Understanding Dirty Price: Bond Pricing Explained

Dirty price is when a bond price includes interest that has accrued since the latest coupon payment.

When investors buy fixed-income securities, such as bondsBonds vs StocksFor prospective investors and many others, it is important to distinguish between bonds vs. stocks. Two of the most common asset classes for investments are, they expect to receive coupon payments based on a fixed schedule. However, the price of a bond is dependent on the present value of future coupon payments. Unless a bond is purchased on the coupon payment date, the bond price likely includes the interest that has accrued since then.

Therefore, the buyer will miss out on one coupon payment, and the seller will pocket the accrued interest – this would be a dirty price. This contrasts with a clean price, which excludes any accrued interest.

Summary

- Dirty price is when a bond price includes interest that has accrued since the latest coupon payment.

- It is seen as “dirty” because the accrued interest included in the bond price goes to the seller.

- To calculate the dirty price, sum the clean price and the accrued interest.

Understanding Dirty Price

To understand dirty price, it’s important first to understand how bonds work. Like other fixed-income assets, bonds provide a coupon payment to the bondholder on a fixed schedule. Coupon payments can occur monthly, quarterly, or annually. However, most bonds make coupon payments on a semi-annual basis (every six months).

A bond is priced based on the present value of its future cash flows. Once a coupon payment has been made, there will be no further payments until the next payment date. The interest that accrues between each payment date is known as the accrued interestAccrued InterestAccrued interest refers to interest generated on an outstanding debt during a period of time, but the payment has not yet been made or. On the payment date, the accrued interest resets back to zero again.

If an investor decides to purchase a bond after the payment date, they won’t receive any coupon payments until the next payment date. However, the bond seller may price a bond to include any accrued interest up to the sell date – it is known as the dirty price.

The price is referred to as “dirty” because the buyer pays for the price of the bond and the accrued interest but won’t receive any coupon payments until the next payment date. Therefore, the accrued interest that was included in the bond price goes to the seller.

How to Calculate the Prices

In the U.S., it is typical to provide clean bond prices by excluding any accrued interest. After the purchase has been completed (settled), the accrued interest is then added back to the clean price to reflect the bond’s true market value.

Dirty Price

Calculating the dirty price is quite simple; we just need to add the accrued interest to the clean price.

The formula is as follows:

Dirty Price = Clean Price + Accrued Interest

Clean Price

If we wish to find the clean price, we simply separate the effect of the accrued interest from the dirty price.

The formula would be as follows:

Clean Price = Dirty Price – Accrued Interest

Both Prices

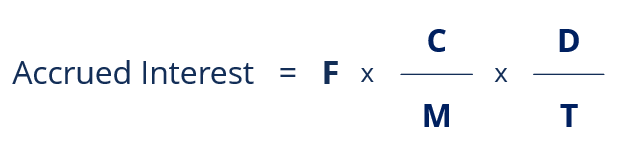

To calculate both prices, we would also need the formula for the accrued interest:

Where:

- F = Face value

- C = Total annual coupon rateCoupon RateA coupon rate is the amount of annual interest income paid to a bondholder, based on the face value of the bond.

- M = Number of coupon payments per year

- D = Days since last payment date

- T = Accrual period (number of days between payments)

Real-World Example

Let’s suppose a government bond pays a coupon rate of 5% and reaches maturity in 2022. The coupon is paid semiannually on December 1 and June 1. Let’s suppose an investor buys the bond on January 1, 2020, for a price of $1,500.

To calculate the dirty price, we first need the interest that has accrued since the last payment date. If the bond was settled on January 1, then 31 days have passed. Using the formula from above:

Solving the above equation provides an accrued Interest of $6.37.

To find the dirty price, we would use the formula given above:

Dirty Price = Clean Price + Accrued Interest

Dirty Price = $1,500 + $6.37 = $1,506.37

Therefore, the dirty price of a bond sold on January 1 would be $1,506.37.

Related Readings

To keep advancing your career, the additional CFI resources below will be useful:

- AccrualAccrualAn accrual is the basis of the accrual principle of accounting that adjusts the revenues earned and expenses incurred by a company at the end

- Coupon Rate TemplateCoupon Rate Templatehis coupon rate template will calculate a bonds coupon rate based on the total annual coupon payments and the face value of the bond. As is customary with CFI templates the blue values are hardcoded numbers and black numbers are calculations dependent on other cells. Here is a snippet of the template:

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- Debt SecurityDebt SecurityA debt security is any debt that can be bought or sold between parties in the market prior to maturity. Its structure represents a debt owed

-

Understanding Clearing Prices in Stock Trading: A Comprehensive Guide

Clearing price is a term that is often used in the stock market. If you plan on trading the market, you need to understand what the clearing price is and how it affects you as an investor. Bid a

-

Understanding Insurable Interest: A Comprehensive Guide

An individual has an insurable interest in something if he or she would suffer greatly financially or otherwise if it were damaged or destroyed. The insured has a stake in the item or property a

invest

- Understanding Add-On Interest: How It Works & Loan Payments

- Understanding Interest: Costs & Rewards of Borrowing and Lending

- Understanding Divergence in Technical Analysis: A Guide

- Understanding Forward Prices: Definition & How They Work

- Understanding Hedging Strategies: A Comprehensive Guide

- Understanding Slippage in Trading: Causes & Impact

- Understanding Strangle Options: A Comprehensive Guide

- Understanding Volatility: A Key Indicator of Investment Risk

- Compound Interest: Understand the Power of Exponential Growth

-

What is Price Fixing?

What is Price Fixing?Price fixing refers to an agreement between market participants to collectively raise, lower, or stabilize prizes to control supply and demandSupply and DemandThe laws of supply and demand are microec...

-

Price Skimming: Definition, Strategy & When to Use It

Price Skimming: Definition, Strategy & When to Use ItPrice skimming, also known as skim pricing, is a pricing strategy in which a firm charges a high initial price and then gradually lowers the price to attract more price-sensitive customers. The pricin...