Collar Option Strategy: A Comprehensive Guide for Risk Management

A collar option strategy, also referred to as a hedge wrapper or simply collar, is an optionsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price. strategy employed to reduce both positive and negative returns of an underlying assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations.. It limits the return of the portfolio to a specified range and can hedge a position against potential volatilityVolatilityVolatility is a measure of the rate of fluctuations in the price of a security over time. It indicates the level of risk associated with the price changes of a security. Investors and traders calculate the volatility of a security to assess past variations in the prices of the underlying asset. A collar position is created through the usage of a protective putProtective PutA protective put is a risk management and options strategy that involves holding a long position in the underlying asset (e.g., stock) and purchasing a put option with a strike price equal or close to the current price of the underlying asset. A protective put strategy is also known as a synthetic call. and covered callCovered CallA covered call is a risk management and an options strategy that involves holding a long position in the underlying asset (e.g., stock) and selling (writing) a call option on the underlying asset. option. More specifically, it is created by holding an underlying stock, buying an out of the money put option, and selling an out of the money call option.

Summary

- A collar option strategy is an options strategy that limits both gains and losses.

- A collar position is created by holding an underlying stock, buying an out of the money put option, and selling an out of the money call option.

- Collars may be used when investors want to hedge a long position in the underlying asset from short-term downside risk.

Creating a Collar Position

Interpreting the Collar Option Strategy

The collar option strategy will limit both upside and downside. The collar position involves a long positionLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). on an underlying stock, a long position on the out of the money put option, and a short positionLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). on the out of the money call option.

By taking a long position in the underlying stock, as the price increases, the investor will profit. As the price decreases, the investor will experience a loss. Holding a long position on an out of the money put option, as the price of the underlying stock decreases, the put option value increases. We see here that the downside of a falling stock price is neutralized by the put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option..

The investor will also take a short position on an out of the money call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame.. If the price of the underlying stock increases, the call option will be exercised by the buyer. Therefore, as the seller, you will experience a loss as the underlying asset increases in price. This potential loss neutralizes the upside of holding the stock.

