Acid-Test Ratio: Understanding Your Company's Short-Term Liquidity

The Acid-Test Ratio, also known as the quick ratioQuick RatioThe Quick Ratio, also known as the Acid-test, measures the ability of a business to pay its short-term liabilities with assets readily convertible into cash, is a liquidity ratio that measures how sufficient a company’s short-term assetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and are to cover its current liabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the. In other words, the acid-test ratio is a measure of how well a company can satisfy its short-term (current) financial obligations. This guide will break down how to calculate the ratio step by step, and discuss its implications.

The Acid-Test Ratio Formula

The formula for calculating the ratio is as follows:

The following items can all be found on a company’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting.:

- Cash and cash equivalents are the most liquid current assets on a company’s balance sheet, such as savings accounts, a term deposit with a maturity of fewer than 3 months, and T-billsTreasury Bills (T-Bills)Treasury Bills (or T-Bills for short) are a short-term financial instrument issued by the US Treasury with maturity periods from a few days up to 52 weeks..

- Marketable securities are liquid financial instruments that can be readily converted into cash.

- Accounts receivables are the money owed to the company from providing customers with goods and/or services.

- Current liabilities are debts or obligations due within one year.

The acid-test ratio formula can alternatively be rendered as follows:

Where:

- Current assets are assets that can be reasonably converted into cash within a year.

- Inventories are the value of materials and goods held by a company with the intention of selling them to customers.

The logic here is that inventory can often be slow moving and thus cannot readily be converted into cash. Additionally, if it were required to be converted quickly into cash, it would most likely be sold at a steep discount to the carrying cost on the balance sheet.

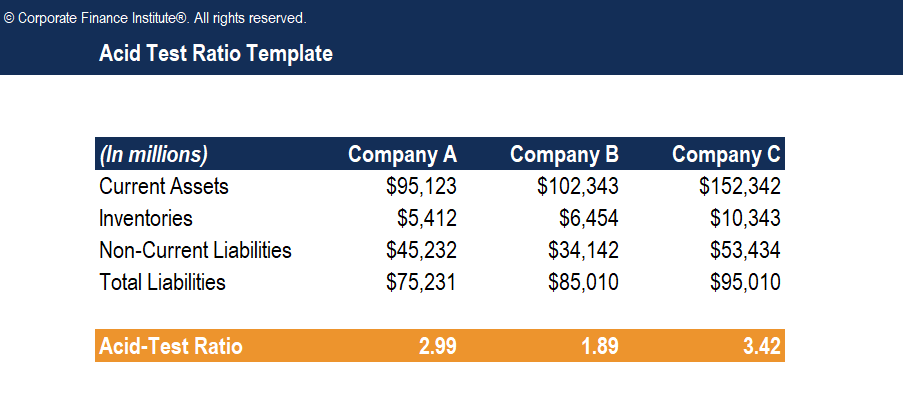

Example of the Acid-Test Ratio

Consider three hypothetical companies:

Here are the calculations of the acid-test ratio for each company:

- Company A: ($95,125 – $5,412) / ($75,231 – $45,232) = 2.99

- Company B: ($102,343 – $6,454) / ($85,010 – $34,142) = 1.89

- Company C: ($152,342 – $10,343) / ($95,010 – $53,434) = 3.42

Note: To determine the current liabilities for each company, total liabilities are subtracted from non-current liabilities.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Interpretation of the Acid-Test Ratio

The acid-test ratio is used to indicate a company’s ability to pay off its current liabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the without relying on the sale of inventory or on obtaining additional financing. Inventory is not included in calculating the ratio, as it is not ordinarily an asset that can be easily and quickly converted into cash. Compared to the current ratio – a liquidity or debt ratio which does include inventory value in the calculation – the acid-test ratio is considered a more conservative estimation of a company’s financial health.

The higher the ratio, the better the company’s liquidity and overall financial health. A ratio of 2 implies that the company owns $2 of liquid assets to cover each $1 of current liabilities. However, it’s important to note that an extremely high quick ratio (for example, a ratio of 10) is not considered favorable, as it may indicate that the company has excess cash that is not being wisely put to use growing its business. A very high ratio may also indicate that the company’s accounts receivables are excessively high – and that may indicate collection problems.

