Understanding Risk Aversion: Definition & Implications

Risk aversion refers to the tendency of an economic agent to strictly prefer certainty to uncertainty. An economic agent exhibiting risk aversion is said to be risk averse. Formally, a risk averse agent strictly prefers the expected valueExpected ValueExpected value (also known as EV, expectation, average, or mean value) is a long-run average value of random variables. The expected value also indicates of a gamble to the gamble itself.

What is a Gamble?

A gamble consists of three elements:

- A set of outcomes

- The probabilityTotal Probability RuleThe Total Probability Rule (also known as the law of total probability) is a fundamental rule in statistics relating to conditional and marginal associated with each outcome

- The payoff from each outcome

Consider the following example: John and Mark are playing a game. John flips a coin and if it is heads, then Mark gives him $10. If it is tails, then Mark gives John $20.

- A set of outcomes: Heads, Tails

- Probability of Heads = Probability of Tails = ½

- John’s payoff from heads is $10. John’s payoff from tails is $20.

The general formula for expected value is the following:

Therefore, the expected value of the gamble described above is +$15 for John. He will make $15 every time he takes part in the gamble. If John is risk averse, then he strictly prefers receiving $15 with certainty to the gamble.

Risk Premium

The risk premiumDefault Risk PremiumA default risk premium is effectively the difference between a debt instrument's interest rate and the risk-free rate. The default risk premium exists to compensate investors for an entity's likelihood of defaulting on their debt. of a gamble is the extra amount required to make an agent indifferent between the gamble and the expected value of the gamble. Conversely, it can also be thought of as the amount of money a risk averse agent will pay to avoid any risk.

In the example above, the expected value of the gamble is $15. The utility received from the expected value of the gamble is 1.17 (log 15). The expected utility from the gamble is 1.15 (½ log 10 + ½ log 20). It is equal to the utility received when consumption is $14.

Therefore, the risk premium is $15 – $14 = $1. A risk averse agent is indifferent between a gamble that offers an expected value of $15 and receiving $14 with certainty. The consumer would pay up to $1 to avoid taking the gamble.

Measures of Risk Aversion

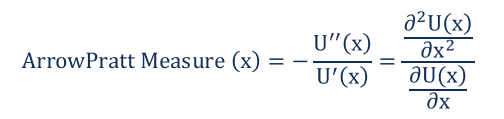

The Arrow-Pratt measure of risk aversion is the most commonly used measure of risk aversion. It analyzes the degree of risk aversion by analyzing the utility representation. The measure is named after two economists: Kenneth Arrow and John Pratt. The Arrow-Pratt formula is given below:

Where:

- U’ and U’’ are the first and second derivative of the utility function with respect to consumption x.

Significance of Risk Aversion

Speaking more practically, risk aversion is an important concept for investors. Investors who are extremely risk-averse prefer investments that offer a guaranteed, or “risk-free”, return. They prefer this even if the return is relatively low compared to higher potential returns that carry a higher degree of risk. For example, extremely risk-averse investors prefer investments such as government bonds and certificates of deposit (CDs) to higher-risk investments such as stocks and commodities.

Investors with a higher risk tolerance – or lower levels of risk aversion – are willing to accept greater levels of risk in exchange for the opportunity to earn higher returns on investment,

Additional Resources

Thank you for reading CFI’s explanation of risk aversion. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Risk and ReturnRisk and ReturnIn investing, risk and return are highly correlated. Increased potential returns on investment usually go hand-in-hand with increased risk. Different types of risks include project-specific risk, industry-specific risk, competitive risk, international risk, and market risk.

- Risk ManagementRisk ManagementRisk management encompasses the identification, analysis, and response to risk factors that form part of the life of a business. It is usually done with

- Systematic RiskSystematic RiskSystematic risk is that part of the total risk that is caused by factors beyond the control of a specific company or individual. Systematic risk is caused by factors that are external to the organization. All investments or securities are subject to systematic risk and therefore, it is a non-diversifiable risk.

- Systemic RiskSystemic RiskSystemic risk can be defined as the risk associated with the collapse or failure of a company, industry, financial institution or an entire economy. It is the risk of a major failure of a financial system, whereby a crisis occurs when providers of capital lose trust in the users of capital

-

Understanding Foreign Exchange Risk: A Comprehensive Guide

Foreign exchange risk, also known as exchange rate risk, is the risk of financial impact due to exchange rate fluctuations. In simpler terms, foreign exchange risk is the risk that a business’ f

-

Funding Liquidity Risk: Definition, Causes & Mitigation

Funding liquidity risk refers to the risk that a company will not be able to meet its short-term financial obligations when due. In other words, funding liquidity risk is the risk that a company will

finance

- Understanding Risk Grades: An Investor's Guide

- Understanding Risk Preference: A Comprehensive Guide

- Understanding Operating Risk: A Key Component of Business Risk

- Understanding Financial Risk: A Comprehensive Guide

- Understanding Risk Aversion: Definition & Implications

- Risk Shifting: Definition, Examples & Implications

- Understanding Currency Risk: A Comprehensive Guide

- Understanding Downside Risk: Protecting Your Investments

- Understanding Risk Aversion in Investing: A Beginner's Guide

-

Understanding Credit Risk: Definition & Implications

Understanding Credit Risk: Definition & ImplicationsCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally, the failure to make required payments on loans...

-

Default Risk Premium: Understanding & Calculation

Default Risk Premium: Understanding & CalculationA default risk premium is effectively the difference between a debt instrument’s interest rate and the risk-free rateRisk-Free RateThe risk-free rate of return is the interest rate an investor c...