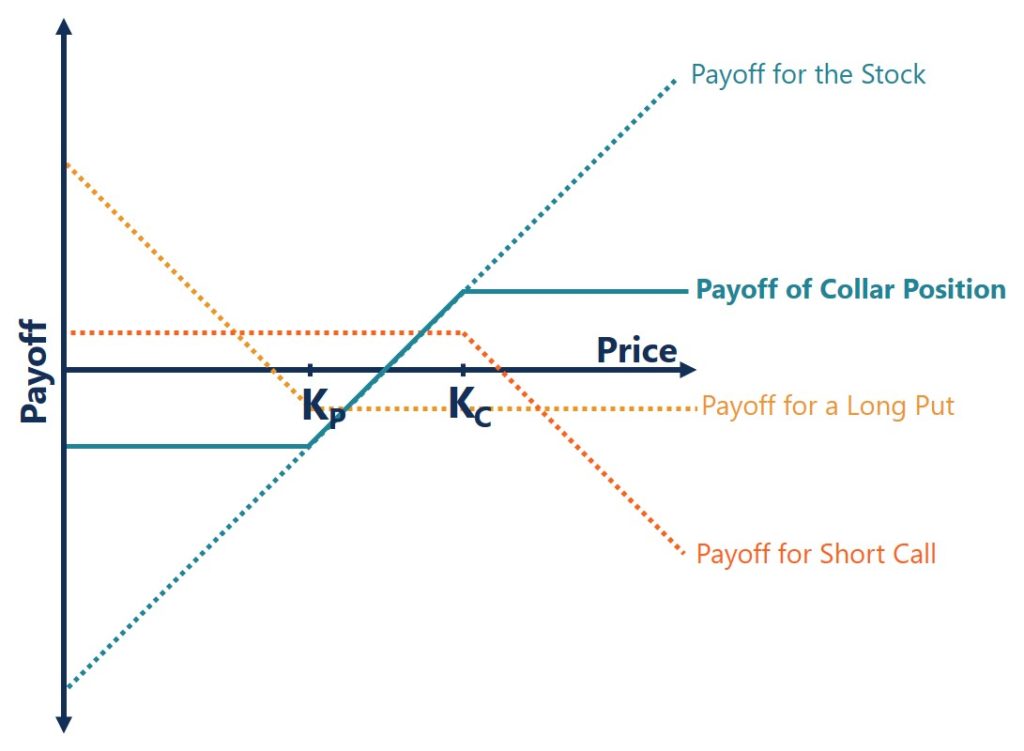

The value of the underlying asset between the strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on of the put option and call option is the value of the portfolio that moves. The loss experienced by the call option above the call strike price will cancel with gains from the stock appreciating, therefore the payoff will be flat here. The gains experienced by the put option below the strike price will cancel with the loss from the depreciating stock price. The payoff will also be flat here. Below we can see what the payoff diagram of a collar would look like.

Collar Option Payoff Diagram

The payoff of a collar can be understood through the use of a payoff diagram. By plotting the payoff for the underlying asset, long put option, and short call option we can see what the collar position payoff would be:

In the chart above, we see that below the put strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on (Kp) and above the call strike price (Kc), the payoff is flat. The potential upside and downside of the portfolio are limited. It is only between the strike prices that we see the payoff movement of a collar position.

Uses of the Collar Option Strategy

The collar option strategy is most often used as a flexible hedgingHedgingHedging is a financial strategy that should be understood and used by investors because of the advantages it offers. As an investment, it protects an individual’s finances from being exposed to a risky situation that may lead to loss of value. option. If an investor holds a long position on a stock, they can construct a collar position to protect against large losses. It is through the usage of the protective putProtective PutA protective put is a risk management and options strategy that involves holding a long position in the underlying asset (e.g., stock) and purchasing a put option with a strike price equal or close to the current price of the underlying asset. A protective put strategy is also known as a synthetic call. option that will gain when the underlying asset falls in price. The covered callCovered CallA covered call is a risk management and an options strategy that involves holding a long position in the underlying asset (e.g., stock) and selling (writing) a call option on the underlying asset. option is sold which can be used to pay for the put option and it will still allow potential upside from an appreciation in the underlying asset, up to the call’s strike price. When the entire cost of the put option is covered by selling the call option, this is referred to as the zero-cost collar.

If a stock has strong long-term potential, but in the short-term has high down-side risk then a collar can be considered. Investors will also consider a collar strategy if a stock they are long in has recently appreciated significantly. To protect these unrealized gains a collar may be used. The use of a collar strategy is also used in mergers and acquisitionsMergers Acquisitions M&A ProcessThis guide takes you through all the steps in the M&A process. Learn how mergers and acquisitions and deals are completed. In this guide, we'll outline the acquisition process from start to finish, the various types of acquirers (strategic vs. financial buys), the importance of synergies, and transaction costs. In a stock deal, a collar can be used to ensure that a potential depreciation of the acquirers stock does not lead to a situation where they must pay much more in diluted shares.