The optimal acid-test ratio number for a specific company depends on the industry and marketplaces the company operates in, the exact nature of the company’s business, and the company’s overall financial stability. For example, a relatively low acid-test ratio is less significant for a well-established business with long-term contract revenues, or for a business with very solid credit, so that it can easily access short-term financing if the need arises.

Drawbacks of the Acid-Test Ratio

As with virtually any financial metric, there are a number of limitations and potential drawbacks to using the quick ratio:

- The acid-test ratio alone is not sufficient to determine the liquidity position of the company. Other liquidity ratios such as the current ratioCurrent Ratio FormulaThe Current Ratio formula is = Current Assets / Current Liabilities. The current ratio, also known as the working capital ratio, measures the capability of a business to meet its short-term obligations that are due within a year. The ratio considers the weight of total current assets versus total current liabilities. It indicates the financial health of a company or cash flow ratio are commonly used in conjunction with the acid-test ratio to provide a more complete and accurate estimation of a company’s liquidity position.

- The ratio excludes inventory from the calculation because inventory is not generally considered a liquid asset. However, some businesses are able to quickly sell their inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a at a fair market price. In such cases, the company’s inventory does qualify as an asset that can readily be converted into cash.

- The ratio does not provide information about the timing and level of cash flowsValuationFree valuation guides to learn the most important concepts at your own pace. These articles will teach you business valuation best practices and how to value a company using comparable company analysis, discounted cash flow (DCF) modeling, and precedent transactions, as used in investment banking, equity research,, which are important factors in accurately determining a company’s ability to pay its obligations when they are due.

- The acid-test ratio assumes that accounts receivable are easily and readily available for collection, but that may not actually be the case.

Other Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources listed below will be useful:

- Debt to Assets RatioFinanceCFI's Finance Articles are designed as self-study guides to learn important finance concepts online at your own pace. Browse hundreds of articles!

- Debt CapacityDebt CapacityDebt capacity refers to the total amount of debt a business can incur and repay according to the terms of the debt agreement.

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

-

Advertising to Sales Ratio: Measuring Ad Effectiveness & ROI

The advertising to sales ratio, also called the “A to S” for short, measures the effectiveness, or how successful, a company’s advertising strategiesAIDA ModelThe AIDA model, which s

-

Understanding the CAPE Ratio: A Guide to Cyclically Adjusted P/E

The CAPE Ratio (also known as the Shiller P/E or PE 10 Ratio) is an acronym for the Cyclically-Adjusted Price-to-Earnings Ratio. The ratio is calculated by dividing a company’s stock price by th

finance

- Asset Turnover Ratio: Definition & Calculation - Financial Analysis

- Current Ratio: Definition, Calculation & Financial Health

- Debt-to-Asset Ratio: Definition, Calculation & Significance

- Defensive Interval Ratio (DIR): Understanding Company Liquidity

- Understanding the Envy Ratio in Private Equity

- Equity Ratio: Understanding Financial Leverage & Risk

- Net Debt to EBITDA Ratio: Understanding Company Solvency

- Pretax Margin Ratio: Definition & Analysis | Financial Insights

- Receivables Turnover Ratio: Definition, Calculation & Importance

-

Fixed-Charge Coverage Ratio (FCCR): Definition & Importance

Fixed-Charge Coverage Ratio (FCCR): Definition & ImportanceThe Fixed-Charge Coverage Ratio (FCCR) is a measure of a company’s ability to meet fixed-charge obligations such as interest expensesInterest ExpenseInterest expense arises out of a company that...

-

Times Interest Earned (TIE) Ratio: Calculation & Interpretation

Times Interest Earned (TIE) Ratio: Calculation & InterpretationThe Times Interest Earned (TIE) ratio measures a company’s ability to meet its debt obligations on a periodic basis. This ratio can be calculated by dividing a company’s EBITEBIT GuideEBIT...