Operating Margin: Definition, Calculation & Importance

Operating margin is equal to operating incomeOperating IncomeOperating income is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue. divided by revenue. Operating margin is a profitability ratio measuring revenue after covering operating and non-operating expenses of a business. Also referred to as return on sales, the operating income indicates how much of the generated sales is left when all operating expenses are paid off.

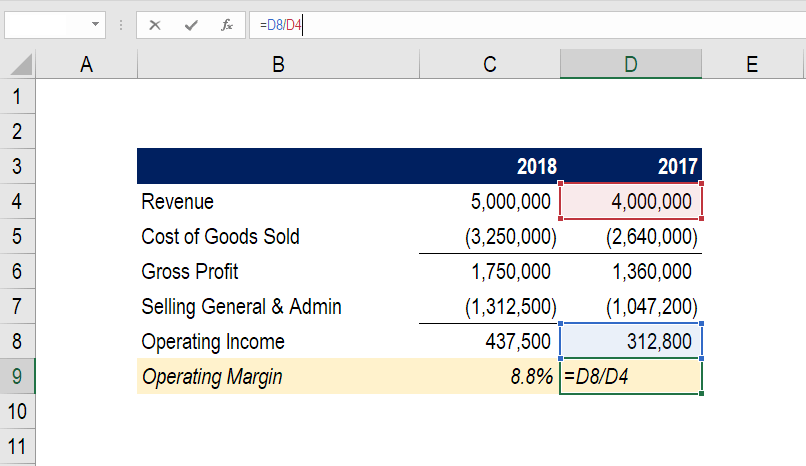

In the above example, you can clearly see how to arrive at the 2018 operating margin for this company. 2018 starts with Revenue of $5 million, less COGS of $3.25 million, resulting in Gross Profit of $1.75 million.

From there, another $1.3 million of Selling General & Administrative SG&A expenses are deducted, to arrive at Operating Income of $437,500.

By taking $437,500 and dividing it by $5.0 million you arrive at the operating margin of 8.8%.

What is the formula for Operating margin?

Operating Margin = Operating Income / Revenue X 100

Another example:

DT Clinton Manufacturing company reported on its 2015 annual income statement a total of $125 million in sales revenue. Operating income before tax netted to $45 million after deducting all $80 million in operating expenses for the year. As a result, an operating margin of 36% was generated, or in other words for every dollar in sales achieved, $0.36 cents is retained as operating profit.

What is Operating Income?

Operating income is the profit of a business after all operating expenses are deducted from sales receipts or revenue. It represents how much a company is making from its core operations, not including other income sources not directly related to its main business activities. It differs from net income in that it does not include the expenses of taxes and interest.

This gives investors and creditors a clear indication as to whether a company’s core business is profitable or not, before considering non-operating items.

What is Sales Revenue?

Sales revenueSales RevenueSales revenue is the income received by a company from its sales of goods or the provision of services. In accounting, the terms "sales" and or net sales is the monetary amount obtained from selling goods and services to business customers, excluding any merchandise returned and allowances/discounts offered to customers. This can be realized either as cash sales or credit sales.

Why is Profit Margin important in business?

A business that is capable of generating operating profit rather than operating at a loss is a positive sign for potential investors and existing creditors. This means that the company’s operating margin creates value for shareholders and continuous loan servicing for lenders. The higher the margin that a company has, the less financial risk it has – as compared to having a lower ratio, indicating a lower profit margin.

Continued increases in profit marginNet Profit MarginNet Profit Margin (also known as "Profit Margin" or "Net Profit Margin Ratio") is a financial ratio used to calculate the percentage of profit a company produces from its total revenue. It measures the amount of net profit a company obtains per dollar of revenue gained. over time shows that profitability is improving. This may either be attributed to efficient control of operating costs or other factors that influence revenue build-ups such as higher pricing, better marketing, and increases in customer demand.

The drawbacks of looking at operating margin/profit

Operating profit is an accounting metric, and therefore not an indicator of economic value or cash flow. Profit includes several non-cash expenses such as depreciation and amortization, stock-based compensation, and other items. Conversely, it doesn’t include capital expenditures and changes in working capital.

In conjunction, these various items that are included or excluded can cause cash flow (the ultimate driver of value for a business) to be very different (higher or lower) than operating profit.

To learn more, read all about business valuationValuationValuation refers to the process of determining the present worth of a company or an asset. It can be done using a number of techniques. Analysts that want.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Read more about profit and loss metrics:

Thank you for reading CFI’s guide to operating margin. See the following CFI resources to learn more.

- Net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through

- EBITDAEBITDAEBITDA or Earnings Before Interest, Tax, Depreciation, Amortization is a company's profits before any of these net deductions are made. EBITDA focuses on the operating decisions of a business because it looks at the business’ profitability from core operations before the impact of capital structure. Formula, examples

- Operating incomeOperating IncomeOperating income is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue.

- Depreciation scheduleDepreciation ScheduleA depreciation schedule is required in financial modeling to link the three financial statements (income, balance sheet, cash flow) in Excel.

-

Margin Debt Explained: Understanding Brokerage Loans for Investing

Margin debt represents the amount that an investor owes a broker in their margin account. When a broker approves a margin account for an investor, the margin account is granted a line of credit that c

-

Understanding Sellouts in Investing: Non-Economic Forced Liquidations

A sellout is a situation where investors are compelled to dispose of their assets due to non-economic factors, such as divorce, illness, or margin calls by a brokerage firm. In times of panic, investo

Accounting

- Understanding Gross Profit Margin: Definition & Calculation

- Net Profit Margin: Definition, Calculation & Importance

- Operating Profit Margin: Definition & Calculation | [Your Company Name]

- Understanding Profitability Ratios: A Comprehensive Guide

- Marginal Profit: Definition, Calculation & Maximization

- Understanding Markup: Definition, Calculation & Importance

- Operating Lease Explained: Benefits & How They Work

- Understanding Profit: A Key Financial Metric

- Profit Margin Explained: Types & How to Calculate

-

Margin Trading Explained: Borrowing Money to Invest

Margin Trading Explained: Borrowing Money to InvestThe term “margin” refers to the amount deposited with a brokerage when borrowing money to buy securities. When an investor buys securities on margin, it means they are using borrowed money...

-

Margin Accounts: Borrowing to Invest & Increase Buying Power

Margin Accounts: Borrowing to Invest & Increase Buying PowerA margin account refers to a type of brokerage account that investors use where they can borrow funds to purchase financial products. Investors are required to pay a monthly interest rate on the amoun...