Collar Option Strategy – Worked Example

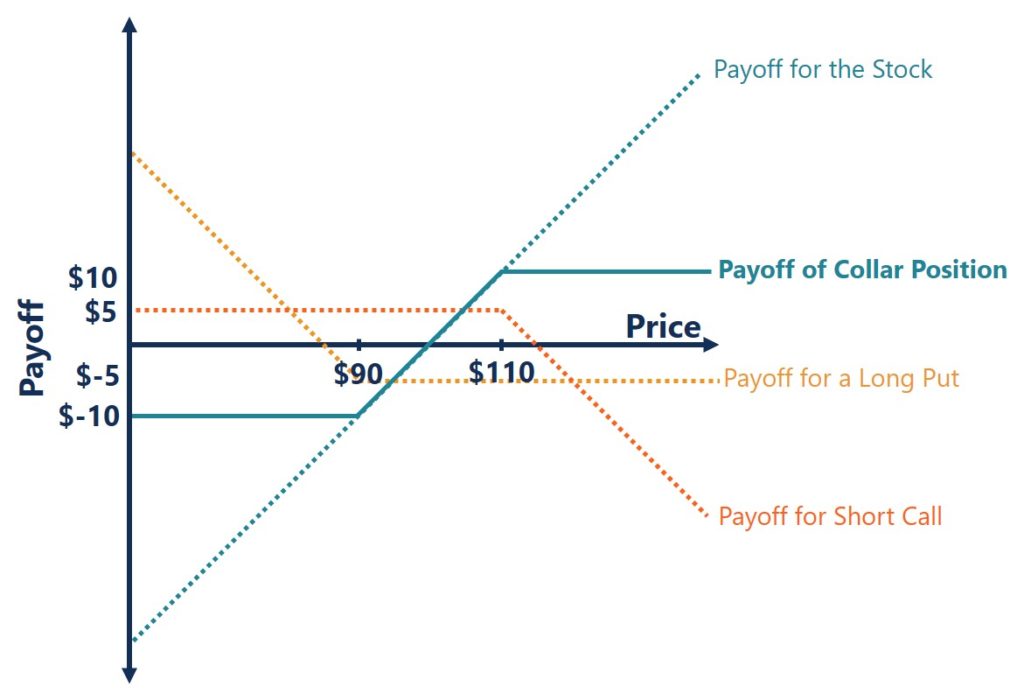

Let us now look at an example that involves creating a collar. Say you are holding a long positionLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). on an asset that has just recently appreciatedAppreciationAppreciation refers to an increase in the value of an asset over time. The term is widely used in several disciplines, including economics, finance, and to a price of $100. You are unsure about the price stability in the near-term future and want to utilize a collar strategy. You buy a put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option. with a strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on of $90 at a premium of $5. You also sell a call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. for $5 with a strike price of $110.

What is your payoff if the price of the asset falls to $80?

- The call option you’ve sold will not be exercised by the buyer and you will end with a payoff of $5.

- The put option you’ve bought for $5 will be exercised with a strike price of $90 meaning a payoff of $5.

- The underlying asset will be worth $80 meaning a loss of $20.

The protective put optionProtective PutA protective put is a risk management and options strategy that involves holding a long position in the underlying asset (e.g., stock) and purchasing a put option with a strike price equal or close to the current price of the underlying asset. A protective put strategy is also known as a synthetic call. you’ve purchased reduced the losses experienced from a drop in the price of the underlying asset. In total your net loss will be: $5 + $5 – $20 = -$10.

Rather than experiencing the full loss of $80 – $100 = -$20, you have ended with a net loss of only $10.

What is your payoff if the price of the assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations. increases to $105?

- The call option you’ve sold for $5 will not be exercised since the underlying asset price is still below the strike price. You will end with a payoff of $5.

- The put option you’ve bought will not be exercised since the underlying price is above the strike price. You will realize a net loss of $5.

- The underlying will be worth $105, meaning a net gain of $5.

The out of the money call and putOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price. were both not exercised. Selling the call option covered the cost of buying the put option so the payoff and loss from the two transactions canceled each other out. In total, your net payoff will be: $5 – $5 + $5 = $5.

It is the same payoff from just holding the underlying asset: $105 – $100 = $5

What is your payoff if the price of the asset increases to $115?

- The call option you’ve sold for $5 will be exercised at a strike priceStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on of $110. The payoff will be $0.

- The put option you’ve bought for $5 will not be exercised. The loss from the transaction will be -$5.

- The underlying asset will be worth $115, meaning a gain of $15,

In this scenario, you would end up with a net payoff of $0 – $5 + $15 = $10.

