Entry Multiple: Definition & Importance in Private Equity

An entry multiple, commonly used in leveraged buyouts, refers to the price paid for a company as a function of a financial metric. The entry multiple is crucial for private equity firmsTop 10 Private Equity FirmsWho are the top 10 private equity firms in the world? Our list of the top ten largest PE firms, sorted by total capital raised. Common strategies within P.E. include leveraged buyouts (LBO), venture capital, growth capital, distressed investments and mezzanine capital. to know, as it helps them determine the purchase price of a company relative to a financial metric. It is ideal to purchase companies at a low entry multiple.

Summary

- An entry multiple refers to the price paid for a company as a function of a financial metric.

- A common multiple used for the entry multiple is EV/EBITDA.

- An entry multiple is commonly compared to an exit multiple.

Understanding Multiples

A multiple, also known as a multiplier, is a valuation technique that calculates the value of a business relative to a financial metric. Multiples are used to compare businesses operating in similar environments to determine whether a company is reasonably priced, compared to peers. There are numerous types of multiples that can be used, including EV/EBITDAEV/EBITDAEV/EBITDA is used in valuation to compare the value of similar businesses by evaluating their Enterprise Value (EV) to EBITDA multiple relative to an average. In this guide, we will break down the EV/EBTIDA multiple into its various components, and walk you through how to calculate it step by step, EV/Sales, EV/EBITEV/EBIT RatioThe enterprise value to earnings before interest and taxes (EV/EBIT) ratio is a metric used to determine if a stock is priced too high or too low, EV/UFCF, and P/EPrice Earnings RatioThe Price Earnings Ratio (P/E Ratio is the relationship between a company’s stock price and earnings per share. It provides a better sense of the value of a company. multiples.

For example, if two companies operating in the same industry with similar business operations trade at P/E multiples of 10x and 4x respectively, ignoring other factors, the company with a 4x P/E multiple is deemed undervalued by investors.

Understanding Entry Multiple

Private equity firms use multiples to understand the price that they are paying for a company relative to a financial metric. For example, when a private equity firm is looking to purchase a company, they would want to compare the purchase price of the company relative to a financial metric – This is termed the “entry multiple.”

The most commonly used multiple for an entry multiple is EV/EBITDA. EV is enterprise value and typically represents the total value of a company. EBITDA is the earnings of a company before interest, taxes, depreciation, and amortization – the company’s operating income.

Example

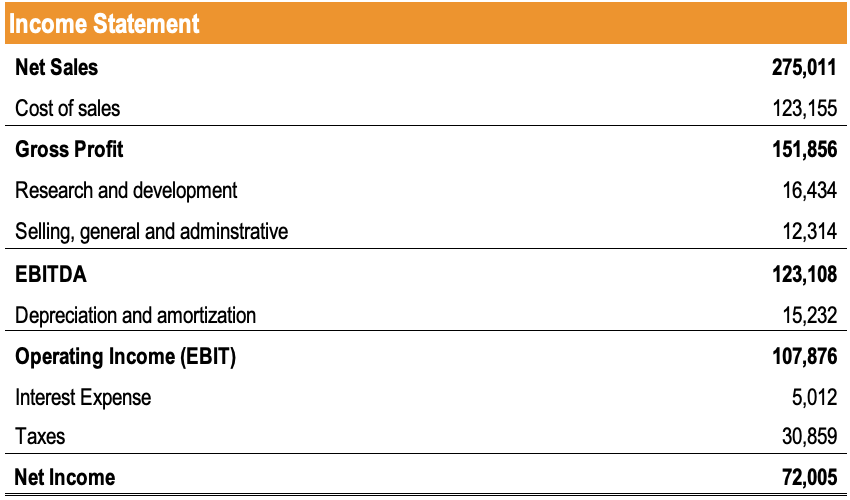

A private equity firm is looking to generate a 25% IRR in a leveraged buyoutLeveraged Buyout (LBO)A leveraged buyout (LBO) is a transaction where a business is acquired using debt as the main source of consideration. of a company. The firm must pay $500,000 to purchase the company. The income statement of the company is as follows:

Using the EV/EBITDA multiple, what is the implied entry multiple of this company?

