Operating Asset Turnover Ratio: Definition & Analysis

The operating asset turnover ratio, an efficiency ratio, is a variation of the total asset turnover ratioAsset Turnover RatioThe asset turnover ratio, also known as the total asset turnover ratio, measures the efficiency with which a company uses its assets to produce sales. A company with a high asset turnover ratio operates more efficiently as compared to competitors with a lower ratio. and identifies how well a company is using its operating assets to generate revenue.

Operating assets are assets that are essential to the day-to-day operations of a business. In other words, operating assets are the assets utilized in the ordinary income-generation process of a business.

Quick Summary:

- The operating asset turnover ratio is an efficiency ratio that identifies the revenue generation capabilities of a company’s operating assets.

- Examples of operating assets include PP&E, cash, accounts receivable, inventory, and land.

- The operating asset turnover ratio is calculated as sales divided by operating assets.

Examples of Operating and Non-Operating Assets

Examples of operating assets include:

- Property, plant, and equipment (PPE)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

- Cash

- Accounts receivable

- InventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a

- Patents and licenses (if required for business operations)

- Land (if used in the operations of the business)

For a general rule of thumb in determining whether an asset is an operating asset, ask yourself: “If the company does not have this asset, will they be able to continue their day-to-day operations?” If the answer is no, then the asset is likely an operating asset.

Examples of non-operating assets include:

- Marketable securitiesMarketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion.

- Loans receivable

- Vacant land (unutilized assets)

- Restricted cash (cash that is not available for immediate business use)

Formula for Operating Asset Turnover Ratio

Where:

- Sales refers to the total revenue earned by the company

- Operating assets, as defined above, are assets that are essential to the day-to-day operations of a business

Example

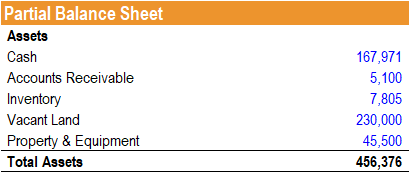

Jeff is an equity analyst and is looking to determine the efficiency of a company’s use of its assets. A partial balance sheet of the company is provided as follows:

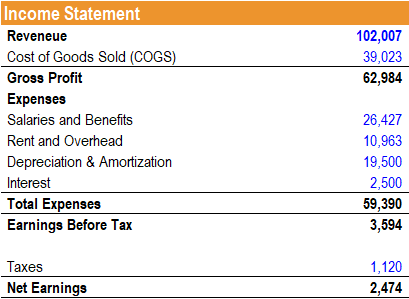

Additionally, the income statement of the company is provided as follows:

Jeff notes that the company’s balance sheet includes a line item for vacant land at $230,000. He decides to use a variation of the total asset turnover – the operating asset turnover to account for the vacant land that is not currently used in the company’s operations. He calculates the ratio as follows:

Operating Asset Turnover Ratio = (167,971 + 5,100 + 7,805 + 45,500) / 102,007 = 2.22

Therefore, for every dollar invested in its operating assets, $2.22 of revenue is generated.

Interpretation

The operating asset turnover ratio indicates how efficiently a company is using its operating assets to generate revenue. A higher ratio is desirable, as it shows that a company is better at utilizing its operating assets to generate revenue.

Although not as commonly used as the total asset turnover ratio, the operating asset turnover ratio is used when a company holds large assets on its books that are not pertinent to its operations. The ratio excludes such line items in its calculation and, thus, provides information regarding how well revenue-generating assets are being utilized.

It is important to note that there is no absolute “ideal” operating asset turnover ratio. The ratio should be analyzed relative to that of competitors or the industry average. In addition, comparing the ratio across industries does not provide a strong insight, as the operating asset requirement and revenue-generation capabilities differ significantly among industries.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Financial Analysis Ratios GlossaryFinancial Analysis Ratios GlossaryGlossary of terms and definitions for common financial analysis ratios terms. It's important to have an understanding of these important terms.

- Operating Return on Assets (OROA)Operating Return on Assets (OROA)Operating return on assets (OROA), an efficiency or profitability ratio, is an extension of the traditional return on assets ratio. Operating return on assets is used to show a company’s operating income that is generated per dollar invested specifically in its assets that are used in its everyday business operations.

- Ratio AnalysisRatio AnalysisRatio analysis refers to the analysis of various pieces of financial information in the financial statements of a business. They are mainly used by external analysts to determine various aspects of a business, such as its profitability, liquidity, and solvency.

-

Current Ratio: Definition, Calculation & Financial Health

The current ratio, also known as the working capitalNet Working CapitalNet Working Capital (NWC) is the difference between a companys current assets (net of cash) and current liabilities (net of debt)

-

Quick Ratio: Understanding Your Business's Short-Term Liquidity

The Quick Ratio, also known as the Acid-test or Liquidity ratio, measures the ability of a business to pay its short-term liabilities by having assets that are readily convertible into cashCash Equiva

finance

- Asset Turnover Ratio: Definition & Importance

- Asset Turnover Ratio: Definition & Calculation - Financial Analysis

- Cash Turnover Ratio (CTR): Calculation & Interpretation

- Debt-to-Asset Ratio: Definition, Calculation & Significance

- Debt-to-Assets Ratio: Definition, Calculation & Risk Assessment

- Fixed Asset Turnover Ratio: Calculation & Importance

- Goodwill to Assets Ratio: Definition & Analysis

- Inventory Turnover Ratio: Definition & Calculation

- Operating Ratio: Definition, Calculation & Importance

-

Asset Management: Definition, Types & Importance

Asset Management: Definition, Types & ImportanceAsset management refers to the process of developing, operating, maintaining, and selling assetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and...

-

Receivables Turnover Ratio: Definition, Calculation & Importance

Receivables Turnover Ratio: Definition, Calculation & ImportanceReceivables turnover ratio is a financial metric that is used to gauge the effectiveness of a company to offer credit and collect the money that it is owed. This ratio is calculated by taking th...