory ShrinkageInventory ShrinkageInventory shrinkage occurs when the number of products in stock are fewer than those recorded on the inventory list. The discrepancy may

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

Cycle Stock: A Guide to Optimized Inventory Management

Having enough inventory on hand to meet customer demand is crucial to maintain and grow your business. Companies must not only carry enough inventory to meet forecasts, but a cushion of additional goo

-

![Operating Profit Margin: Definition & Calculation | [Your Company Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815165062_S.png)

Operating Profit Margin: Definition & Calculation | [Your Company Name]

Operating Profit Margin is a profitability or performance ratio that reflects the percentage of profit a company produces from its operations, prior to subtracting taxes and interest charges. It is ca

Accounting

- Inventory Turnover Ratio: Definition & Calculation | AccountingTools

- Understanding Operating Risk: A Key Component of Business Risk

- Understanding Shadow Inventory: What Banks Hold & What It Means for the Market

- Understanding Throughput: A Key Metric for Business Efficiency

- Understanding Market Cycles: Trends & Economic Environments

- Understanding Inventory: Definition & Importance in Financial Statements

- Inventory Shrinkage: Causes, Impact & Reconciliation

- Operating Lease Explained: Benefits & How They Work

- Understanding Operating Leases: Definition & Benefits

-

Operating Margin: Definition, Calculation & Importance

Operating Margin: Definition, Calculation & ImportanceOperating margin is equal to operating incomeOperating IncomeOperating income is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue. divided by rev...

-

Understanding Inventory Quality: Definition & Importance

Understanding Inventory Quality: Definition & ImportanceInventory refers to all goods and materials that are held by a business with the goal of selling them for a profit or for use in the production process of finished goods. In the manufacturing industry...