The implied entry multiple of this company is $500,000/$123,108 = 4.06x.

Relating Entry Multiple and Exit Multiple

An entry multiple is commonly used to compare to an exit multiple. Understanding that an entry multiple is the price paid for a company relative to a financial metric, an exit multiple is simply the sale price of a company relative to a financial metric.

Multiple Expansion

For private equity firms, it is desirable to achieve a low entry multiple and a high exit multiple. Essentially, this means that the firm is purchasing the company at a low price relative to a financial metric and selling the company at a higher price relative to a financial metric.

For example, if a firm purchases a company with an EBITDA of $10M at a purchase price of $100M, and sells the company five years later at a sale price of $200M when the company has an EBITDA of $15M, the entry multiple is 10x (100M/10M), and the exit multiple is 13.3x (200M/15).

Stable Multiple

When the entry multiple is the same as the exit multiple, it means that the firm is purchasing and selling the company at the same relative value. In leveraged buyout models, a stable multiple is assumed.

For example, if a firm purchases a company at a purchase price of $100M with an EBITDA of $10M and sells the company five years later at a sale price of $200M with an EBITDA of $20M, the entry multiple is 10x (100M/10M), and the exit multiple is 10x (200M/20).

Multiple Compression

When the entry multiple is higher than the exit multiple, it means that the firm is purchasing the company at a higher price relative to a financial metric and is selling the company at a lower price relative to a financial metric. This is undesirable and compromises the IRR of the investment.

For example, if a firm purchases a company at a purchase price of $100M with an EBITDA of $10M and sells the company five years later at a sale price of $100M with an EBITDA of $20M, the entry multiple is 10x (100M/10M), and the exit multiple is 5x (100M/20).

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Enterprise Value vs Equity ValueEnterprise Value vs Equity ValueEnterprise value vs equity value. This guide explains the difference between the enterprise value (firm value) and the equity value of a business. See an example of how to calculate each and download the calculator. Enterprise value = equity value + debt - cash. Learn the meaning and how each is used in valuation

- Internal Rate of Return (IRR)Internal Rate of Return (IRR)The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

- Profitability RatiosProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit

- Types of Valuation MultiplesTypes of Valuation MultiplesThere are many types of valuation multiples used in financial analysis. They can be categorized as equity multiples and enterprise value multiples.

-

Understanding Acquisition Cost: Definitions & Applications

Acquisition cost is the cost of purchasing an asset. It is generally used in three different contexts in business, which include the following:Mergers and acquisitionsFixed assetsCustomer acquisition&

-

Advertising Budget: Definition, Planning & Best Practices

An advertising budget is a company’s allocation of promotional expenditures over a specified time period. It is a measure of a company’s planned expenditure on accomplishing marketing obje

finance

- Acquirer Definition: Understanding Corporate Acquisitions

- Understanding Clawbacks: Protecting Stakeholders from Failed Performance

- EBIT/EV Multiple: Understanding Earnings Yield & Valuation

- Understanding Financial Gearing: Debt & Leverage Explained

- Leverage in Finance: Strategies, Types & Risks

- Parent Company Explained: Definition, Control & Examples

- Understanding Stocks: A Beginner's Guide to Share Ownership

- Understanding Net-Net: A Financial Health Indicator

- EBITA Explained: Understanding Earnings Before Interest, Taxes, and Amortization

-

Ramp-Up: Definition, Benefits & How to Achieve It

Ramp-Up: Definition, Benefits & How to Achieve ItIn business, ramp-up is a term that describes a significant increase in the output of a company’s products or services. Essentially, ramp-up implies bringing the company’s capacity utiliza...

-

Streamlining Processes: Definition, Benefits & Techniques

Streamlining Processes: Definition, Benefits & TechniquesStreamlining refers to the improvement of the efficiency of a certain process within an organization. It can be done by automationExcel vs Automation in Financial ModelingBefore we discuss Excel vs au...