Percentage of Completion Method: Accounting Explained

The percentage of completion method is a revenue recognition accounting concept that evaluates how to realize revenue periodically over a long-term project or contract. Revenue, expenses, and gross profitGross ProfitGross profit is the direct profit left over after deducting the cost of goods sold, or cost of sales, from sales revenue. It's used to calculate the gross profit margin. are recognized each period based on the percentage of work completed or costs incurred.

Understanding the Percentage of Completion Method

The percentage of completion method falls in-line with IFRS 15, which indicates that revenue from performance obligations recognized over a period of time should be based on the percentage of completion. The method recognizes revenues and expenses in proportion to the completeness of the contracted project. It is commonly measured through the cost-to-cost method.

There are two conditions to use the percentage of completion method:

- Collections by the company must be reasonably assured.

- Costs and project completion must be reasonably estimated.

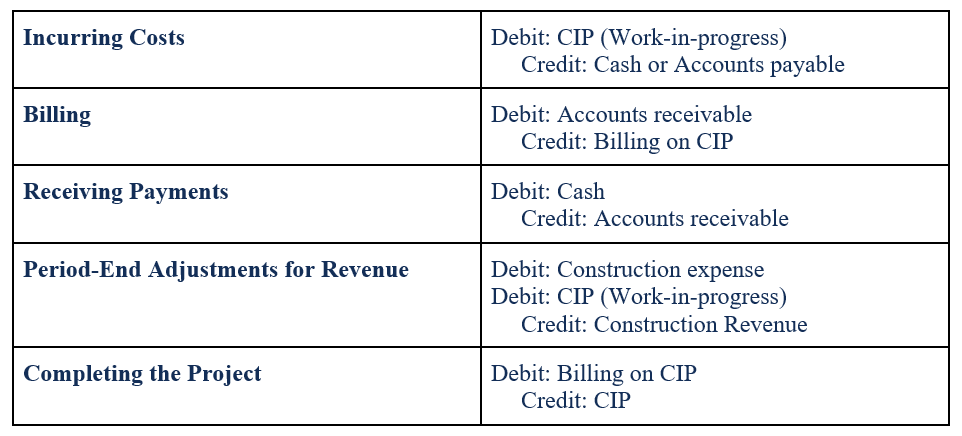

Journal Entries: Percentage of Completion Method

Journal entriesJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits) for the percentage of completion method are as follows:

Cost-To-Cost Approach

In the cost-to-cost approach, the percentage of completion is based on the costs incurred to the estimated total cost to complete the project. Therefore, the equation for the cost-to-cost estimate of percentage completion is:

Percentage complete:

Revenue recognized:

An example is provided below to clarify the cost-to-cost approach.

Example of the Cost-To-Cost Approach

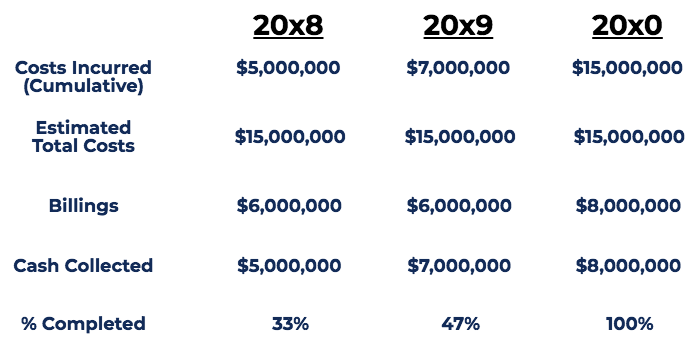

StrongBridges Ltd. was awarded a $20 million contract to build a bridge. The estimated time to complete the project is three (3) years, with an estimated cost of $15 million. Assuming that the cost estimates do not change, the project is expected to generate $5 million in profitProfit ModelA profit model refers to a company’s plan that aims to make the business profitable and viable. It lays out what the company plans to manufacture, how. The following is a schedule on the project:

Notes:

- Costs Incurred is the costs incurred to build the bridge as estimated by the company’s engineer.

- Billings are the amount of money StrongBridges Ltd. billed for the construction of the bridge. Billings amount is set by the contract.

- Cash Collected is the amount of money StrongBridges Ltd. received for the construction of the bridge. The variation in billings and cash collected is due to timing differences.

- % Completed is determined by the percentage completion formula.

For the schedule above, revenues recognized under the percentage of completion method:

- Year 2008: 33% completed. Revenue recognized = 33% x $20 million (contract price) = $6,600,000

- Year 2009: 47% completed. Revenue recognized = 47% x $20 million (contract price) – $6.6 million (previously recognized) = $2,800,000

- Year 2010: 100% completed. Revenue recognized = 100% x $20 million (contract price) – $6.6 million – $2.8 million (previously recognized) = $10,600,000

Total Revenue = $20,000,000

Costs recognized under the percentage of completion method:

- Year 2008: $5,000,000

- Year 2009: $2,000,000

- Year 2010: $8,000,000

Total Cost = $15,000,000

Profit recognized under the percentage of completion method:

- Year 2008: $6,600,000 – $5,000,000 = $1,600,000

- Year 2009: $2,800,000 – $2,000,000 = $800,000

- Year 2010: $10,600,000 – $8,000,000 = $2,600,000

Gross Profit = $5,000,000

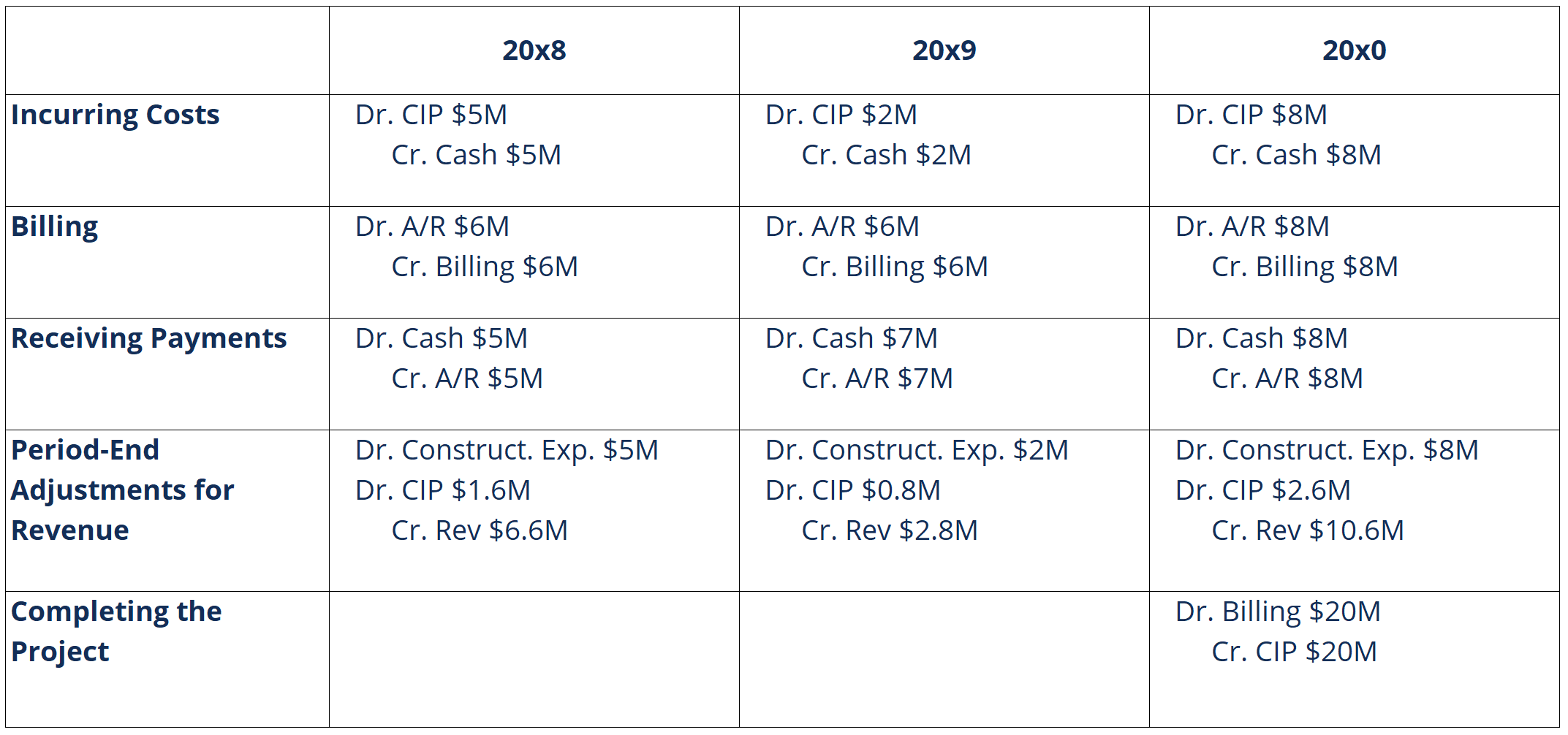

Journal entries for the example above would be as follows:

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Evaluation PlanEvaluation PlanAn evaluation plan is part of the planning for a project - the part that is related to deciding how the project will be monitored and assessed

- Project Budget TemplateProject Budget TemplateThis project budget template provides you with a tool to summarize the cost budget for a project. The Project Budget is a tool used by project managers to estimate the total cost of a project. A Project Budget template includes a detailed estimate of all costs that are likely to be incurred before the project is comple

- Project FinanceProject Finance - A PrimerProject finance primer. Project finance is the financial analysis of the complete life-cycle of a project. Typically, a cost-benefit analysis is used to

- Raid LogRAID LogA RAID Log is a project management tool that is aimed at centralizing and simplifying the collection, monitoring, and tracking of project data

-

Effective Interest Method Explained: Bond Amortization & Accounting

The Effective Interest Method is a technique used for amortizing bonds to show the actual interest rate in effect during any period in the life of a bond before maturity. It is based on the bond&rsquo

-

Understanding Accounting Methods: Cash vs. Accrual

An accounting method refers to a set of rules that a company adheres to when keeping its financial records and reporting financial transactions. The transactions are recorded in a manner that accurate

Accounting

- Understanding the Completed Contract Method: Revenue Recognition Explained

- Consolidation Method Explained: A Comprehensive Guide

- Cost Method Explained: Accounting & Investment Strategies

- Cost Recovery Method: Understanding Revenue Recognition

- Direct Method for Cash Flow Statements: A Comprehensive Guide

- Equity Method Accounting: Definition & Intercorporate Investments

- High-Low Method: Understanding & Application in Cost Accounting

- Profitability Index (PI): Definition, Formula & Investment Ranking

- Specific Identification Method: A Comprehensive Guide for Inventory Valuation

-

Vietnamese Dong (VND): A Comprehensive Guide to Vietnam's Currency

Vietnamese Dong (VND): A Comprehensive Guide to Vietnam's CurrencyThe Vietnamese Dong refers to Vietnam’s official currency and is represented by ISO code VND. The word “dong” implies money in Vietnamese; it means adding the word after a country&rs...

-

Capitalization-Weighted Index (CWI): Explained

Capitalization-Weighted Index (CWI): ExplainedThe Capitalization-Weighted Index (cap-weighted index, CWI) is a type of stock market index in which each component of the index is weighted relative to its total market capitalizationMarket Capitaliz...