It is less than if you had just held the underlying assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations.: $115 – $100 = $15. In this scenario, the collar is limiting the upside potential of the underlying asset.

In the scenarios above, the call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. you’ve sold completely covers the cost of buying the put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option.. It is called a zero-cost collar. Below is an illustration of the collar position:

Here, we can see that the loss is capped if the price of the underlying asset falls below $90. Similarly, if the price of the underlying asset rises above $110, the payoff is also capped. To further illustrate this, let’s look at two more scenarios.

What would the payoff be if the asset dropped in price to $0?

- The call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. you’ve sold for $5 would not be exercised and the payoff would be $5.

- The put option you’ve bought for $5 would be exercised at a strike price of $90. The payoff would be $90 – $5 = $85.

- The underlying asset’s fallen from $100 to $0, resulting in a loss of $100.

The net payoff to you would be $5 + $85 – $100 = -$10.

It is the same payoff when the asset fell to a price of $80. We see that the protective putProtective PutA protective put is a risk management and options strategy that involves holding a long position in the underlying asset (e.g., stock) and purchasing a put option with a strike price equal or close to the current price of the underlying asset. A protective put strategy is also known as a synthetic call. is capping the losses experienced from a fall in the underlying asset.

What would the payoff be if the asset rose in price to $200?

- The call option you’ve sold for $5 would be exercised and the payoff would be $5 – $90 = -$85.

- The put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option. you’ve bought for $5 would not be exercised. The loss from this transaction would be -$5.

- The underlying asset’s risen from $100 to $200, resulting in a gain of $100.

The net payoff to you would be -$85 – $5 + $100 = $10.

It is the same payoff when the price increased to $115. Here, we can see how the collar position limited the upside potential of the underlying asset.

Additional Resources

Thank you for reading CFI’s resource on the collar option strategy. If you would like to learn about related concepts, check out CFI’s other resources below:

- HedgingHedgingHedging is a financial strategy that should be understood and used by investors because of the advantages it offers. As an investment, it protects an individual’s finances from being exposed to a risky situation that may lead to loss of value.

- Protective PutProtective PutA protective put is a risk management and options strategy that involves holding a long position in the underlying asset (e.g., stock) and purchasing a put option with a strike price equal or close to the current price of the underlying asset. A protective put strategy is also known as a synthetic call.

- Synthetic PositionSynthetic PositionA synthetic position is a trading option used to simulate the features of another comparable position. More specifically, a synthetic position is created to

- Options Case Study – Long CallOptions Case Study – Long CallTo study the complex nature and interactions between options and the underlying asset, we present an options case study. It's much easier to

-

Understanding Option Intrinsic Value: A Clear Explanation

Intrinsic value for call options is literally the difference between the price of the market and the strike price (or exercise price), as long as the market is above the strike price. The intrin

-

Profitable Options Trading Strategies: A Comprehensive Guide

Welcome back to the derivative segment. Here, we discuss the meanings and strategies related to derivatives, and how you can use derivatives to maximise your profits, or simply hedge your position

invest

- Call Options: A Comprehensive Guide for Investors

- Understanding Delta: A Key Risk Measure in Derivatives

- Understanding Digital Options: A Comprehensive Guide for Traders

- Understanding Exercise Price in Options Trading

- Knock-In Options Explained: A Comprehensive Guide

- Knock-Out Options: A Comprehensive Guide

- Naked Options: Risks, Rewards, and How They Work

- Understanding Near-The-Money Options: A Comprehensive Guide

- Put Options Explained: A Comprehensive Guide for Investors

-

Understanding Put-Call Parity: A Comprehensive Guide

Put-call parity is an important concept in options Options: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certa...

-

Understanding At-The-Money (ATM) Options: A Comprehensive Guide

Understanding At-The-Money (ATM) Options: A Comprehensive GuideAt the money (ATM) describes a situation when the strike price of an option is equal to the underlying asset’s current market price. It is a concept of moneyness, which describes the position be...